Introduction

A string of high-mileage VSC claims. A wave of GAP payouts following a market downturn. A single bad year that erases the underwriting profits a dealer spent three years accumulating. These aren't hypothetical scenarios — they're the exact situations that dealer-owned reinsurance programs were designed to handle. But without the right protection structure, the program itself becomes the problem.

Excess of loss (XOL) reinsurance is the mechanism that prevents that outcome. It defines how much risk a dealer's reinsurance company absorbs before a separate reinsurer steps in and creates a financial ceiling on downside exposure without surrendering the upside in profitable years.

This post breaks down what XOL reinsurance is, how it works mechanically, its main types, and why dealers running their own reinsurance programs need to understand it. The goal is practical: knowing whether your program is structured to hold up when claims volume spikes or a single loss runs large.

TLDR

- XOL reinsurance only activates when losses exceed a pre-set threshold — the reinsurer covers the excess, not routine claims

- The three core types are per-risk XOL, per-occurrence XOL, and aggregate XOL (stop-loss)

- Aggregate XOL is most relevant to dealer-owned reinsurance companies — it caps total annual losses, not just single large events

- Understanding XOL structure lets dealers evaluate program proposals critically rather than taking them at face value

What Is Excess of Loss Reinsurance?

Excess of loss reinsurance is a non-proportional reinsurance structure in which the reinsurer pays losses that exceed a pre-agreed dollar threshold, up to a defined maximum. Below that threshold, the ceding party — the insurer or dealer-owned reinsurance company — absorbs losses entirely on its own.

The Reinsurance Association of America defines it plainly: XOL "indemnifies the ceding company for the amount of loss in excess of a specified retention," subject to a stated limit. Lloyd's of London describes it as a reinsurer agreeing to pay "the amount of a loss which exceeds a specified sum (the retention) up to a maximum amount."

Key Terms to Know

Three terms come up constantly in XOL contracts:

- Cedent (ceding company) — the entity transferring risk; in dealer reinsurance, this is the dealer's own reinsurance company

- Reinsurer — the party accepting the transferred risk above the retention

- Retention (attachment point) — the dollar amount the cedent keeps; the reinsurer's obligation only begins here

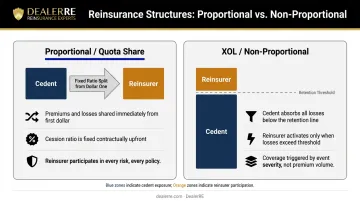

Proportional vs. Non-Proportional

The "non-proportional" label matters. In proportional reinsurance, the cedent and reinsurer split every premium dollar and every claim dollar at a fixed ratio from the first dollar. XOL works differently: the reinsurer has no involvement in small, routine claims at all. The reinsurer's obligation begins only when a loss crosses the retention threshold — not before.

The two structures differ in a few key ways:

- Proportional: Risk and premium shared from dollar one, at a fixed split

- XOL (non-proportional): Cedent absorbs all losses below the retention; reinsurer covers only the excess

- Routine claims: Stay entirely with the cedent under XOL, reducing reinsurer involvement in day-to-day losses

XOL can be structured as a treaty — covering an entire portfolio automatically — or facultative, negotiated individually per risk. For dealer-owned reinsurance programs, treaty XOL is the more common and practical arrangement.

How Excess of Loss Reinsurance Works

The Basic Structure

The market notation for XOL is: Limit xs Retention.

A layer written as $500,000 xs $100,000 means:

| Loss Amount | Who Pays |

|---|---|

| First $100,000 | Cedent (the dealer's reinsurance company) |

| $100,001 – $600,000 | Reinsurer |

| Above $600,000 | Cedent again (above the limit) |

The cedent always retains the first layer of loss. The reinsurer fills the defined band above it. Losses that exceed both the retention and the limit fall back to the cedent — so setting a realistic limit matters as much as choosing the right attachment point.

Attachment Points and Premium Cost

Setting the attachment point is a strategic decision with direct cost implications:

- Lower attachment point: The reinsurer gets involved earlier, but higher loss frequency means higher premium cost

- Higher attachment point: Premium cost drops, but the cedent must have enough capital to absorb more before reinsurance responds

As Munich Re notes, lower-attaching layers "experience a greater frequency of claims" than higher layers, which drives their rates up accordingly.

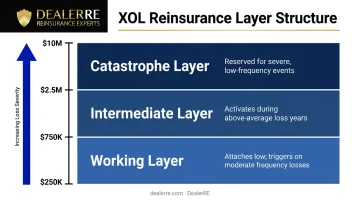

Layered Programs

Complex reinsurance programs typically stack multiple XOL layers on top of each other:

- Working layer: Attaches low and triggers regularly on moderate losses, providing the most frequent reinsurer involvement

- Intermediate layer: Activates during above-average loss years when the working layer is exhausted

- Catastrophe layer: Reserved for severe events that breach both lower layers

Each layer can have different reinsurers participating, spreading risk across multiple parties while managing overall cost.

Reinstatements

Once a loss erodes the reinsurance limit, the layer is reduced. A reinstatement provision can restore it to full capacity, typically for an additional premium. Munich Re notes: "In the event of a claim, the cover is reduced by the amount of the claim unless it is reinstated to the full amount of the cover."

For dealer-owned reinsurance companies, the number of available reinstatements determines how much protection remains after a significant claims event mid-year.

Types of Excess of Loss Reinsurance

Per-Risk XOL

The attachment point and limit apply to each individual risk — meaning each vehicle service contract or insured unit — rather than to a group of losses. A single policy that generates an unusually large repair claim on a high-value vehicle would trigger this layer, while routine smaller claims on other policies would not.

Per-Occurrence XOL

Here, the attachment and limit apply to total losses arising from a single event across multiple policies simultaneously. A hailstorm that damages a dealer's entire lot — triggering claims across multiple CPI or physical damage policies at once — is the classic example. The occurrence definition in the contract determines which losses count as a single event.

Catastrophe XOL

A specialized form of per-occurrence protection aimed at large-scale disasters. These treaties typically include an hours clause — a defined time window (often 72 or 168 hours, as confirmed in a 2024 HFW analysis) during which related losses are grouped as arising from a single catastrophe. More relevant to large property and casualty insurers, but worth understanding structurally.

Aggregate XOL (Stop-Loss)

This is the type most relevant to dealer-owned reinsurance programs. Rather than responding to any single large event, aggregate XOL triggers when cumulative claims over an entire policy period — typically one year — exceed a set retention threshold.

The RAA defines it as indemnifying the ceding company "when its total losses during a period exceed either a predetermined dollar amount or a percentage of the company's subject premiums." The structure is designed to prevent wide swings in annual loss ratios — exactly the exposure that erodes profit in a dealer-owned program.

For dealers, that means protection against the risk that matters most: not a single catastrophic claim, but a sustained pattern of elevated losses across the full year. Aggregate XOL guards against:

- High VSC claim frequency that outpaces premium collections

- GAP settlement volume that exceeds projected annual exposure

- Mechanical breakdown patterns across a BHPH portfolio that steadily drain reserves

A Note on Terminology

You may encounter "XOL," "XL," and "XS" used interchangeably depending on the market. Lloyd's and the London Market tend to use XL and XS; U.S. participants more commonly write XOL. When reviewing reinsurance contracts, confirm which abbreviation your counterparty uses — the mechanics are identical, but contract language should match consistently throughout.

Excess of Loss vs. Other Reinsurance Structures

XOL vs. Quota Share

| Feature | Quota Share | Excess of Loss |

|---|---|---|

| Premium sharing | Fixed % ceded on every risk | Cedent pays a separate XOL premium |

| Loss sharing | All losses split from dollar one | Reinsurer only pays above retention |

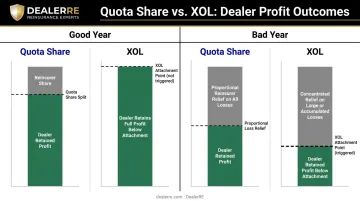

| Good-year impact | Reinsurer takes a share of profit | Cedent keeps all profit below attachment |

| Bad-year protection | Proportional relief on all losses | Concentrated relief on large/accumulated losses |

The Insurance Information Institute captures the core trade-off: in quota share, "the reinsurer and the primary company share both the premium from the policyholder and the potential losses." In XOL, the cedent pays a calculated fee and the reinsurer only pays excess losses.

For dealers, this distinction is significant. Quota share means giving up a percentage of underwriting profit every year, including the good ones. XOL lets the dealer keep full profit in normal years while limiting exposure in bad ones — provided the dealer has sufficient capital to absorb the retention.

XOL vs. Surplus Share

Surplus share is a proportional treaty where the reinsurer assumes risk in proportion to the amount by which a risk exceeds the cedent's net retention capacity. It's more common in property lines and less applicable to F&I product portfolios, where per-occurrence and aggregate XOL structures are the better fit for F&I programs.

That gap in applicability points directly to when XOL earns its place.

When XOL Is the Right Structure

XOL suits programs where the cedent wants to protect earnings from outsized losses — either large single-loss events or aggregate bad years — while retaining full underwriting profit when losses stay within normal ranges. For dealer-owned reinsurance companies, that's exactly the structure the economics call for.

Why Auto Dealers Should Understand Excess of Loss Reinsurance

Dealers who operate their own reinsurance company aren't just selling F&I products — they're functioning as insurers. That means carrying real underwriting risk, and understanding XOL is what separates dealers who manage that risk deliberately from those who discover their exposure only after a damaging claims year.

The Real Downside Scenario

VSC programs can produce severe loss volatility. Actuarial research published in the CAS journal Variance documented loss ratios above 200% in certain extended service contract program contexts. That figure illustrates how dramatically claims can deviate from projections. Add GAP settlements during a period of elevated vehicle depreciation or a BHPH book with higher mechanical breakdown frequency, and cumulative annual losses can erode years of built-up profit quickly.

Aggregate XOL protection directly addresses this scenario. It doesn't matter whether the losses came from one large event or dozens of routine-but-elevated claims — once the aggregate retention is hit, the reinsurer covers the remainder up to the defined limit.

How the Admin Obligor Structure Connects

In the admin obligor structure that DealerRE helps dealers build, the dealer's reinsurance entity is backed by an A-rated carrier. That backing provides a fundamental layer of protection: if the reinsurance company cannot meet its financial obligations, the ultimate liability for claim payments rests with the direct writing insurance company. The dealer's exposure is limited to formation costs plus accumulated earnings.

DealerRE's full-service administration also includes performance reports and financial analysis, giving dealers visibility into how their program is performing against projections. That ongoing monitoring enables early recognition of an adverse loss year before it becomes a capital problem.

Asking the Right Questions

Dealers who understand XOL concepts are better positioned to evaluate any reinsurance program proposal on its merits. Key questions worth asking:

- Does the program include aggregate XOL (stop-loss) protection, and at what retention level does it trigger?

- What is the annual limit, and is it sufficient to cover a realistic worst-case claims year?

- Are reinstatements available if the limit is exhausted before year-end?

- Who holds the XOL contract — the fronting carrier, the administrator, or the dealer's own reinsurance entity?

Dealers who can't answer those questions are relying on trust rather than oversight. Understanding the structure is what makes it possible to hold a program — and its administrator — accountable.

Frequently Asked Questions

What does XS mean in insurance?

"XS" stands for "excess" — it refers to coverage that only applies to losses above a defined threshold. In reinsurance contexts, XS, XL, and XOL are used interchangeably across different markets to describe the same excess of loss structure.

What is the difference between excess of loss reinsurance and quota share?

Quota share splits every premium and every claim proportionally between cedent and reinsurer from the first dollar. XOL only involves the reinsurer when losses exceed a defined retention. XOL lets the cedent keep more profit in good years but requires sufficient capital to absorb losses up to the attachment point.

What is an attachment point in excess of loss reinsurance?

The attachment point is the loss threshold at which the reinsurer's obligation begins. The cedent pays all losses below this amount; the reinsurer covers losses above it, up to the defined limit. It is also called the retention or, in some markets, the priority.

What are the main types of excess of loss reinsurance?

There are three primary forms:

- Per-risk XOL — responds to a single large individual risk loss

- Per-occurrence XOL — responds to multiple losses from one event

- Aggregate XOL / stop-loss — responds when total losses for a period exceed a cumulative threshold

How does excess of loss reinsurance apply to dealer-owned reinsurance programs?

Aggregate XOL protection can cap a dealer's downside in a high-claims year by covering cumulative losses once they exceed the annual retention. Well-structured programs typically include this layer so dealers retain underwriting profits in normal years while carrying defined protection against adverse claims periods.

Is excess of loss reinsurance the same as stop-loss reinsurance?

Stop-loss is a form of aggregate XOL. Both respond when total losses over a period exceed a retention threshold, but "stop-loss" specifically emphasizes capping cumulative annual losses rather than any single large event. The terms are often used interchangeably in dealer reinsurance contexts.