That basic transaction is the foundation of a $900 billion global market (gross premiums, end of 2023). Behind every major hurricane payout or catastrophic loss event, there's almost always a chain of risk-sharing agreements working in the background.

This article breaks down how reinsurance works, the two primary structural types, and why these same principles matter well beyond traditional insurance — including for auto dealers who want to stop sending F&I profits to third-party providers.

Key Takeaways

- Reinsurance is a contract where a primary insurer (the cedent) transfers part of its risk to a reinsurer in exchange for a share of the premium

- The two primary types are treaty reinsurance (broad, automatic coverage) and facultative reinsurance (negotiated per policy)

- Reinsurance is structured either proportionally (shared percentages of premiums and losses) or non-proportionally (triggered only above a loss threshold)

- Reinsurance expands underwriting capacity, stabilizes income, and shields carriers against catastrophic losses

- These same risk-transfer principles underpin dealer-owned reinsurance programs in automotive F&I

How Does Reinsurance Work?

The Core Parties

Every reinsurance transaction involves two primary parties:

- The cedent (ceding company): The primary insurer that issues the original policy and transfers — or "cedes" — a portion of its risk. Per the Reinsurance Association of America, this is "the insurer which cedes all or part of insurance risk written to another."

- The reinsurer: The company that assumes that ceded risk in exchange for a corresponding share of the premium — and agrees to indemnify the cedent against covered losses.

The policyholder never interacts directly with the reinsurer — their contract stays with the primary insurer, and the reinsurance relationship operates entirely behind the scenes.

The Mechanics of Risk Transfer

Once a reinsurance contract is signed, the cedent's net liability — the amount it retains for its own account — decreases. Capital requirements are tied directly to risk exposure, so less net liability means less capital locked in reserves — freeing up capacity to write more policies.

As Swiss Re's Essential Guide to Reinsurance puts it: "Freeing up capital allows insurers to write more business, thus enabling economic growth and helping to create stability."

The reinsurer's obligation is triggered only when the primary insurer incurs a covered loss under the original policy — and only to the extent specified in the reinsurance agreement, with the cedent retaining some portion of that risk in every arrangement.

Retrocession and Reinsurance Brokers

Because reinsurers carry retained exposure of their own, risk distribution doesn't stop at one level. Reinsurers can purchase their own reinsurance — called retrocession — to further spread that exposure, particularly against catastrophic events. A retrocedent cedes risk to a retrocessionaire, continuing the chain.

Many reinsurance contracts don't get placed directly between cedent and reinsurer. Reinsurance brokers serve as intermediaries, negotiating contract terms on behalf of the ceding company and facilitating placement across one or more reinsurers. They're compensated by commission and generally represent the cedent's interests throughout the process.

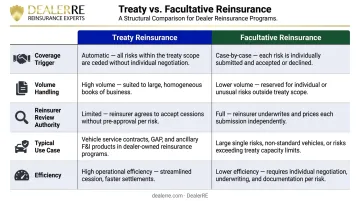

Treaty vs. Facultative Reinsurance: The Two Primary Types

Treaty Reinsurance

Treaty reinsurance is a standing agreement. The reinsurer automatically accepts all risks within a defined category — every auto policy, every homeowners policy, whatever the treaty specifies — without reviewing each one individually. Both parties are obligated to cede and accept under the terms.

This structure is built for volume. It's efficient, predictable, and well-suited to standardized, high-frequency risks. That efficiency explains why treaty reinsurance captures approximately 76% of the global reinsurance market by share.

Facultative Reinsurance

Facultative reinsurance works differently. Each individual policy or risk is negotiated and underwritten separately. The reinsurer retains the "faculty" — the option — to accept or decline each submission on its own merits.

This structure suits unusual, high-value, or complex risks that don't fit neatly within treaty guidelines. A commercial property with a unique construction type, a large fleet with atypical exposure — these are the kinds of risks that get handled facultatively.

How They Compare

| Dimension | Treaty | Facultative |

|---|---|---|

| Coverage trigger | Automatic, per standing agreement | Negotiated case by case |

| Volume handling | High — designed for bulk | Low — individual risks |

| Reinsurer review authority | Limited | Extensive |

| Typical use case | Standard, uniform portfolios | Large, complex, or unusual risks |

| Efficiency | High | Lower, but more control |

Some programs combine both: treaty coverage handles the routine book of business automatically, while facultative placements address risks that exceed treaty limits or fall outside defined categories. As Swiss Re notes, facultative is "mostly used by the primary insurer as a complement to obligatory reinsurance" — meaning the two approaches work together rather than in competition.

For businesses evaluating reinsurance structures, the choice depends on your portfolio composition. Standardized, recurring risks favor treaty. Anything unusual or outsized typically warrants facultative review.

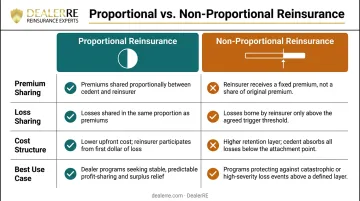

Proportional vs. Non-Proportional Reinsurance

Treaty and facultative describe how risks are transferred. The proportional vs. non-proportional distinction describes who pays what when a loss occurs — and that difference has direct implications for cost structure and cash flow.

Proportional Reinsurance

In a proportional arrangement, the reinsurer receives a fixed percentage of premiums and pays the same percentage of every claim — regardless of how large or small the loss is.

Two common subtypes:

- Quota share applies a fixed percentage uniformly across every policy in the portfolio. At 30%, the reinsurer collects 30% of every premium and covers 30% of every claim.

- Surplus share lets the cedent (the insuring party) set a defined retention per risk. Liability above that retention is transferred proportionally — useful for managing exposure on higher-value individual risks.

Proportional reinsurance is predictable and provides broad coverage. It's particularly effective for homogenous portfolios — motor insurance, for example — where risk characteristics are consistent across the book.

Non-Proportional Reinsurance

Non-proportional structures only activate above a pre-agreed loss threshold, called the retention or priority. Below that line, the cedent absorbs losses entirely. Above it, the reinsurer steps in — up to an agreed limit.

Two common subtypes:

- Excess of loss (XL) activates when a single loss crosses the cedent's retention threshold — typically used for per-risk protection or catastrophe coverage.

- Stop loss / aggregate XL triggers when total losses across a period exceed a set dollar amount or percentage of earned premiums — a safeguard against sustained, high-frequency loss years.

The Practical Trade-Off

| Factor | Proportional | Non-Proportional |

|---|---|---|

| Premium sharing | Yes — reinsurer receives share | No — cedent keeps all premium |

| Loss sharing | Every claim | Only above retention threshold |

| Cost | Higher routine cost | Lower routine cost |

| Best for | Stable, predictable portfolios | Catastrophic or tail-risk protection |

Neither structure is inherently superior — the right choice depends on whether the priority is steady cash flow management or protection against infrequent, high-severity losses. Most mature programs layer both to cover different parts of the risk curve.

Key Benefits of Reinsurance

Capacity Expansion

Without reinsurance, an insurer's ability to write policies is capped by its capital base. By ceding a portion of risk, the insurer reduces its net liability — which frees capital and enables it to accept more or larger risks than it otherwise could. This directly expands revenue potential without requiring additional equity.

Financial Stabilization

A single catastrophic event — a major weather loss, a surge in claims — can swing an insurer's results dramatically in a given year. Reinsurance absorbs that volatility, which helps carriers maintain the regulatory reserve levels and claims-paying consistency that policyholders depend on. For dealer-owned programs, that stability translates directly to predictable performance and protected reserves.

Access to Expertise

Reinsurers accumulate deep knowledge across markets, product lines, and regions. For a dealer setting up a reinsurance program for the first time, that expertise matters. Key advantages include:

- Access to proven pricing models and underwriting data

- Established risk management frameworks built over years of program experience

- Guidance on compliance, claims adjudication, and program structure

How Reinsurance Principles Apply to Auto Dealers

The mechanics described above aren't limited to traditional insurance carriers. The same logic (risk transfer, premium retention, reserve management) applies directly when auto dealers establish their own reinsurance companies to back the F&I products they sell.

The Profit Leak Problem

When dealers sell F&I products (vehicle service contracts, GAP, collateral protection, ancillaries) through third-party providers, underwriting profits flow out of the dealership. The provider collects premiums, pays claims, and keeps what's left. If third-party providers weren't profitable on dealer business, they wouldn't offer it.

Dealers selling more than 30 cars per month typically generate enough volume to make the math work the other way — by retaining those profits themselves.

How the Admin Obligor Model Works

In DealerRE's admin obligor (AO) reinsurance structure, the dealer establishes their own reinsurance company — a separate legal entity — that reinsures the F&I products sold through the dealership. Here's how it functions:

- Premiums from F&I product sales are ceded to the dealer's reinsurance company, held in a U.S.-based trust account

- Reserves are invested in conservative government instruments; once balance sheet cash exceeds 125% of unearned premiums, the owner can direct excess funds into more aggressive investments

- Claims are paid from the trust; the dealer's reinsurance company pays covered claims rather than a third party

- The A-rated backing carrier serves as the ultimate guarantor — if the dealer's reinsurance company can't meet its obligations, the carrier steps in, protecting the customer

The "admin obligor" distinction matters: a third-party administrator — not the dealer — serves as the contractual obligor on the F&I products. The dealer owns the reinsurance company and captures profits but isn't the direct contractual party on each customer contract. This structure limits liability while preserving profit retention.

The Financial Upside

The financial advantages stack up quickly:

- Underwriting profit retention — dealers capture what was previously flowing to third-party providers

- Investment income on reserves held in trust

- Tax planning advantages — qualifying reinsurance companies with under $2.2 million in annual net premiums may elect to be taxed only on investment income under IRC Section 831(b) (consult a qualified tax advisor for applicability to your situation)

- Earned income flexibility — profits from the reinsurance company can be reinvested in the dealership, used for real estate, or directed toward other long-term assets

DealerRE's Role

DealerRE has helped more than 400 auto dealers nationwide establish and manage their own admin obligor reinsurance programs since 1994. Their full-service model covers:

- Company formation and setup

- Compliance management and filings

- Claims adjudication through their administrator partner

- F&I training and staff development

- Monthly financial reporting and performance analysis

The program runs in the background — dealers stay focused on selling while DealerRE handles the infrastructure.

The F&I opportunity is real: publicly traded dealerships averaged $2,505 in F&I gross profit per vehicle retailed in Q1 2025, a 2.8% year-over-year gain. Dealers who also capture the underwriting layer on those deals are compounding that number — those who don't are funding someone else's profitability on every contract sold.

Frequently Asked Questions

How does a reinsurance company work?

A reinsurance company enters a contract with a primary insurer, assumes a portion of that insurer's policy risk in exchange for a share of the premiums, and pays claims when the conditions of the reinsurance agreement are triggered. The policyholder has no direct relationship with the reinsurer — only with the primary insurer.

How do reinsurance companies make money?

Reinsurers collect premiums from ceding companies, invest the reserves held against potential claims, and profit when actual losses come in below premiums collected. The model mirrors how primary insurers operate, except reinsurers work at a wholesale level, taking on portfolios of risk rather than individual policies.

What is the difference between treaty and facultative reinsurance?

Treaty reinsurance covers an entire category of policies automatically under a standing agreement. Facultative reinsurance is negotiated individually for each specific risk, giving the reinsurer the option to accept or decline each submission on its own terms.

What is proportional reinsurance?

In proportional reinsurance, the reinsurer receives a pre-agreed percentage of all premiums and pays the same percentage of all claims. The two main forms are quota share (a fixed percentage across all policies) and surplus share (covering the excess above the cedent's retention limit).

What is a ceding company in reinsurance?

A ceding company is the primary insurer that transfers (or "cedes") a portion of its insurance risk to a reinsurer. It retains the direct relationship with the policyholder and remains responsible for the full policy obligation, even after ceding part of the risk.

Can an auto dealer own their own reinsurance company?

Yes. Auto dealers can establish their own reinsurance company, typically structured as an admin obligor program backed by A-rated carriers. This lets dealers retain the underwriting profits from F&I products they sell instead of those profits going to third-party providers. Customers maintain the same coverage protections throughout.