Introduction

When a financed or leased vehicle is totaled or stolen, the insurance payout often falls thousands of dollars short of the remaining loan balance—leaving the customer on the hook for a car they no longer own. With total loss claims reaching a record 23.1% in 2025, nearly one in four claims puts buyers in exactly this position.

Two products exist to protect against this shortfall: gap insurance and loan/lease payoff coverage. They're often marketed as interchangeable, but a structural difference—a payout cap on loan/lease payoff coverage—can leave customers significantly underprotected at claim time.

For dealers offering these products through their F&I programs, the distinction matters. Presenting the wrong coverage—or failing to explain the payout cap clearly—sets up post-claim complaints and erodes customer trust.

Understanding the payout mechanics helps F&I teams set accurate expectations and match the right product to each financing situation.

TLDR

- Gap insurance covers the full difference between your loan/lease balance and the car's actual cash value (ACV) after a total loss — loan/lease payoff coverage works the same way but caps the payout at 25% of ACV

- Both require active comprehensive and collision coverage and apply only to total loss or theft, not repairs or partial damage

- Gap insurance is typically purchased at the dealership or through a lender and financed into the loan; loan/lease payoff is an add-on endorsement through your auto insurer

- If your potential shortfall could exceed 25% of ACV (large loan, low down payment, long term), true gap insurance offers stronger protection

- Dealers offering these products should understand payout mechanics to build customer trust and maximize F&I profitability

Gap Insurance vs. Loan/Lease Payoff: Quick Comparison

Both coverages share the same trigger—total loss or theft—and require comprehensive and collision insurance to be active. But they differ significantly in payout ceiling, purchase channel, and contract details.

| Feature | Gap Insurance | Loan/Lease Payoff |

|---|---|---|

| Coverage Amount | Covers the entire deficiency between loan balance and ACV; no percentage ceiling (some include deductible relief) | Typically capped at 25% of the vehicle's ACV; any shortfall beyond the cap is the borrower's responsibility |

| Purchase Channel | Offered by dealerships, lenders, credit unions; often financed into the loan | Sold as an endorsement added to an existing auto insurance policy; easier to modify or cancel |

| Deductible Treatment | Many contracts include deductible relief, meaning the deductible may also be covered | The borrower's standard deductible typically applies, reducing the net benefit |

| Cost | $400-$1,000+ as a financed flat fee | $20-$150 per year added to auto premium |

| Best For | Large loans, low down payments, long terms, high-depreciation vehicles | Modest, predictable shortfalls within the 25% cap |

Three differences in the table above carry more weight than they appear to at first glance.

Coverage amount is the most consequential. Loan/lease payoff's 25% cap sounds reasonable until a customer finances $40,000 on a vehicle that depreciates 30% in year one—the cap leaves a real gap in the gap coverage. True GAP insurance carries no ceiling, so the entire deficiency is settled regardless of how far the vehicle has fallen in value.

Purchase channel shapes flexibility and cost. GAP is typically financed as a lump sum at the point of sale, which means interest accrues on it over the loan term. Loan/lease payoff, added as a policy endorsement, can be dropped or adjusted at renewal without touching the loan balance.

Deductible treatment determines the net payout. Many GAP contracts absorb the borrower's deductible as part of the claim settlement, eliminating one more out-of-pocket expense at claim time. Loan/lease payoff applies the standard deductible first, so the 25% cap is effectively lower than it looks on paper.

What is Gap Insurance?

Gap insurance (Guaranteed Asset Protection) is a financial product that covers the shortfall between a vehicle's actual cash value (ACV) and the remaining loan or lease balance. ACV is what the insurer pays out after a total loss. This gap exists because vehicles depreciate rapidly while loan balances decrease much more slowly.

According to Kelley Blue Book, new cars lose approximately 20% of their value in the first year alone. Electric vehicles face a steeper curve—35–40% in year one.

Meanwhile, early loan payments go primarily toward interest, so the balance drops far more slowly than the car's value. That mismatch is exactly where the gap lives.

The core benefit: the driver is not left making payments on a vehicle they can no longer drive. Most gap contracts waive the full deficiency, and many also absorb the deductible, making it the more comprehensive option of the two products.

Key eligibility conditions:

- Typically must be purchased within 30 days of vehicle purchase

- Generally limited to new vehicles or vehicles without previous title history

- Requires active comprehensive and collision coverage

Important exclusions:

Gap insurance does not cover:

- Vehicle repairs or partial damage

- Past-due payments, late fees, or delinquencies

- Carry-over negative equity from a previous loan

- Fees added to the loan such as extended warranties or credit life insurance

These exclusions are commonly misunderstood and can cause claim disputes if not communicated clearly upfront.

Use Cases of Gap Insurance

Gap insurance provides the most value in these situations:

- Down payments under 20% create a larger potential gap from day one

- Loan terms of 60+ months slow principal reduction, keeping buyers underwater longer

- Leased vehicles often require gap coverage as a lender condition

- High-depreciation models—luxury sedans, certain EVs—widen the gap faster than average

- Rolled negative equity from a prior loan puts buyers underwater before they leave the lot

Numerical illustration:

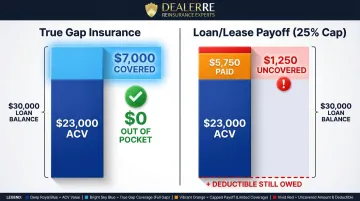

If a buyer owes $30,000 on their loan and the insurer determines the ACV is $23,000 after a total loss, the deficiency is $7,000. True gap insurance covers the entire $7,000 shortfall. By contrast, a loan/lease payoff endorsement capped at 25% of ACV would pay only $5,750 (25% of $23,000), leaving the buyer with a $1,250 out-of-pocket bill—plus their deductible if the contract doesn't include relief.

What is Loan/Lease Payoff Coverage?

Loan/lease payoff coverage is an optional endorsement added to an existing auto insurance policy that functions similarly to gap insurance but with a payout ceiling, commonly set at 25% of the vehicle's ACV. This terminology confusion creates real problems: major insurers often market this product as their "version of gap insurance," leading customers and even some F&I professionals to treat them as interchangeable. They are not.

Carrier structures vary significantly. According to Progressive's policy documentation, their Loan/Lease Payoff Coverage "pays the difference between the vehicle's value and the loan, limited to no more than 25% of the vehicle's value." Here's how three major insurers compare:

- Progressive: Covers the deficiency up to 25% of ACV

- USAA: Pays a flat 20% above ACV regardless of loan balance

- GEICO: Does not offer gap coverage in any form

For drivers whose loan-to-value gap is modest and falls within 25% of ACV, this endorsement is a lower-cost option that's easy to manage through your existing policy — simpler to add, adjust, or cancel than a standalone product. It can also serve buyers of used vehicles who don't qualify for traditional gap insurance.

When depreciation is steep, the 25% cap creates real out-of-pocket exposure. Consider a borrower with an ACV of $24,000 who owes $32,000 — the total deficiency is $8,000. A Loan/Lease Payoff endorsement capped at 25% of ACV pays a maximum of $6,000, leaving the borrower $2,000 short — plus any uncovered deductible.

That gap between what the endorsement pays and what the borrower owes is the central question when deciding whether this coverage is the right fit.

Use Cases of Loan/Lease Payoff Coverage

Loan/lease payoff coverage is the better or only practical option when:

- The buyer's insurer does not offer standalone gap insurance (like GEICO)

- The vehicle is used and more than three years old, disqualifying it from traditional gap insurance

- The buyer's estimated shortfall is small enough to fall comfortably within the 25% cap

- The buyer prefers managing all coverage through one insurer rather than a dealer-financed add-on

Gap Insurance vs. Loan/Lease Payoff: Which Is Better?

The right choice depends on the size of the likely coverage gap over the loan or lease term. Several factors increase gap risk and make the deficiency more likely to exceed 25% of ACV:

High-risk factors:

- Low or no down payment

- Loan terms of 72-84 months

- High-depreciation vehicles (EVs, luxury sedans)

- Rolled-over negative equity from a previous vehicle

- Leased vehicles with minimal capitalized cost reduction

With nearly 30% of new vehicles financed with 73- to 84-month loan terms, and average negative equity on trade-ins hitting a record $7,214 in Q4 2025, buyers are carrying deeper deficiencies for longer periods. When any of the above conditions are present, true gap insurance is the safer option.

Situational recommendations:

- Choose gap insurance when: The potential deficiency is large and uncertain; the buyer has minimal down payment, a long loan term, or a high-depreciation vehicle; the lender or leasing company requires gap coverage

- Choose loan/lease payoff when: The shortfall is modest, temporary, and calculable within the 25% cap; the buyer has substantial equity and a shorter loan term; the buyer prefers one-stop insurance management

- Always verify: Whether the lender or leasing company has a coverage requirement before deciding

The Naming Gotcha

Carriers use the terms interchangeably in marketing. To determine which protection a buyer actually has, they need to look for the presence or absence of a percentage cap in the actual contract or endorsement language — not the product name. A product labeled "Gap Coverage" might actually be a 25%-capped endorsement, while another labeled "Loan/Lease Payoff" might cover the full deficiency.

Real-World Scenario: 72-Month Loan, 18-Month Total Loss

A buyer finances a mid-range sedan with a 72-month loan, puts down 5%, and totals the vehicle at 18 months. Because early payments go primarily toward interest, the loan balance has decreased minimally. Meanwhile, the vehicle has depreciated 20%+ in its first year.

Scenario details:

- Original purchase price: $35,000

- Down payment: $1,750 (5%)

- Loan amount: $33,250

- Loan balance at 18 months: $29,500

- ACV at 18 months (after 25% depreciation): $26,250

- Deficiency: $3,250

True gap insurance: Pays the entire $3,250 shortfall (plus deductible if included). Out-of-pocket cost: $0.

Loan/lease payoff (25% cap): Pays up to 25% of ACV = $6,562.50. Since the deficiency is $3,250, the endorsement covers it fully in this scenario. Out-of-pocket cost: deductible only (typically $500-$1,000).

But if the buyer had rolled $5,000 negative equity into the loan:

- Loan balance at 18 months: $34,000

- ACV: $26,250

- Deficiency: $7,750

True gap insurance: Pays the entire $7,750 shortfall. Out-of-pocket cost: $0.

Loan/lease payoff (25% cap): Pays up to $6,562.50. Out-of-pocket cost: $1,187.50 plus deductible.

When to Cancel

Both coverages become unnecessary once the loan/lease balance drops below the vehicle's ACV — at that point, the driver is no longer "upside down." This typically happens between years two and three. Canceling at that point recovers premium dollars without leaving any coverage gap behind — which makes tracking equity position an ongoing part of managing the loan, not a one-time decision at signing.

What Auto Dealers Should Know When Offering These Products

For franchise, independent, and BHPH dealers, the choice between offering gap insurance and loan/lease payoff coverage through their F&I menu has a direct impact on both customer satisfaction and dealership profitability.

True gap products offered through the dealer, particularly through a dealer-owned reinsurance structure, allow the dealership to retain the underwriting profit rather than passing it to a third-party insurer. When dealers buy gap coverage from third-party providers at retail pricing, they capture only the markup between wholesale cost and retail price.

The third-party provider keeps all underwriting profit generated from premium reserves not used to pay claims. That profit stays with them regardless of how few claims occur.

How dealer-owned reinsurance captures that profit:

Through an administrator obligor reinsurance structure like DealerRE's program, dealers establish their own reinsurance company to directly underwrite gap coverage. The dealer collects the full retail premium and retains both the gross profit margin and the underwriting profit.

This structure is especially powerful for BHPH dealerships. Many BHPH dealers were already forgiving remaining balances after total loss accidents, providing gap coverage for free. Reinsurance converts that informal practice into a documented, profitable product line while improving customer satisfaction.

For example, if a BHPH dealer sells 150 gap policies annually at $499 each, that represents $75,000 added to receivables for a service many were previously providing for free. When claims occur, dealers file with their own reinsurance company and process payments directly, eliminating the adversarial relationship that often exists with third-party providers who have financial incentives to deny or delay claims.

That profit advantage only holds if your F&I team can sell it correctly.

Train your F&I staff on product differences:

Dealers and F&I managers who can clearly explain the difference between these two products — particularly the payout cap and its real-world implications — are better equipped to match the right coverage to each customer's financing situation. This reduces post-claim complaints and builds long-term customer retention.

Training should cover how to identify high-risk scenarios and communicate why the 25% cap matters:

- Low down payment deals where the customer starts underwater immediately

- Long loan terms (72–84 months) where equity builds slowly

- Rolled equity from a previous trade that inflates the new loan balance

Stay current on disclosure requirements:

When gap products are financed into a loan, state and federal regulations require specific disclosures. California's AB 2311, effective 2023, prohibits selling a gap waiver if the price exceeds 4% of the amount financed. It also mandates pro-rata refunds upon early termination. At the federal level, the CFPB requires that if gap insurance is mandatory to qualify for financing, the cost must be included in the finance charge and reflected in the disclosed APR.

Dealers should keep documentation current and ensure F&I staff understand cancellation and refund policies — these are among the most common sources of customer disputes.

Conclusion

For buyers with large loans, minimal equity, or high-depreciation vehicles, true gap insurance provides the most complete protection. For buyers with modest, well-defined shortfalls, loan/lease payoff coverage is a practical and accessible option—the key is understanding the cap before relying on it.

That distinction matters just as much on the dealer side. For auto dealers, knowing which product fits which buyer is how you protect customers from real financial exposure and build a more trusted F&I operation. Dealers who want to capture the underwriting profits from those products—rather than passing them to third-party providers—should look into owning their own reinsurance program. DealerRE helps dealerships set up and manage exactly that.

Frequently Asked Questions

Is loan/lease payoff coverage the same as gap insurance?

While both cover the shortfall between ACV and the loan balance after a total loss, they are not identical. Loan/lease payoff is typically capped at 25% of ACV, while true gap insurance is designed to cover the entire deficiency. Always read the actual contract terms before assuming equivalency.

Is loan/lease payoff coverage worth it?

It can be worth it when the potential shortfall is modest and falls within the 25% cap. Buyers with large loans, long terms, or low down payments are more likely to exceed that cap — making standalone gap insurance the safer choice.

Which is better: loan/lease payoff coverage or gap insurance?

For buyers at higher risk of going significantly upside down, gap insurance offers stronger protection. Loan/lease payoff works for buyers whose shortfall is small and predictable — but the cap is a real liability when depreciation outpaces equity.

Should you buy gap insurance on a lease?

Many lease agreements include gap coverage by default, but verify this before signing. If the lease excludes it — or the carrier only offers a capped loan/lease payoff endorsement — adding standalone gap coverage is advisable. Leases carry depreciation exposure from day one.

What does gap insurance cover and what does it not cover?

Gap insurance covers the deficiency between the loan/lease payoff and the vehicle's ACV after a total loss or theft. It does not cover repairs, missed payments, or amounts financed into the loan — such as extended warranties or negative equity rolled over from a prior vehicle.

How much does gap insurance usually cost?

Costs vary by provider and purchase channel. Insurer-based loan/lease payoff endorsements typically cost $20–$150 per year added to an existing premium. Dealer-sold gap products are often priced as a flat fee of $400–$1,000+ financed into the loan, which accrues interest over the loan term.