Introduction

Extended warranties are among the highest-margin products in any F&I office—vehicle service contracts routinely generate $1,000 to $3,000 or more per deal. Yet most dealers only capture a fraction of that. The real profit isn't in the sale itself; it's in the underwriting profits that flow after the contract is written.

Dealers push extended warranties for good reason—the margins are real. The problem is that the largest slice of that profit typically flows to third-party administrators and warranty companies, not back to the dealership. This article walks through the full profit structure of vehicle service contracts and shows exactly how dealers can reclaim what they're currently leaving on the table.

TLDR

- Extended warranties deliver retail margins that frequently exceed 50%, making them one of the most profitable F&I products available

- Dealers earn upfront gross profit on every warranty sale, but this represents only the first of three potential profit layers

- Administrator income and reinsurance reserves (the second and third profit layers) flow to third-party companies unless the dealer owns a reinsurance structure

- Dealers without a reinsurance structure commonly surrender six figures in annual profit to external providers

- Owning a reinsurance company captures the full profit stack from every service contract sold

What Are Extended Warranty Profit Margins?

Defining the Vehicle Service Contract

In the dealership context, an "extended warranty" is actually a Vehicle Service Contract (VSC)—a distinction that matters legally and functionally. The Federal Trade Commission defines auto service contracts as optional agreements sold by vehicle manufacturers, dealers, or independent companies to perform or pay for specific repairs. Unlike manufacturer warranties included in the vehicle's base price, VSCs are purchased separately and cover mechanical repairs beyond the factory warranty period, typically through a third-party administrator rather than the manufacturer.

The Basic Profit Model

The standard VSC profit model works like this: the dealer sells the contract at retail price, pays a dealer cost to the administrator, and keeps the spread as gross profit. This markup is substantial. Industry data shows dealer markup typically accounts for 50% or more of a VSC's retail price.

For example:

- Wholesale cost to dealer: $1,000

- Retail price to customer: $2,000

- Dealer gross profit: $1,000 (50% margin)

Depending on pricing strategy, dealers may apply markups ranging from 50% to 200% above wholesale cost.

Why These Margins Matter

Extended warranty profit margins dwarf front-end vehicle gross profit—which explains why F&I managers are trained and incentivized to prioritize VSCs in every deal. New vehicle front-end gross averaged $3,284 in Q2 2025; used vehicle gross came in at just $1,642 in Q1 2025. A single VSC, by contrast, can add $1,000+ in pure gross profit per deal—with minimal negotiation resistance once financed into monthly payments.

Why Dealerships Push Extended Warranties So Hard

F&I Is the Primary Profit Engine

Front-end vehicle gross has faced years of compression due to market transparency, online pricing tools, and inventory shifts. That pressure has made F&I the dealership's primary profit center — F&I products now represent approximately 25% of total dealership gross profit, up from just 15% in 2009.

Public dealer groups demonstrate the profit potential. AutoNation reported F&I gross profit per vehicle retailed (PVR) of $2,891 in Q4 2025, up from $2,686 the previous year. The industry average sits lower — StoneEagle reported Q4 2025 F&I PVR at $1,995 — but F&I performance now determines dealership profitability.

Service Contract Penetration Drives Performance

VSC penetration rate — the percentage of deals that include a service contract — serves as a critical F&I metric tracked by managers and dealer principals alike. National service contract penetration averages approximately 47%, while top-performing dealerships (top 5%) reach about 84% penetration.

High penetration equals high per-vehicle revenue. When VSCs are rolled into monthly payments, sticker shock diminishes and the product becomes easier to sell — while the dealer still captures full gross profit.

The Compounding Financial Effect

Consider a realistic scenario:

- Dealership selling 100 units monthly

- 50% VSC penetration rate (50 contracts sold)

- $1,000 average gross profit per contract

- Monthly VSC revenue: $50,000

- Annual VSC revenue: $600,000

This represents substantial income from a single F&I product — and it's only the first profit layer. The financial incentive to sell VSCs aggressively is real, which is exactly why F&I managers are trained to close them using specific psychological techniques.

Sales Psychology and Information Asymmetry

F&I managers are trained to sell service contracts using three core psychological levers:

- Fear of repair costs — positioning VSCs against the prospect of a $3,000 transmission job

- Peace of mind messaging — framing the purchase as protection, not a transaction

- Loss aversion — the principle that people feel potential losses more acutely than equivalent gains, making "what if" scenarios highly effective

Dealers also hold a structural information advantage. They know claim probabilities and expected loss ratios; customers generally don't. Combined with the genuine complexity of modern vehicle repair costs, that asymmetry makes VSC sales consistently predictable — and consistently profitable.

Where the Profit Actually Goes: The Hidden Layers

The Three-Layer Profit Structure

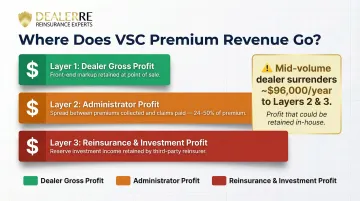

The gross profit a dealer keeps at point of sale is only Layer 1. It's often the smallest share of total economic value that contract generates. Most dealers are capturing just one-third of what's available.

Layer 1 — Dealer Gross Profit: This is the immediate markup between wholesale cost and retail price that the dealership keeps when the VSC is sold. This layer is visible, tracked, and celebrated in monthly F&I reports.

Layer 2 — Administrator Profit: The third-party VSC administrator collects the dealer cost (the "wholesale" price), manages the claims process, and retains the spread between premiums collected and claims paid. Industry loss ratios typically hover around 50-76%, meaning administrators retain 24-50% of every premium dollar after paying claims. When claims run low, those reserve balances grow — and the dealer sees none of it.

Layer 3 — Reinsurance/Investment Profit: Behind most VSC programs sits an insurance or reinsurance structure where unearned premium reserves are held and invested over time. These reserves generate investment income from bonds, equities, or other instruments. This "back-end" profit layer is retained by the third-party reinsurer, unless the dealer owns that reinsurance company outright.

The Retro Program Partial Solution

Understanding these three layers makes clear why retro programs exist — they're designed to give dealers a slice of what they're currently missing. Some dealers participate in retro arrangements that share a portion of Layer 2 profits back when claims experience is favorable. Retro programs help, but they have structural limitations:

- Dealers still don't capture the full reinsurance layer

- No control over claims reserves

- No access to investment income

- Limited to a percentage of underwriting profit, not 100%

Quantifying the Gap

According to Woodward & Associates, a prominent automotive accounting firm, dealers who don't own their reinsurance company miss out on incremental profits that "can amount to an annual six figure amount."

Here's what that looks like for a mid-volume dealer:

| Variable | Figure |

|---|---|

| VSCs sold per month | 20 contracts |

| Reserve per contract | $800 |

| Estimated claims rate | 50% |

| Underwriting profit per contract | $400 |

| Annual profit retained by third party | $96,000 |

That $96,000 stays with the warranty company. The dealer who sold every one of those contracts walks away with none of it.

How Dealer-Owned Reinsurance Unlocks the Full Profit Stack

The Dealer-Owned Reinsurance Model

Instead of paying third-party administrators and reinsurers to hold and profit from VSC reserves, dealers can establish their own reinsurance company that receives the unearned premium reserves from every service contract sold. This structure allows dealers to act as their own insurance company, capturing 100% of underwriting profits and investment income.

How the Structure Works

The money flow operates as follows:

- Dealer sells VSC to customer at retail price

- Dealer cost flows to the administrator for claims management

- Administrator fee is deducted for operational services

- Remaining reserves flow into the dealer's reinsurance company

- Claims are paid from the dealer's reinsurance company

- Remaining reserves and investment income accumulate as dealer profit

Key Financial Advantages

Controlling your own reinsurance company creates multiple profit opportunities across underwriting, claims, investment, and tax planning:

Underwriting profits stay with you. You retain 100% of the back-end profits that third-party warranty companies were quietly keeping — on top of your original F&I gross.

Claims control stays in-house. Managing claims directly eliminates friction with external providers who are incentivized to deny. You can route repairs back to your own service facility, keeping that revenue inside the dealership.

Investment income accrues to you. Premium reserves are invested per regulatory guidelines, generating returns on your capital. Those earnings belong to your reinsurance company — not a provider's balance sheet.

Tax treatment improves. Properly structured reinsurance companies can elect IRC 831(b) status for companies under $2.2 million in annual net premiums, providing favorable tax treatment on underwriting income.

Wealth-Building Beyond Operations

Accumulated reinsurance profits create flexibility beyond dealership operations. Earned income can be used to:

- Purchase real estate

- Fund college education for children

- Reinvest in dealership infrastructure

- Fund personal asset purchases outside the business

- Build a financial base that doesn't depend on daily operations

For dealers who've spent years feeding third-party providers, that accumulated capital can be substantial — and it's been sitting on someone else's books.

How DealerRE Can Help

DealerRE specializes in helping automotive dealers—franchise, independent, and BHPH—establish and manage their own admin obligor reinsurance companies, replacing third-party arrangements with dealer-owned structures that capture the full profit stack.

Comprehensive Admin Obligor Structure

DealerRE's admin obligor model means your dealer-owned reinsurance company serves as the obligor—the party responsible for paying claims—for the products it reinsures. Unlike traditional third-party arrangements where external companies control claims and keep profits, you own 100% of your reinsurance company.

It only reinsures business your dealership writes, so no other dealer's losses affect your profitability. The structure is backed by A-rated insurers, providing security and regulatory compliance while keeping you in full control.

Full-Service Management

DealerRE handles the complexity so you can focus on running your dealership:

- Legal setup and filings — Complete formation of your reinsurance company with all regulatory requirements

- Tax returns and compliance — Annual tax filing, Form 1120PC preparation, and IRC 831(b) election coordination

- Claims adjudication — Professional claims processing through Assured Vehicle Protection (AVP)

- F&I training — Comprehensive online and in-person training programs for your staff

- Performance analysis — Monthly financial statements and periodic operations review

- Ongoing renewals — License maintenance and regulatory updates

With 28 years in the field and 400+ dealers served nationwide, DealerRE brings deep operational experience to every program. The team works alongside vetted CPAs and legal counsel to keep your dealership and reinsurance program in full compliance.

Take the Next Step

If your dealership is still routing F&I profits to third-party warranty companies, a free analysis from DealerRE will show exactly what you're giving up. Call (804) 824-9533 or visit DealerRE.com to get started.

Frequently Asked Questions

What profit margin do dealers earn on selling extended warranties?

Dealer gross profit on VSC sales commonly ranges from 50% or higher depending on the contract sold and negotiated cost. Front-end gross is only the first profit layer, though. Dealer-owned reinsurance unlocks administrator and reinsurance profit layers that can double or triple total earnings per contract.

Do car dealerships make money on warranty repair work?

OEM warranty repair reimbursements depend on labor and parts rates negotiated with manufacturers, where profit margins are typically modest. Extended warranty contract sales operate differently—profit comes from front-end gross plus reinsurance reserves if the dealer owns that structure, not from hourly labor rates.

How profitable are car warranty companies?

Third-party warranty companies are highly profitable because they collect premiums, pay out only a fraction in claims (typically 50-76%), and retain investment income on reserves. Assurant's Global Automotive segment generated $4,203.8 million in net earned premiums in 2025, with improved loss experience driving profitability. Dealers who own their own reinsurance structure capture that same premium spread instead of paying it out to a third party.

How much profit does a new car dealer make per car?

Front-end vehicle gross has compressed significantly, with new vehicles averaging $3,284 per unit in Q2 2025 and used vehicles just $1,642 in Q1 2025. This compression makes F&I products like VSCs critical to overall per-unit profitability—F&I often contributes more net profit per deal than the vehicle sale itself.

What is a dealer-owned reinsurance company and how does it work?

A dealer-owned reinsurance company is a structure that allows dealers to receive and retain VSC premium reserves that would otherwise go to third-party reinsurers. Dealers profit from unearned premiums, investment income, and claims savings, capturing the full margin rather than just initial front-end gross.

Is it worth it for a dealership to set up its own reinsurance company?

For dealers with consistent VSC sales volume (typically 30+ vehicles monthly), the incremental profit from owning reinsurance can reach six figures annually. DealerRE has helped 400+ dealers set up and run these programs since 1994, managing all compliance, claims adjudication, and administration so dealers focus on selling.