F&I now generates 73% of total dealership profit, up from 56% just a year prior. That makes the underwriting margin on F&I products the single largest financial lever most dealers aren't controlling.

This guide breaks down reinsurance underwriting in plain terms — what it is, how it works inside a dealer-owned structure, which factors drive the numbers, and where the profit actually goes when you own the reinsurance company.

TL;DR

- Reinsurance underwriting evaluates and prices risk to determine who keeps the profit between premiums collected and claims paid

- In a dealer-owned program, the dealer's reinsurance entity sits on the reinsurer side, keeping underwriting profit in-house

- Key underwriting inputs include vehicle age and mileage, product type, buyer profile, and the dealer's historical loss ratio

- Treaty/quota share is the standard dealer program structure: set up once, it automatically covers contracts as they're written

- Dealers who understand underwriting price F&I products more accurately and build stronger long-term profit from their reinsurance program

What Is Reinsurance Underwriting?

The Basic Mechanics

The NAIC defines reinsurance as a contract in which a reinsurer agrees to indemnify an insurer for a specified share of losses (essentially, insurance for insurance companies). When a primary insurer issues a policy to a customer, it assumes financial responsibility for future claims. By transferring (or "ceding") a portion of that liability to a reinsurer, the primary insurer reduces the capital it must hold and frees capacity to write more business.

The underwriting piece is what happens before any coverage is issued. It's the process of evaluating whether to accept transferred risk, at what price, and under what terms. Claims adjudication is the separate process that happens afterward: evaluating and paying claims once coverage is active. Both affect profitability, but underwriting is where the margin is set.

Underwriting Profit: The Number That Matters

The NAIC defines underwriting profit specifically as what remains after deducting losses and expenses from earned premiums — excluding investment income. That distinction matters. Underwriting profit is the pure risk-transfer margin: premiums in, claims and admin costs out, difference kept.

That margin doesn't disappear when it flows through a dealership — it just goes to whoever controls the underwriting. When a dealer sells an F&I product through a third-party provider, that provider is doing the underwriting. They decide which vehicles qualify, at what price, and how claims will be managed. And they keep the underwriting profit.

In a dealer-owned reinsurance structure, those decisions — and that profit — stay with the dealer. The core advantage breaks down simply:

- The dealer sets underwriting criteria for their specific customer base

- Premium income accumulates inside a dealer-controlled reinsurance entity

- Claims are managed according to the program's design, not a third party's margin targets

- Underwriting profit is retained rather than paid out to an outside provider

If your warranty provider weren't profitable on your book of business, why would they keep doing business with you? That's the question worth sitting with — because the answer points directly to where the money is going.

How Reinsurance Underwriting Works in a Dealer-Owned Structure

The Transaction Flow

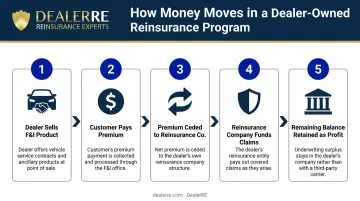

In a dealer-owned reinsurance program, the basic money flow looks like this:

- Dealer sells an F&I product — VSC, GAP, ancillary coverage

- Customer pays a premium — collected at point of sale

- A portion of that premium is ceded to the dealer's own reinsurance company

- The reinsurance company funds claims from the accumulated premium pool

- Remaining balance after claims and costs is retained as profit by the dealer's entity

The dealer still earns the same front-end gross they earned before. The difference is that the underwriting profit — which previously flowed to the third-party administrator — now stays within the dealer's own company.

The Admin Obligor Structure

DealerRE builds programs using an admin obligor structure, where the dealer's reinsurance company is formally positioned as the obligor on F&I contracts. This means the dealer's entity retains financial upside — both underwriting profit and investment income on premium reserves — while being backed by A-rated insurance carriers for security and regulatory compliance.

That positioning also limits the dealer's liability to formation costs plus accumulated earnings. If the reinsurance entity can't meet obligations, the direct writing insurance company carries the ultimate liability — so the dealer captures the financial upside while the A-rated carrier backstops the risk.

The Feedback Loop

That structural control extends beyond finances. When dealers own the reinsurance function, claims data feeds directly into business decisions rather than disappearing into a third party's reporting system.

DealerRE provides monthly financial statements and performance reports detailing all reinsurance operations activity. Their administrator monitors claims losses and projects performance through contract earn-out. That ongoing visibility creates a direct connection between how the dealer manages F&I sales quality and how the reinsurance program performs over time.

In practice, this means:

- Low loss ratio — the dealer may qualify for improved program terms over time

- Claims running high — early warning flags the issue before it compounds across multiple contract years

- Consistent performance data — builds a track record that strengthens the dealer's negotiating position with administrators

Key Factors Evaluated in Reinsurance Underwriting

When a program administrator evaluates a dealer's book of business, several inputs drive the underwriting assessment:

Vehicle and Product Eligibility

- Vehicle age and mileage directly affect expected claim frequency — older, higher-mileage inventory carries more risk

- Make and model reliability profiles influence coverage tier and pricing

- Product type matters: a VSC on a 90,000-mile used vehicle prices differently than GAP on a near-new franchise unit

Actuarial research shows that for used vehicles, approximately two-thirds of total losses emerge by the time only half the contract term has elapsed , a pattern that differs sharply from new-vehicle claims, which cluster near the end of the manufacturer's warranty period. This timing difference directly affects how reserves are structured.

DealerRE offers VSC programs for dealers across the full inventory spectrum — from late-model, low-mileage vehicles to high-mileage units exceeding 90,000 miles — with coverage terms structured to match the vehicle profile.

Buyer Profile and Financing Structure

For BHPH dealers especially, the relationship between vehicle type and customer payment behavior is a core underwriting consideration. A vehicle that breaks down stops generating payments. That connection means:

- Vehicle reliability is both a claims risk and a collections risk

- Financing structure and LTV ratios influence GAP exposure

- Customer profile informs expected claims frequency across the reinsurance pool

These factors help underwriters price risk accurately, which keeps the reinsurance pool financially sound for every dealer in the program.

Historical Loss Ratios

A dealer's claims track record is among the most influential inputs. The loss ratio (claims paid divided by premiums earned) tells the underwriter whether the existing portfolio is performing as priced or running above expected levels.

State insurance departments have historically used a 50% loss ratio as a regulatory benchmark for evaluating whether premiums charged are reasonable relative to benefits provided. Actual dealer program loss ratios depend on vehicle mix, coverage terms, claims management, and program maturity. Tracking this number consistently matters , and DealerRE's monthly reporting tracks it consistently.

Rising repair costs add further pressure: auto repair costs have increased more than 20% due to parts shortages and labor demand, which means programs written at pre-inflation pricing carry higher claim severity than originally modeled.

Portfolio Volume and Product Mix

Higher-volume programs generate more predictable aggregate loss patterns. A diversified product mix (VSCs alongside GAP, tire and wheel, windshield, and other ancillary products) reduces concentration risk and smooths overall portfolio performance. GAP penetration has reached 35.39% industry-wide, making it a meaningful component of any dealer's reinsurance portfolio.

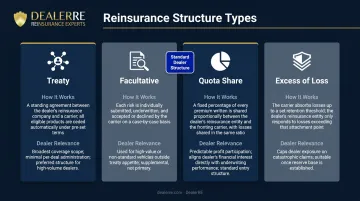

Types of Reinsurance Structures Dealers Should Know

| Structure | How It Works | Dealer Relevance |

|---|---|---|

| Treaty (Auto Standard) | Single agreement covers all qualifying contracts automatically | Set up once; coverage follows every contract written |

| Facultative | Each policy underwritten individually | Impractical for high-volume F&I operations |

| Quota Share (Proportional) | Dealer's reinsurer receives a fixed % of each premium; pays same % of each claim | Standard dealer structure; profit tied directly to portfolio performance |

| Excess of Loss (Non-Proportional) | Reinsurer only pays when losses exceed a threshold | More common in large institutional programs; less typical at dealer level |

Treaty reinsurance is what makes dealer-owned reinsurance scalable. The Insurance Information Institute confirms that treaty arrangements cover an entire book of business under agreed terms — no individual contract approval required. For a dealer writing F&I products daily, this is the only practical structure.

Quota share is the standard because it aligns the dealer's profitability directly with overall portfolio performance. The dealer's reinsurance company earns when the book performs well — and absorbs losses alongside the portfolio when it doesn't.

How Underwriting Profits Flow Back to the Dealer

When premiums exceed claims and administrative costs, the difference is underwriting profit. In a dealer-owned program, that money belongs to the dealer's entity — not a third-party warranty company using it to fund their own operations and investor returns.

What Dealers Do With It

Common uses for accumulated reinsurance profit include:

- Reinvesting in inventory or facility improvements

- Funding retirement vehicles

- Purchasing real estate

- Covering college education costs for children

- Expanding dealership operations

These are profits the dealer was always generating through F&I sales. The only change is where they land.

Investment Income on Top

Beyond underwriting profit, DealerRE's structure allows the dealer's reinsurance company to earn investment income on premium reserves held in trust. Funds are initially invested in conservative government instruments per regulatory guidelines. Once the balance sheet exceeds 125% of unearned premiums, excess funds can be directed more aggressively at the dealer's discretion.

The Long-Term Picture

Reinsurance profit compounds. A dealer who has operated their own reinsurance company for five or more years often finds it has become one of their most significant income sources — additive to, not a replacement for, core dealership operations.

In buy-sell transactions, dealer-owned reinsurance companies are treated as separately valued assets, requiring specialized assessment beyond standard dealership blue sky valuation. The reinsurance company isn't just generating annual income; it's building transferable enterprise value.

As one DealerRE client put it: "Without question, starting our own Reinsurance Company is one of the best decisions I ever made in the used car business."

Frequently Asked Questions

What is reinsurance underwriting?

Reinsurance underwriting is the analysis a reinsurer performs to decide whether to accept risk transferred from a primary insurer, and at what premium and terms. In the dealer context, this process determines how F&I product pricing is set and who captures the resulting profit margin.

What factors are evaluated during reinsurance underwriting for a dealership?

The main inputs are vehicle age and mileage, F&I product type, buyer profile, the dealer's historical loss ratio, and total portfolio volume. Together, these determine whether the transferred risk is acceptable and how it should be priced to keep the reinsurance pool financially sound over time.

What is an admin obligor reinsurance structure?

In an admin obligor structure, the dealer's own reinsurance company is named as the obligor on F&I contracts, backed by an A-rated insurer. This allows the dealer to retain underwriting profit and investment income while the A-rated carrier provides the financial security floor, limiting dealer liability to formation costs plus accumulated earnings.

How does reinsurance underwriting profit benefit auto dealers?

When total premiums exceed claims and administrative costs, the difference stays within the dealer's reinsurance entity rather than flowing to a third-party warranty provider. Capturing this margin can significantly improve long-term financial position and build separable business value.

What is the difference between treaty and facultative reinsurance?

Treaty reinsurance automatically covers all contracts within an agreed class without individual approval, making it the standard for dealer programs. Facultative reinsurance involves separate underwriting review for each policy. For dealers writing F&I products at volume, treaty is the only practical structure.