Introduction

Most auto dealers running their own reinsurance programs never encounter an Industry Loss Warranty directly. But the broader reinsurance market — where ILWs trade regularly — shapes the pricing, capacity, and stability of the insurance market that backs every dealer program in the country.

When a major catastrophe triggers industry-wide losses and tightens reinsurance capacity, dealers feel it downstream: higher premiums, reduced coverage options, and pressure on the carriers backing their programs. Understanding what ILWs are and how they work gives dealers a clearer picture of why reinsurance markets move the way they do.

This article covers the core mechanics of ILWs: what they are, how triggers and payouts function, the different contract types, their advantages and limitations, and how they compare to other insurance-linked securities (ILS). It's written for dealer principals, F&I directors, and anyone else who wants to understand the reinsurance ecosystem that sits behind their program.

TLDR

- An ILW pays out when total industry-wide insured losses from a catastrophe exceed a pre-set threshold — not when an individual company hits a loss target

- Two trigger types exist: binary (full payout if threshold met) and dual-trigger (requires both industry loss AND buyer's own losses)

- Basis risk is the primary risk for ILW buyers: industry losses can exceed the trigger while the buyer's own losses stay below expectations, resulting in a payout that doesn't match actual exposure

- ILWs are faster and cheaper to arrange than catastrophe bonds, but less flexible in trigger precision

- ILW market dynamics shape broader reinsurance pricing — when ILW capacity tightens after a major catastrophe, dealers feel it through higher premiums and reduced coverage options

What Is an Industry Loss Warranty (ILW)?

An ILW is a reinsurance or derivative contract where a buyer receives compensation based on total insured losses across the entire insurance industry from a catastrophic event — not based on their own portfolio's performance. If a hurricane causes $25 billion in industry losses and a contract's trigger is set at $20 billion, the buyer collects. If losses come in at $18 billion, nothing is paid — regardless of what the buyer personally lost.

The Two Core Contract Terms

Every ILW is built around two numbers:

- Trigger: the industry-wide loss threshold that must be exceeded for the contract to activate (e.g., $20 billion in hurricane losses across all U.S. insurers)

- Limit: the maximum payout the buyer receives when the trigger is met (e.g., $100 million)

So in that example: the buyer pays a premium, and if a qualifying hurricane generates $20 billion or more in total industry losses, the buyer receives up to $100 million in compensation.

Reinsurance Contract or Financial Derivative?

ILWs are typically documented as reinsurance contracts, but they can also be structured as financial derivatives. When structured as a derivative, an ultimate net loss clause is often added, requiring the buyer to also demonstrate their own losses meet a minimum threshold before payout is made. This clause helps the contract qualify as reinsurance for accounting and regulatory purposes rather than a pure speculative instrument.

That regulatory distinction shapes how ILWs have evolved — and why they gained traction during periods of extreme market stress.

A Brief History

ILWs were first traded in the 1980s but remained a niche product for years. Growth accelerated sharply after Hurricane Andrew (1992), the September 11 attacks (2001), and the active 2004–2005 hurricane seasons. Two forces drove that expansion: hedge funds entering the reinsurance market and the breakdown of the retrocessional market (the layer of reinsurance that protects reinsurers themselves). You'll also hear them called original loss warranties.

Typical market participants:

- Buyers include insurers, reinsurers, and Lloyd's syndicates with concentrated catastrophe exposure

- Sellers include traditional reinsurers, hedge funds, and ILS fund managers providing capacity in exchange for premium income

How ILW Triggers and Payouts Work

Industry Loss Indices

ILW payouts aren't triggered by the buyer reporting their own losses. An independent third-party index must confirm that total industry losses crossed the threshold. The three most commonly used indices are:

- Property Claims Services (PCS), a Verisk unit, is the standard for U.S. peril losses

- SIGMA (Swiss Re) handles international loss reporting across global events

- PERILS AG focuses specifically on European catastrophe events

PCS also offers "supported triggers" designed specifically for ILW and ILS contract use. Using informal or unsupported data sources as triggers creates real problems — PCS has warned that informal indices may not report at regular intervals, delaying loss finalization and trapping collateral.

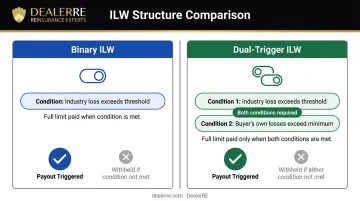

Binary vs. Dual-Trigger ILWs

| Contract Type | How It Works |

|---|---|

| Binary ILW | Full limit paid if industry loss exceeds trigger — one condition, no other requirements |

| Indemnity-Based (Dual-Trigger) ILW | Requires BOTH the industry loss trigger AND the buyer's own retained losses to exceed specified amounts |

The dual-trigger structure exists to reduce moral hazard. A buyer with skin in the game is less likely to be indifferent about managing their own losses.

Beyond trigger type, ILW contracts also differ in how they measure qualifying events — and that distinction matters a great deal for buyers facing volatile loss years.

Per Occurrence vs. Aggregate Structures

A per occurrence ILW responds to a single catastrophic event: one earthquake, one hurricane season landfall. The trigger is clean and discrete.

An aggregate ILW responds if the cumulative total of qualifying industry losses from multiple events over a defined period exceeds a set threshold. This structure appeals to buyers worried about a bad year with several mid-sized events rather than one catastrophic single loss.

How Premiums Are Calculated

ILW premiums are expressed as a rate on line (ROL) — the premium as a percentage of the coverage limit. A 10% ROL on a $100 million limit means a $10 million premium.

ROL reflects the modeled probability of the trigger being reached. Higher trigger thresholds produce lower rates on line; lower thresholds cost more. Artemis publishes ILW pricing data tracking rates for specific trigger levels across U.S. earthquake, U.S. wind, and all-natural-peril covers — traders and underwriters use it as a standard market benchmark.

For context: following the record catastrophe losses of 2011, loss-affected ILW contracts saw 30–50% rate increases, while non-loss-affected contracts saw 10–20% increases.

Trapped Collateral

ILW contracts are typically fully collateralized. After a major event, industry loss estimates can take 12–24 months to finalize. Until the reporting index certifies the final loss figure, the collateral posted by the seller becomes "trapped" — it cannot be redeployed, creating liquidity pressure for investors and sometimes delaying market participants from renewing expiring coverage.

Types of ILW Contracts Explained

Live Cat ILWs

Traded while a catastrophic event is actively occurring — for example, a hurricane approaching landfall. Buyers use these to hedge increasing exposure as storm track and intensity models update in real time. Pricing shifts rapidly as loss estimates evolve. A contract placed when a storm is offshore will look very different from one placed hours before landfall.

Dead Cat ILWs

Bought after an event has occurred but before the total industry loss is certified by the reporting index. Buyers lock in protection at a known premium while the final loss number remains uncertain. During Hurricane Harvey in 2017, Artemis reported active dead cat trading as loss estimates developed post-landfall. Buyers used these contracts to lock in certainty before the final industry loss figure was confirmed.

Backup Cover ILWs

Arranged after a primary catastrophe has depleted a buyer's existing reinsurance protection. These cover follow-on events during the remainder of the contract period. Common secondary scenarios include:

- Flooding in the days following a hurricane

- Wildfires triggered by earthquake damage

- Severe weather events that follow a primary storm

Demand typically spikes immediately after a major loss event, when buyers realize their protection is exhausted and secondary events remain possible.

Occurrence vs. Aggregate Structures

Each of the three ILW types above can be structured as either occurrence-based or aggregate. The distinction matters for how the trigger is measured:

- Occurrence: triggers on a single qualifying event exceeding the industry loss threshold

- Aggregate: triggers on the combined industry loss from multiple events within the contract period

Aggregate structures have gained traction when buyers want protection against a series of moderate catastrophes rather than waiting for one extreme event to breach a higher trigger.

Benefits and Limitations of ILWs

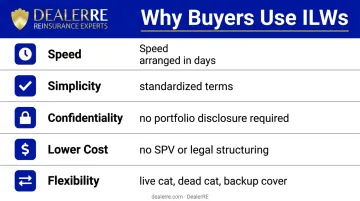

Why Buyers Use ILWs

Compared to traditional reinsurance or catastrophe bonds, ILWs offer several practical advantages:

- Speed — can be arranged in days, including during or after an event

- Simplicity — standardized terms avoid complex loss adjustment processes

- Confidentiality — buyers don't need to disclose their own portfolio data to sellers

- Lower cost than catastrophe bonds — no special purpose vehicle or extensive legal structuring required

- Flexibility — live cat, dead cat, and backup cover variants allow trading across the full event lifecycle

The Central Limitation: Basis Risk

The most significant risk for any ILW buyer is basis risk — the mismatch between what the contract pays and what the buyer actually lost.

Two scenarios create this problem:

- Under-recovery — industry losses fall short of the trigger threshold, so the contract pays nothing despite the buyer's severe individual losses

- Over-recovery — the trigger is met, but the buyer's own losses are minimal; the contract pays out more than needed

As the Casualty Actuarial Society notes, basis risk is highest for companies whose exposure concentrations differ significantly from industry averages. A regional insurer heavily concentrated in one area will often diverge from national index performance.

Index Misalignment

Basis risk worsens when the index itself is a poor fit. If the contract tracks a different geographic region, excludes certain covered perils, or two competing indices produce conflicting loss estimates, the mismatch compounds. In 2018, three major Japan catastrophe events exposed this directly — informal trigger data disrupted the ILW market through trapped collateral and elevated basis risk. PCS estimated the Japanese ILW market at $500 million to $1 billion, which illustrates how much capital can be affected when index selection goes wrong.

Index selection should be reviewed carefully during contract negotiation. Disputes at claims time are harder to resolve and far costlier than addressing misalignment upfront.

ILWs vs. Other Reinsurance and ILS Instruments

ILS as the Broader Category

Insurance-Linked Securities (ILS) is the umbrella term for financial instruments that transfer insurance risk to capital markets. ILWs are one instrument within that category. The full ILS universe includes:

- Catastrophe bonds

- Collateralized reinsurance

- Sidecars

- Industry Loss Warranties (ILWs)

ILWs are specifically the subset triggered by industry-level loss indices, as opposed to parametric triggers (which respond to physical measurements like wind speed) or indemnity triggers (which respond to an individual company's verified losses).

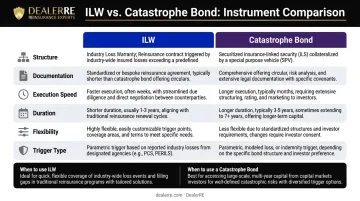

ILW vs. Catastrophe Bond

| Feature | ILW | Catastrophe Bond |

|---|---|---|

| Structure | Private contract | Issued through Special Purpose Vehicle (SPV) |

| Documentation | Standardized, lower cost | Extensive legal structure, higher cost |

| Execution speed | Days; tradeable during/after events | Weeks to months |

| Duration | Typically annual | Multi-year (commonly 3–4 years) |

| Flexibility | High — live cat, dead cat, backup cover | Pre-placed; limited mid-term adjustment |

| Trigger | Industry loss index | Indemnity, index, parametric, or modeled |

Cat bonds are the right fit when buyers want long-term, pre-placed protection and have the lead time to work with capital markets investors. ILWs serve a different need — speed, flexibility, and the ability to transact around a developing or recent event — which is why both instruments coexist in active portfolios.

Market Size and Pricing Influence

The U.S. Treasury's Federal Insurance Office 2025 Annual Report estimated ILW capacity at $5–$7 billion — roughly 8–11% of the approximately $65 billion in total ILS risk capital outstanding. That share is modest in volume, but ILWs punch above their weight in market signaling.

Because ILWs are more consistently priced and transparent than many bespoke reinsurance treaties, Artemis ILW pricing indices serve as a reference point across the broader reinsurance and cat bond markets, reflecting the current cost of peak-peril catastrophe capacity.

What Dealer-Owned Reinsurance Programs Should Know About ILWs

Auto dealers running their own reinsurance companies don't buy or sell ILWs. But the events that activate ILW contracts — major hurricanes, earthquakes, large-scale catastrophes — also drive broader reinsurance market hardening that affects every participant in the chain.

When ILW triggers are hit and large losses settle, reinsurance capacity tightens and premiums increase across the board. Guy Carpenter's January 2025 renewal data showed loss-impacted property catastrophe layers seeing risk-adjusted rate increases of up to 30% — illustrating how catastrophe events ripple through the entire market. For dealers with reinsurance programs backed by insurance carriers, this matters. Three things are directly affected:

- Carrier financial health and claims-paying capacity

- Availability of reinsurance capacity for program backing

- Premium stability over the life of the program

Understanding how ILWs function helps dealer principals ask sharper questions about their program's backing, the financial strength of the carriers involved, and how their administrator structures the program against broader market volatility.

DealerRE has worked with over 400 auto dealers to build admin obligor reinsurance programs backed by A-rated insurers. In this structure, if the dealer's reinsurance company cannot meet its financial obligations, the liability for claim payments rests with the direct writing insurance company — providing a safety net that holds regardless of what any single catastrophe season brings.

Dealers who want to understand exactly how their program is structured, and what protections are built in, can explore how DealerRE designs those programs from the ground up.

Frequently Asked Questions

What does ILW mean in insurance?

ILW stands for Industry Loss Warranty. It's a reinsurance or derivative contract that pays out when total insured losses across the entire insurance industry from a specified catastrophic event exceed a pre-set dollar threshold — not based on the individual buyer's own losses.

What is the difference between ILS and ILW?

ILS (Insurance-Linked Securities) is the broad category of instruments that move insurance risk to capital markets, including catastrophe bonds, collateralized reinsurance, sidecars, and ILWs. An ILW is one specific type of ILS instrument, distinguished by its use of an industry-wide loss index as the payout trigger.

What triggers an ILW payout?

The contract pays out when a recognized industry loss index confirms that total insured industry losses from a qualifying event have exceeded the pre-specified threshold. In the U.S., that index is typically Property Claims Services (PCS); internationally, Swiss Re's SIGMA is commonly used.

What is basis risk in an ILW?

Basis risk is the potential mismatch between what the ILW pays and what the buyer actually lost. The buyer may suffer heavy individual losses without the industry threshold being reached, receiving nothing. Conversely, the threshold may be met when the buyer's own losses are minimal, resulting in a windfall.

How are ILW premiums calculated?

ILW premiums are expressed as a "rate on line" (a percentage of the coverage limit). A catastrophe model estimates the probability of the trigger being reached, and that probability drives the rate — with higher thresholds generally producing lower rates since they're statistically less likely to be breached.

Are live cat and dead cat ILWs the same type of contract?

Both are ILW contracts but differ by timing. Live cat contracts are traded while an event is actively occurring. Dead cat contracts are bought after an event has happened but before the final industry loss total is confirmed by the reporting index.