Portfolio reinsurance is the mechanism that changes that equation. It's the foundational concept behind dealer-owned reinsurance programs, and understanding it clearly is the first step toward deciding whether owning that second profit layer makes sense for your dealership.

This article explains what portfolio reinsurance is, defines the key terms you'll encounter, walks through how it works in practice, and connects those concepts directly to the F&I programs dealers run every day.

TL;DR

- Portfolio reinsurance transfers an entire block of insurance policies — including future claim obligations and associated premiums — from one insurer to a reinsurer

- In dealer F&I, a dealer-owned reinsurance company assumes the risk of products sold at the dealership and keeps the underwriting profits

- Core terms: ceding company, reinsurer, reinsurance treaty, unearned premium reserve (UPR), and loss ratio

- Average F&I gross profit per vehicle retailed was $2,515 in Q2 2025 — and third-party providers are capturing underwriting profit on top of that

- Dealer-owned programs let you keep both layers

What Is Portfolio Reinsurance?

The Reinsurance Association of America defines portfolio reinsurance as "the transfer of portfolio via a cession of reinsurance; the reinsurance of a runoff. Only policies in force are reinsured, and no new or renewal business is included."

Put simply, an insurer takes an entire existing book of policies — a portfolio — and hands both the obligations and the associated premium income to another company, the reinsurer. That reinsurer steps fully into the original insurer's position.

The word "portfolio" here means exactly what it means in finance: a collection. In insurance, it's a defined group of policies treated as a single block rather than as individual contracts.

Two Distinct Uses of the Term

Portfolio reinsurance shows up in two contexts:

- Traditional use — An insurer exits a market segment, discontinues a product line, or winds down a book of business. They transfer the in-force policies to another carrier so policyholders maintain coverage.

- Dealer-owned use — A dealer establishes their own reinsurance company that assumes the risk on F&I products sold at the dealership. The dealer's company steps into the role of the reinsurer, taking on claim exposure and retaining the underwriting profit when claims come in below the reserve.

This article focuses on the second use. The underlying mechanics are the same in both cases: risk and premium obligations move from one party to another. The difference is motivation — profit capture rather than market exit.

How It Differs from Standard Reinsurance

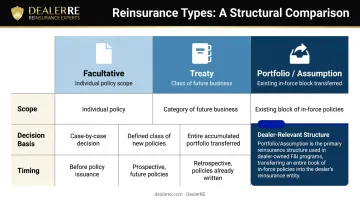

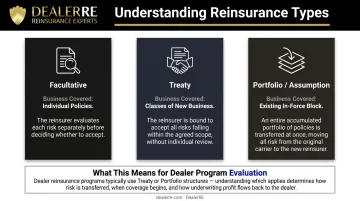

| Type | Scope | What Transfers |

|---|---|---|

| Facultative | Individual policy | Reinsurer decides case by case |

| Treaty | Category of future business | Defined class of new policies |

| Portfolio/Assumption | Existing block of in-force policies | Entire accumulated portfolio, no new business |

Facultative and treaty reinsurance are indemnity arrangements — the original insurer remains liable to policyholders. Portfolio reinsurance (also called assumption reinsurance) effects a novation (a formal substitution of one party for another): the assuming insurer becomes directly liable, and the original insurer's obligations are extinguished.

Key Terms in Portfolio Reinsurance You Need to Know

These terms appear in every reinsurance program structure. Understanding them helps you evaluate programs and ask better questions.

Ceding Company (Cedant)

The original insurer that transfers — "cedes" — risk and premium to the reinsurer. In a dealer F&I context, this is typically the third-party administrator or warranty provider who issued the original policies — and the party ceding business once a dealer transitions to their own reinsurance structure.

Reinsurer (Assuming Company)

The entity that accepts transferred risk in exchange for the associated premiums. In dealer-owned programs, this role shifts from a third-party carrier to the dealer's own reinsurance company — which means claim exposure, and the profits from managing it well, now belong to the dealer.

Reinsurance Treaty

The formal contract governing the arrangement. It defines which risks are covered, what percentage of premiums transfers, how claims are processed and paid, and the responsibilities of each party. This document is the legal foundation of any reinsurance program.

Unearned Premium Reserve (UPR)

The insurer holds premiums in reserve for coverage not yet delivered. The NAIC defines unearned premium as "the amount of premium for which payment has been made by the policyholder but coverage has not yet been provided."

These funds sit on the balance sheet as a liability — a real future obligation. Regulatory rules restrict how they can be invested. In DealerRE's structure, UPR funds are held in trust and invested in government bonds, with investment income flowing to the dealer's reinsurance company rather than a third party.

Loss Ratio

For dealer-owned programs, the loss ratio is the number that determines how much surplus builds in your reinsurance company. It's the ratio of claims paid to premiums collected — a 60% loss ratio means 60 cents of every premium dollar went to claims, and **40 cents is potential underwriting profit**.

Well-managed F&I portfolios in dealer-owned structures often target loss ratios in the 40–60% range. Every point below that threshold is profit your company retains — not a margin that flows to a third-party administrator.

How Portfolio Reinsurance Works Step by Step

The Basic Premium-Reserve-Claims Cycle

- Premiums collected — Policyholders (or vehicle buyers) pay premiums for F&I coverage. Those funds go into a reserve account.

- Claims paid from reserve — When a covered event occurs (a mechanical breakdown, a total loss), money is paid from the reserve to cover the repair or balance.

- Surplus accumulates — If premiums collected exceed claims paid over the policy period, the remainder is underwriting profit.

In a conventional third-party program, step three benefits the warranty company or insurance provider. In a dealer-owned program, it benefits the dealer.

The Transfer Mechanism

In a portfolio reinsurance transaction, the ceding company hands over:

- All current reserve balances

- Future premium streams from in-force policies

- Responsibility for paying any outstanding or future claims

The reinsurer formally steps into the ceding company's position. After that, the reinsurer holds both the liability and the financial upside — including any underwriting profit that builds over time.

What Happens to Policyholders

Customers' coverage terms remain unchanged. The NAIC Assumption Reinsurance Model Act requires that policyholders be notified of any transfer via first-class mail, with clear disclosure of their right to reject the transfer.

If a policyholder continues paying premiums to the assuming insurer, consent is legally established. The obligation to honor their claim simply shifts to the new party.

The Dealer-Owned Structure in Practice

DealerRE helps dealers establish what's called an admin obligor reinsurance company. The structure works like this:

- The dealer creates their own reinsurance company

- An A-rated fronting insurer underwrites and issues the F&I products (vehicle service contracts, GAP, CPI, ancillary products)

- The dealer's reinsurance company reinsures those products — assuming the claim risk

- Premium funds are held in a U.S.-based trust account under a formal Trust Agreement

- Claims are paid from that trust; if claims come in below reserves, the surplus belongs to the dealer's company

If the dealer's reinsurance company cannot meet its financial obligations, the direct writing insurance company bears the ultimate liability — which limits the dealer's exposure to formation costs and accumulated earnings.

Portfolio Reinsurance for Auto Dealers: The F&I Connection

The Traditional Dealer Problem

Most dealers selling third-party F&I products earn a front-end margin at the point of sale. What they don't see is what happens after: the warranty company or insurance provider collects the premiums, manages the claims, and keeps whatever is left over when the policy term expires.

Third-party providers wouldn't continue doing business with dealers if they weren't profitable. The F&I product space is a $35 billion industry at retail for vehicle service contracts alone. The underwriting margin that sustains that industry largely comes from dealer-sold volume.

What Dealer-Owned Reinsurance Changes

Instead of the third party holding the risk and keeping the profit, the dealer's own reinsurance company takes on the portfolio-level risk — and receives the financial upside when claims come in below reserve expectations. The dealer keeps the same front-end margin they were earning before. They also capture the underwriting profit they were previously sending out the door.

DealerRE has helped over 400 auto dealers across the country establish and manage their own admin obligor reinsurance companies. Their programs cover the full F&I product range:

- Vehicle service contracts and extended warranties

- GAP (Guaranteed Asset Protection)

- Collateral Protection Insurance (CPI) and Debt Cancellation Coverage

- Ancillary products: tire and wheel, windshield repair, door ding protection, theft protection

- Certified Pre-Owned warranty programs (DealerRenew Certified)

Strategic Uses for Reinsurance Profits

Accumulated underwriting profits in a dealer's reinsurance company aren't just passive income. They're flexible capital with real-world applications:

- Funding the dealer principal's retirement

- Building succession capital for next-generation ownership transfers

- Creating deferred compensation plans for key employees

- Reinvesting directly into dealership operations

- Personal wealth-building: real estate, education funding, and other investments

The tax-advantaged structure that makes dealer-owned reinsurance possible has been in place for nearly 40 years, originating in Reagan-era legislation — a proven framework with decades of dealer adoption behind it.

Portfolio Reinsurance vs. Related Concepts

Understanding how portfolio reinsurance compares to other structures helps you evaluate any program proposal on its actual terms.

Quota Share vs. Portfolio Reinsurance

Quota share is an ongoing proportional arrangement where a fixed percentage of premiums and claims on new business is shared with a reinsurer from day one. The split is continuous and applies to future production.

Portfolio reinsurance transfers an existing, accumulated block of in-force policies in a single transaction. In practice, once a DealerRE admin obligor program is established, the ongoing arrangement operates closer to a quota share structure: premiums from new F&I sales flow to the dealer's reinsurance company on a go-forward basis as contracts are written.

Excess of Loss vs. Portfolio Reinsurance

Excess of loss is non-proportional: the reinsurer only pays claims above a defined retention threshold. It doesn't share in routine claims — protecting against catastrophic loss spikes rather than everyday exposure.

Portfolio reinsurance transfers full liability on a defined existing block.

These aren't mutually exclusive. An excess of loss layer can be added on top of a proportional dealer program to protect against scenarios where claim frequency or severity dramatically exceeds expectations, providing a secondary protection layer when both frequency and severity push beyond what the base program was designed to absorb.

Facultative vs. Treaty vs. Portfolio Reinsurance

| Type | Business Covered | Decision Point |

|---|---|---|

| Facultative | Individual policies | Reinsurer evaluates each risk separately |

| Treaty | Classes of new business | Reinsurer bound to accept all within scope |

| Portfolio/Assumption | Existing in-force block | Entire accumulated portfolio transferred at once |

When evaluating any dealer participation program, the structure type determines where profits flow, who carries claim exposure, and what happens to reserves if the program terminates. A proportional arrangement means shared upside and shared risk. A non-proportional layer means you absorb predictable losses and only hand off the catastrophic tail. Knowing which one you're being offered changes every conversation about program economics.

Frequently Asked Questions

What is portfolio reinsurance?

Portfolio reinsurance is the transfer of an entire block of existing insurance policies (including future claim obligations and associated premiums) from one insurer (the ceding company) to a reinsurer. The reinsurer assumes full responsibility for honoring policyholder claims under those policies.

Is portfolio reinsurance still used?

Yes. AXIS Capital disclosed a Loss Portfolio Transfer reinsurance agreement executed in December 2024. In the dealer space, the admin obligor reinsurance structure, which operates on the same core mechanism, has been in use for nearly 40 years.

How does portfolio reinsurance differ from traditional insurance?

Traditional insurance is a contract between an insurer and a policyholder. Portfolio reinsurance is a business-to-business transaction where one insurer transfers liability on a block of existing policies to another company. The reinsurer doesn't sell directly to consumers or interact with the original policyholders — it assumes the financial obligations behind the scenes.

What is the difference between portfolio reinsurance and quota share reinsurance?

Quota share applies to new business going forward on a percentage-split basis, with premiums and claims shared continuously as new policies are written. Portfolio reinsurance transfers an existing, accumulated block of policies in a single transaction — one is a recurring arrangement, the other a clean, one-time handoff.

Can auto dealers use portfolio reinsurance to improve profitability?

Yes. By establishing a dealer-owned reinsurance company, dealers assume the risk of their F&I portfolio and capture underwriting profits that would otherwise stay with a third-party administrator or warranty provider. The dealer retains existing front-end margins while adding the underwriting profit layer on top.

What happens to customers when their policies are transferred through portfolio reinsurance?

Customers' coverage terms remain unchanged, and they receive written notice of the transfer with the right to reject it. If they continue their coverage, the assuming insurer steps into the original insurer's position and honors all claims under the same terms.