That's the part most dealers haven't examined closely enough.

Reinsurance isn't a single thing. It comes in distinct structures — treaty, facultative, proportional, non-proportional, dealer-owned — each designed to serve different goals. Understanding these differences is what separates dealers who passively participate in someone else's reinsurance program from those who own the economics themselves.

This article covers the main types of reinsurance, how they differ, and what each one means for your dealership's F&I strategy.

TL;DR

- Treaty reinsurance automatically covers an entire class of policies; facultative covers individual risks case-by-case — most dealer programs run on a treaty structure

- Proportional reinsurance splits premiums and losses by percentage; non-proportional only triggers the reinsurer when losses cross a set threshold

- Dealer-owned reinsurance (the admin obligor model) lets your dealership capture the underwriting profits that currently flow to third-party F&I providers

- Under IRC 831(b), programs under $1.2M in annual premiums can accumulate underwriting profits tax-free, with taxes applying only to investment income

- Dealers selling 30+ vehicles per month generally have sufficient volume to make a dealer-owned program financially worthwhile

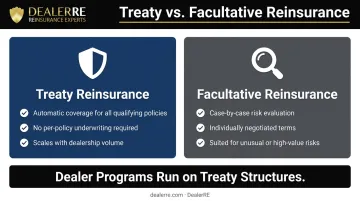

Treaty vs. Facultative Reinsurance: The Two Core Types

Almost all reinsurance contracts fall into one of two fundamental structures. Getting this distinction right is the foundation for understanding everything else.

Treaty Reinsurance

Treaty reinsurance is a standing agreement between an insurer and a reinsurer where coverage applies automatically to an entire defined class of risks over a set period. No individual policy gets submitted for approval — if it falls within the agreed scope, it's covered.

A dealer example: a reinsurer agrees to cover all vehicle service contracts written at a dealership during a given year. Every qualifying contract is included automatically, without separate negotiation.

Key advantages:

- Eliminates per-policy underwriting burden, keeping administration lean

- Predictable coverage for high-volume, consistent risk portfolios

- Scalable as dealership volume grows

The main trade-off is that because the reinsurer accepts all risks within the defined scope, the structure must account for the full range of exposures — including the weaker ones.

According to the Insurance Information Institute, treaty reinsurance is the dominant form of reinsurance by volume precisely because of this efficiency advantage.

Facultative Reinsurance

Facultative reinsurance works case-by-case. The reinsurer evaluates each risk independently and decides whether to accept or decline it. This structure handles large or unusual exposures that fall outside standard treaty parameters — a high-value commercial property policy or a specialty liability contract, for instance.

The strength is flexibility: coverage terms are negotiated specifically for the risk at hand. Each placement requires its own underwriting process, which adds administrative burden and slows execution.

That friction is exactly why facultative structures don't fit high-volume dealer operations. When you're writing dozens of service contracts a month, you need coverage that scales with deal flow — not one that stalls for individual negotiation each time.

Bottom line for dealers: Treaty is the everyday engine. Facultative is the exception tool for one-off risks. Dealer reinsurance programs are built on treaty-style arrangements because volume and consistency are what make them profitable.

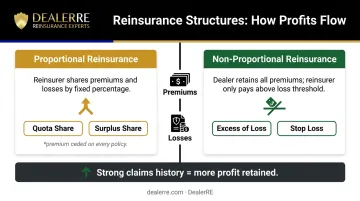

Proportional vs. Non-Proportional Reinsurance

Beyond treaty vs. facultative, reinsurance is also classified by how losses and premiums are actually divided. This distinction has direct implications for how much profit your dealership retains.

Proportional Reinsurance

In proportional reinsurance, the reinsurer receives a pre-agreed percentage of premiums and pays that same percentage of any claims. Two sub-types exist:

- Quota share: a fixed percentage of all risks — if the arrangement is 40%, the reinsurer gets 40% of premiums and covers 40% of every claim

- Surplus share: the insurer retains risks up to a set dollar limit; the reinsurer covers the amount above that retention

The strengths are simplicity and predictability. Insurers starting a new line of business often use proportional structures to share risk from day one.

The trade-off is significant: a meaningful slice of premium income goes to the reinsurer on every policy, whether claims materialize or not. That's profit you're ceding regardless of how well-controlled your loss experience is.

Non-Proportional Reinsurance

Non-proportional reinsurance flips the model. The insurer — or dealer — keeps all premiums and handles losses up to a defined threshold. The reinsurer only pays when losses exceed that threshold.

Two common forms:

- Excess of loss: reinsurer pays above a per-event or per-risk retention limit

- Stop loss (aggregate): reinsurer pays when the insurer's total loss ratio exceeds a set percentage over a defined period

Strong loss experience means you retain all the premium income without paying a proportional share to a reinsurer. The trade-off: if claims stay consistently below the threshold, the cost of reinsurance coverage can feel like unused overhead.

For dealers running their own programs: Non-proportional or hybrid structures can significantly increase profit retention when F&I products carry well-managed claims histories. The key variable is your loss experience. Dealers with controlled claims exposure — particularly on vehicle service contracts — can structure programs to retain substantially more underwriting income.

Other Key Reinsurance Types Worth Knowing

Three additional reinsurance structures come up regularly in dealer conversations. Knowing how they work helps you evaluate the carriers and program structures behind your own reinsurance company.

Catastrophe reinsurance protects against a surge of claims from a single large-scale event (a hurricane, earthquake, or widespread product failure). It's typically structured as excess-of-loss and is most relevant to large property/casualty carriers. Swiss Re estimated approximately $200 billion in global demand for property catastrophe reinsurance, with annual insured losses above $100 billion likely to persist — the scale of that exposure is precisely why reinsurers price tail risk so carefully and why A-rated backing matters for dealer programs.

Retrocession is reinsurance for reinsurers. When a reinsurer takes on risk from a primary insurer, it can pass part of that exposure to yet another reinsurer (the retrocessionaire). This layering is how the global market absorbs large concentrations of risk.

The result is a capital base of $769 billion in dedicated reinsurance capital as of 2024 — stable enough to support the A-rated fronting carriers that back dealer reinsurance programs.

Aggregate excess of loss protects against cumulative claims over a period exceeding a set amount, rather than responding to any single event. For dealers, this is relevant as a safety net against an unexpectedly bad claims year : you keep premiums and profits in good years without ceding proportional income, while the reinsurer absorbs aggregate losses that exceed your retention threshold.

Dealer-Owned Reinsurance: The Type Built for Auto Dealerships

Of all the reinsurance structures covered in this guide, one is designed specifically to redirect F&I profits back to the dealer.

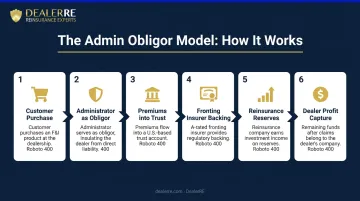

How the Admin Obligor Model Works

Dealer-owned reinsurance, specifically the admin obligor structure, is a distinct application of reinsurance tailored to the F&I space. The dealer forms a Producer-Owned Reinsurance Company (P.O.R.C.), structured as a standalone C Corporation separate from the dealership.

This entity assumes the financial obligation behind F&I products sold to customers — vehicle service contracts, GAP, collateral protection insurance, and ancillary products — while an A-rated fronting insurer provides the regulatory backing required by state insurance departments.

The mechanics:

- Customers purchase F&I products through your dealership's finance office

- The administrator (not the dealer) serves as obligor on the contract — this insulates you from direct customer liability

- Premiums flow into a trust account held by a U.S.-based trust company — no offshore accounts, no complex wire transfers

- The fronting insurer provides regulatory standing and consumer-facing insurance backing

- Your reinsurance company earns investment income on held reserves while waiting to pay claims

- When contracts earn out and claims come in below projections, the remaining funds belong to your company

If your reinsurance company cannot meet its obligations, the A-rated fronting carrier covers the remaining claims. The dealer's downside is limited to formation costs plus accumulated earnings.

The Profit Retention Advantage

Under a standard third-party F&I arrangement, you earn a front-end markup on each product sold. The third-party provider holds the risk, manages the reserves, and collects the underwriting margin when claims don't consume the full premium. That margin is the profit you're currently not capturing.

With dealer-owned reinsurance, you keep both the front-end gross profit and the underwriting profit on every contract your customers buy. As Mercer Capital notes, dealers without reinsurance structures "typically rely on commissions from third-party providers, thereby surrendering significant underwriting profit and investment income to unrelated parties."

F&I remains the most resilient dealership profit center — average F&I gross profit per vehicle retailed reached $2,505 in Q1 2025, approaching historic highs. The underwriting margin sitting inside those F&I products represents real money that either stays with you or gets handed to someone else.

Tax and Investment Benefits

The IRC 831(b) election delivers a significant tax advantage for dealers using this structure. Dealer-owned reinsurance companies with annual premiums below $1.2 million are taxed only on investment income — underwriting profits accumulate without being subject to income tax at the company level.

Beyond the tax treatment, reserve funds held in your trust account earn investment income. Once reserves exceed 125% of unearned premiums, excess funds can be invested more aggressively at the direction of company ownership.

You can direct that earned income toward:

- Real estate purchases

- Dealership reinvestment

- Children's education funding

- Other personal or business assets

DealerRE's Role

Since Tim Byrd founded the company in 1994, DealerRE has helped over 400 auto dealers establish and manage dealer-owned admin obligor reinsurance programs nationwide.

The service model covers the full lifecycle: company formation, F&I training, claims processing through administrator partner AVP, compliance management, legal forms and filings, tax return preparation, and monthly financial reporting. Dealers selling 30 or more vehicles per month typically have the volume to make these programs economically viable, though DealerRE evaluates each dealership individually.

How to Choose the Right Type for Your Dealership

The right reinsurance structure isn't the most complex one — it's the one that matches your volume, risk tolerance, and financial goals.

Questions to Ask Before Deciding

- How much risk do you want to retain vs. transfer? Proportional structures share exposure from dollar one. Non-proportional lets you keep more profit in exchange for bearing smaller losses yourself.

- What does your claims history look like? Dealers with controlled loss experience on F&I products are better positioned for structures that maximize profit retention.

- Do you have the volume? A minimum of 25–30 VSC contracts per month (roughly 300–350 annually) is the standard viability threshold for dealer-owned programs.

- What's your primary goal? Protecting against downside exposure calls for different structures than maximizing profit capture.

Common Mistakes to Avoid

- Defaulting to a third-party arrangement because it's familiar — without calculating the underwriting profit being left on the table

- Choosing a structure based on complexity rather than operational fit

- Underestimating the administrative requirements of running your own reinsurance company (this is why full-service administration matters)

- Entering a GAP reinsurance program without adequate volume — historically high loss ratios in GAP require a large book of business to absorb

The structure that fits your dealership comes down to your numbers: volume, loss history, and what you're trying to accomplish financially. If you're unsure where your program stands, that's exactly the conversation to have with a reinsurance specialist before committing to any structure.

Frequently Asked Questions

What is the difference between treaty and facultative reinsurance?

Treaty reinsurance automatically covers an entire class of policies under a standing agreement — no individual underwriting required. Facultative is negotiated separately for each specific risk. Dealer reinsurance programs run on treaty-style structures because they need coverage that scales automatically with F&I volume.

What is proportional reinsurance vs. non-proportional reinsurance?

Proportional arrangements split premiums and losses by a fixed percentage between insurer and reinsurer. Non-proportional means the reinsurer only pays when losses exceed a set threshold — the insurer keeps all premiums until that point. Non-proportional structures are more attractive for dealers with strong claims control since they retain more premium income.

What is admin obligor reinsurance?

Admin obligor reinsurance is a structure where a dealer-owned company assumes the financial obligation behind F&I products, backed by an A-rated fronting insurer. The dealership captures underwriting profits rather than paying them to a third-party provider. The fronting carrier handles regulatory compliance and consumer-facing backing.

Can an auto dealership own its own reinsurance company?

Yes. Dealers can own and operate their own reinsurance companies using a Producer-Owned Reinsurance Company (P.O.R.C.) structure. A program administrator like DealerRE handles setup, compliance, tax filings, and ongoing management.

What F&I products can dealer-owned reinsurance cover?

Dealer-owned programs typically cover vehicle service contracts, GAP, collateral protection insurance, debt cancellation coverage, and ancillary products like tire and wheel protection, windshield repair, door ding protection, and theft prevention — the same products dealers currently sell through third-party providers.

What is the difference between dealer-owned reinsurance and a third-party F&I provider?

Third-party providers let you earn a front-end markup, but they keep the underwriting profit. Dealer-owned reinsurance puts that margin back in your company, along with investment income on reserves — improving long-term F&I profitability on the same product volume.