Introduction

Front-end vehicle sales margins are under pressure. According to recent data, F&I gross profit per vehicle retailed reached $2,505 in Q1 2025, approaching historic highs—while new and used vehicle margins continue to shrink. Yet most dealers are still handing over a massive revenue stream to third-party F&I providers without realizing it.

The profits your warranty and insurance companies keep after paying claims? Those could belong to you instead.

Today, dealers earn a commission when they sell F&I products like vehicle service contracts and GAP insurance. But the real money, the underwriting profit left over after claims are paid, stays with the third-party provider. Dealer reinsurance changes that equation entirely.

This guide breaks down exactly what dealer reinsurance is, how it works, which structures fit which dealerships, and how to evaluate whether it's the right move for your operation.

TLDR: What You Need to Know About Dealer Reinsurance

- Dealer reinsurance lets auto dealers form their own captive company that earns underwriting profits on F&I products they already sell, keeping that money in-house instead of paying it to third parties.

- When claims are lower than premiums collected, the leftover funds stay in the dealer's reinsurance entity and can be invested, withdrawn, or used to fund business growth.

- The three main structures — CFC, Dealer Held Warranty Company, and Non-Controlled Foreign Corporation — each carry different risk, flexibility, and tax profiles.

- Benefits include profit capture, tax deferral, claims control, and long-term personal wealth building.

- Reinsurance is not just for large franchise groups—independent dealers and BHPH dealers can participate with the right program structure.

What Is Dealer Reinsurance?

Dealer reinsurance is a financial structure in which a dealer creates a separate legal entity, a captive reinsurance company, to assume the underwriting risk on the F&I products sold at their dealership. Instead of that risk (and profit) going to a third-party insurer, it stays with the dealer.

How It Differs from the Standard Commission Model

When a customer buys a vehicle service contract or GAP insurance, the dealer earns a flat commission. The insurance company collects the premium, pays claims, and pockets whatever is left. Reinsurance lets the dealer participate in that remaining profit.

F&I Products Typically Covered

Dealer reinsurance programs commonly cover:

- Vehicle service contracts (VSCs/extended warranties)

- GAP insurance

- Tire and wheel protection

- Dent and appearance coverage

- Other ancillary F&I products

The right product mix depends on each dealer's risk profile and historical loss ratios.

Historical Context

Dealer-owned reinsurance companies began in the 1950s with Texas-domiciled entities reinsuring credit life and disability insurance. By the 1960s, the model had moved to Arizona, which eventually housed over 1,000 such companies. As extended service contracts emerged, programs shifted to offshore domiciles like the British Virgin Islands and Turks and Caicos. Dealers have been using this structure for over 70 years.

The Admin Obligor Distinction

In an admin obligor structure, the dealer's reinsurance company is the contractual obligor on the F&I contracts, but it is backed and insured by an A-rated carrier. This provides the dealer with greater control and profit participation while maintaining consumer protection and regulatory compliance—and it is the model DealerRE specializes in.

How Does Dealer Reinsurance Work?

Here's how money moves through a dealer reinsurance program — from the moment a customer signs to the point where profit lands back in the dealer's pocket.

Step 1 — Customer Purchase

A buyer purchases an F&I product (such as a vehicle service contract) at the point of sale. They pay a premium that becomes the financial foundation of the reinsurance program.

Step 2 — Premium Allocation

The collected premium is divided among three uses:

- Administrative fees paid to the program administrator

- Compliance and risk management costs to keep the program in good standing

- Reserves deposited into the dealer's captive reinsurance entity

Step 3 — Ceding Risk to the Captive

The dealer formally transfers — or "cedes" — the net underwriting exposure (the financial risk of paying future claims) to their reinsurance company, which is typically domiciled offshore (such as Turks & Caicos) or through a domestic structure.

Step 4 — Claims Activity

As customers file claims over the life of their contracts, those claims are paid out of the reserves in the reinsurance entity. The dealer (or their administrator) has oversight of claims adjudication—meaning the dealer has direct input into how customer claims are handled.

Step 5 — Underwriting Profit

When total claims paid are less than total premiums collected, the difference is underwriting profit. That profit stays inside the dealer's reinsurance entity rather than flowing to a third party. Over time, this balance can grow substantially.

Step 6 — Investment Income

Between the time premiums are collected and claims are paid, the reserves are invested. Dealers can invest those reserves in assets such as equities, bonds, or real estate — compounding their reinsurance dollars on a tax-deferred basis.

Key Benefits of Owning Your Own Reinsurance Company

Capture 100% of Underwriting Profits

Instead of earning only a front-end commission while the third-party insurer keeps the remaining premium profit, the dealer's captive retains those profits.

Third-party warranty and insurance companies would not stay in business with dealers unless they were profitable. That inherent profit is available for dealers to capture by owning their own reinsurance company.

Tax Advantages and Deferral

Premiums are often treated as tax-deferred income—not taxed until claims are paid out or profits are distributed. Under Internal Revenue Code Section 831(b), qualifying small insurance companies can elect to be taxed only on taxable investment income in lieu of tax on premium income. Setting up reinsurance companies in tax-advantaged jurisdictions allows dealers to accumulate wealth more efficiently than taking taxable dealership distributions.

Beyond the financial upside, ownership also changes how dealers interact with their customers.

Control Over the Customer Experience

When the dealer's own entity manages claims, the dealer can ensure those claims are handled in a way that reflects well on the dealership. A poor claim experience with a third-party provider can cost the dealer a future vehicle sale—dealer-controlled claims handling strengthens customer loyalty and repeat business.

Income Diversification and Long-Term Wealth Building

Reinsurance profits are not directly tied to vehicle sales volume, providing a countercyclical income stream during slow sales periods. Earned income from the reinsurance company can be used for:

- Real estate investment

- Funding a child's college education

- Reinvesting into the dealership

- Purchasing equipment

- Retirement

Succession and Estate Planning

A captive reinsurance entity is a structured way to transfer wealth across generations in family-owned dealerships. Few dealers take advantage of this benefit, yet it's particularly valuable for multi-generational dealer groups or owners planning their exit strategy.

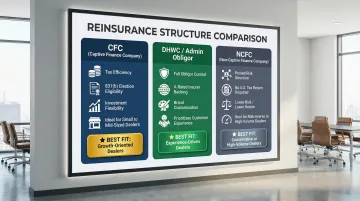

Types of Dealer Reinsurance Structures

Dealers can choose from three primary reinsurance structures, each with different levels of control, tax treatment, and risk exposure. The right fit depends on the dealer's risk tolerance, desired control, tax situation, and growth stage.

Controlled Foreign Corporation (CFC)

A CFC is taxed as a U.S. company but domiciled in an offshore country; all assets are held in U.S. financial institutions. Under IRC Section 957, a Controlled Foreign Corporation is any foreign corporation where more than 50% of the total combined voting power or total value of stock is owned by U.S. shareholders.

Key advantages:

- Flexibility to direct investments

- Ability to take loans against the account

- Use funds for capital improvements or floor plan

- Qualifies for IRS 831(b) election (excludes up to $2.8M annually in premiums from taxable income)

Best fit: Small to mid-sized dealers seeking tax efficiency and hands-on control

Dealer Held Warranty Company / Admin Obligor (DHWC)

The DHWC is an administrative corporation where the dealer (or dealer group) is the obligor—meaning the dealer's company is responsible for paying claims. A third-party administrator handles day-to-day operations, and the structure is treated as an insurance company for tax purposes.

DealerRE's admin obligor model backs the reinsurance company with A-rated insurers, providing security for both the dealer and their customers. Contracts can be highly customized with service tie-backs to the dealership.

Key advantages:

- Dealer retains full obligor status — maximum brand and claims control

- Backed by A-rated insurers for regulatory security

- Contracts customizable with direct service tie-backs to the dealership

- Structured as an insurance company for favorable tax treatment

Best fit: Dealers who want full control over the customer experience and the credibility of regulatory backing

Non-Controlled Foreign Corporation (NCFC)

The NCFC is domiciled offshore and claims are paid from offshore funds. It offers the least investment flexibility. The offshore domicile means premiums are subject to excise taxes, and dealers take profits as dividends (surplus).

Key trade-offs:

- Does not file an annual U.S. tax return

- Bypasses 831(b) premium limits

- Pools multiple dealers together to share risk

- Lowest risk but also lowest returns

Best fit: Dealers newer to reinsurance who prefer lower risk exposure, or larger operations that have scaled beyond 831(b) premium limits

Comparative Overview

| Structure Type | Ownership & Control | Tax & Regulatory | Best Fit |

|---|---|---|---|

| CFC | Dealer controls investments and claims | 831(b) election available; files U.S. tax return | Small to mid-sized dealers wanting tax efficiency |

| DHWC/Admin Obligor | Dealer is obligor; backed by A-rated carrier | Treated as insurance company for tax purposes | Dealers prioritizing customer control and branding |

| NCFC | Pooled with other dealers; limited control | No U.S. tax return; excise taxes apply | Risk-averse dealers or those exceeding 831(b) limits |

Common Misconceptions About Dealer Reinsurance

Misconception 1 — "Reinsurance isn't properly regulated"

The IRS previously identified micro-captive transactions as "transactions of interest" under Notice 2016-66 due to potential tax avoidance or evasion. The IRS finalized regulations in January 2025 that addressed this directly.

Those rules include a clear "Seller's Captive" exception for entities where at least 95% of business consists of issuing or reinsuring contracts purchased by unrelated customers in connection with products or services sold by the dealer.

Dealers who stay compliant face no unusual regulatory risk. An experienced administrator handles all legal forms, filings, tax returns, and renewals — keeping the dealer's workload minimal.

Misconception 2 — "It's only for large franchise dealerships"

Sales volume matters less than most dealers think. Independent dealers and Buy Here Pay Here (BHPH) dealers can and do benefit from reinsurance.

BHPH operators in particular can use admin obligor reinsurance programs to protect their vehicles from mechanical breakdown and offset insurance losses funded by their customer base. DealerRE works with dealers selling more than 30 cars per month — a threshold most active independent lots already clear.

Misconception 3 — "Managing a reinsurance company is too complex and time-consuming"

Setup work and some ongoing oversight are real — but the operational burden is far lighter than most dealers expect. Full-service administrators handle the heavy lifting, including:

- Compliance management and regulatory filings

- Claims adjudication

- Performance reporting and financial bookkeeping

- Tax return preparation and annual renewals

Dealers stay in control of their program without having to become insurance experts.

Is Dealer Reinsurance Right for Your Dealership?

Signs It's a Strong Fit

- You already sell F&I products and want to stop giving underwriting profits to a third party

- You have sufficient F&I volume to generate meaningful premiums (typically 30+ vehicle sales per month)

- You're interested in long-term wealth accumulation or tax efficiency

- You want more control over the customer experience after the sale

Signs to Evaluate Carefully

- Very low F&I volume

- Limited management bandwidth

- Strong preference for guaranteed short-term commissions over long-term profit accumulation

Risk tolerance also matters — DOWC structures offer more certainty, while traditional reinsurance carries more underwriting variability. Knowing where you fall on that spectrum shapes which program fits best.

How to Take the Next Step with DealerRE

DealerRE starts with a detailed analysis of your dealership's F&I volume, product mix, and current income to show exactly what a reinsurance program could return — before you commit to anything. With 28+ years of experience and over 400 dealers served nationwide, the setup and ongoing support are fully managed. That includes:

- Fast company setup with no hidden fees

- Full-service administration: training, claims adjudication, compliance, bookkeeping, and performance reporting

- Admin obligor programs backed by A-rated insurers

Call DealerRE at (804) 824-9533 to get a free analysis and see what your dealership could be keeping.

Frequently Asked Questions

What is dealer reinsurance?

Dealer reinsurance is a structure where an auto dealer creates their own captive company to retain the underwriting profits on F&I products they already sell, rather than allowing those profits to go to a third-party insurer.

How does auto dealer reinsurance work?

The customer pays a premium on an F&I product, that premium is allocated to reserves in the dealer's captive entity, claims are paid from those reserves, and any profit remaining after claims is the dealer's to keep and invest.

How do dealerships make money on extended warranties?

Dealerships earn a front-end commission when they sell a VSC through a third-party provider. With dealer reinsurance, they can also capture the underwriting profit (the funds left over after claims are paid), which is often significantly larger than the initial commission.

What is the difference between a vehicle service contract and insurance?

A vehicle service contract (VSC) is a service agreement that covers mechanical repair costs and is not technically insurance. GAP insurance is a true insurance product that covers the difference between a vehicle's value and the loan balance if the car is totaled.

Are dealerships self-insured?

Through a dealer-owned captive, dealers take on the underwriting risk for F&I products, similar in concept to self-insurance. In a properly structured admin obligor program, however, that captive is backed by an A-rated insurer, providing a financial safety net rather than pure self-insurance exposure.

Where do reinsurers get their money?

Reinsurers collect premiums from F&I product sales, hold those premiums as reserves, and earn underwriting profit when claims paid fall short of premiums collected. Investment income on those reserves adds an additional layer of return.

Ready to explore whether dealer reinsurance is right for your dealership? Contact DealerRE at (804) 824-9533 or visit their website for a free, no-obligation business analysis. With nearly three decades of experience, DealerRE has helped over 400 dealers recapture underwriting profits and build long-term financial strength.