Introduction

Every BHPH dealer knows this moment: a customer's car breaks down. They can't afford the repair. Payments stop. You're forced to choose between absorbing the repair cost yourself or repossessing a broken vehicle—then fixing it anyway. Either path drains cash flow and threatens your lending pool.

This isn't just an operational headache. It's a cash flow problem with no clean exit. When repairs come out of your pocket to keep customers on the road, you're subsidizing their ownership with no reserve to draw from and no way to recoup those costs. Squeezed margins, depleted capital, and a business model built on absorbing losses.

Dealer-owned VSC reinsurance is the structural fix that turns this liability into a funded system and a new profit center. Instead of paying third-party warranty companies to capture your underwriting profits, you establish your own reinsurance company.

Your customers fund repairs through their monthly payments. You control the program. You keep 100% of the underwriting profit that warranty providers currently pocket.

What follows is a direct breakdown of how it works, what it costs to set up, and what BHPH dealers are actually earning once they stop writing checks to third-party providers.

TLDR: Key Takeaways

- BHPH dealers face unique threats: mechanical breakdowns lead directly to missed payments and repossessions

- Dealer-owned VSC reinsurance lets you fund repairs through customer payments—without draining your lending pool

- You capture 100% of underwriting profits that third-party warranty companies currently keep

- VSCs, Collateral Protection Insurance, and Debt Cancellation Coverage all flow through your reinsurance company—one structure, multiple revenue streams

- IRC 831(b) taxes small insurance companies only on investment income—keeping more profit inside your company instead of sending it to the IRS

Why BHPH Dealers Lose Money Every Time a Car Breaks Down

BHPH revenue depends entirely on consistent customer payments. Unlike traditional dealers who profit primarily from vehicle sales, BHPH operators function as lenders — and when a vehicle fails, that payment stream stops immediately.

The Three Root Causes of BHPH Customer Payment Failure

Customer payment failures in BHPH stem from three primary causes:

- Mechanical breakdown – When vehicles fail, customers stop paying. Industry data shows that bad debt expense reached 28% of sales in 2024, up from 21% in 2022, with mechanical issues contributing significantly to this trend

- Lapsed collateral insurance – Nearly 15% of consumers allow auto insurance coverage to lapse within a six-month period, exposing dealer collateral

- Life events – Job loss, medical emergencies, and other personal crises disrupt payment consistency

The Compounding Cost of the "Punish the Customer" Approach

When dealers repo a broken-down vehicle, the costs compound quickly:

- Repair costs remain – The vehicle still needs fixing before resale

- Lost customer relationship – The customer is gone, eliminating all future payment revenue

- Lost future payments – With an average default rate of 37.49% and average gross losses of $8,510 per repossession (2019 data), the financial impact is severe

- Repo administration costs – Processing, storage, and resale expenses compound the loss

Dealers respond to these losses in predictable ways — and most of those responses create new problems.

Why Current Workarounds Fail

BHPH dealers typically try three approaches to manage mechanical breakdowns—all problematic:

1. Paying for repairs out of pocket – Drains operating cash flow and creates inconsistent customer expectations

2. 50/50 splits with customers – Customers often can't afford their half, leading to the same payment failure

3. Buying third-party warranties upfront – The most damaging option for cash flow. Sell 10 contracts at $1,000 each, and third-party providers demand the full $10,000 the following month — pulled directly from the lending pool you need to fund new deals.

DealerRE's structure solves this by allowing dealers to finance VSC premiums over the contract term, collecting payments monthly as customers pay. This preserves cash flow, protects the lending pool, and puts underwriting profits back in the dealer's pocket at contract end.

What Is Vehicle Service Contract Reinsurance for BHPH Dealers?

Dealer-owned reinsurance is a separate legal entity (typically a C-corporation under IRC 831(b)) that you own and control. It accepts premiums from vehicle service contracts and other F&I products, holds those premiums in a protected trust account, pays claims from the trust, and retains unused reserves as profit.

Why Reinsurance Beats "Setting Money Aside"

Informal reserves create four critical problems:

- Tax inefficiency – Informal reserves are taxed as gross profit immediately

- No legal structure – Without defined coverage parameters, you create unlimited implied warranty exposure under law

- Liability risk – Informal promises lack the legal protection of insured contracts

- Administrative challenges – Out-of-town breakdowns require professional claims networks to manage

Reinsurance addresses each problem directly—through formal legal structure, contractual liability limits, and a professional claims administration network that operates wherever your customers drive.

The Admin Obligor Structure: Your Company, Backed by an A-Rated Carrier

In DealerRE's admin obligor model, your reinsurance company is the obligor on the VSC, backed and reinsured by an A-rated insurance carrier. This means:

- Customers have the protection of a major insurer behind their contract

- You control the program design, coverage terms, and claim handling

- You capture the underwriting profit

- If your reinsurance company's reserves are insufficient, the A-rated carrier covers claims—limiting your liability to formation costs plus accumulated earnings

A DOWC without admitted insurer backing carries a critical gap: unlimited claim liability. The admin obligor structure eliminates that exposure by placing an A-rated carrier as the backstop.

Two Types of Reinsurance Contracts: Quota Share vs. Excess of Loss

Quota Share Reinsurance:

You cede a fixed percentage of premiums and losses to the reinsurer. Risk and profit are shared proportionally at a defined ratio. This structure is ideal for homogeneous portfolios like motor insurance, where risks are fairly similar—perfect for BHPH VSC programs.

Excess of Loss Reinsurance:

You retain losses up to a defined threshold (your "retention" or "deductible"). The reinsurer covers catastrophic losses above that amount. Premiums and losses are not shared proportionally—this structure protects against large, unexpected claims.

Most BHPH VSC programs use quota share admin obligor structures backed by A-rated insurers. The proportional design keeps risk manageable while giving dealers a predictable share of underwriting profit on every contract sold.

A 30-Year Track Record: This Isn't New

Dealer-owned reinsurance isn't experimental. Producer-owned reinsurance companies began forming in the 1960s and 1970s, and vehicle service contract reinsurance became a mainstay in the 1980s. For decades, the structure was largely the domain of franchise and large-volume dealers. DealerRE has spent 30 years bringing that same framework to independent and BHPH operators—with the compliance infrastructure, A-rated carrier backing, and hands-on administration to make it work at any scale.

How BHPH VSC Reinsurance Works: The Mechanics

Premium Finance: Protecting Your Cash Flow and Lending Pool

Traditional third-party warranty companies require full premium payment upfront. Sell 10 contracts at $1,000 each? You owe $10,000 next month—depleting your lending pool.

DealerRE finances the premium over the contract term instead. A prorated portion of the VSC premium is collected from the customer's regular payment and forwarded to your reinsurance trust account each period.

Example: A $1,000 VSC on a 24-month contract collects approximately $42/month from the customer. You're billed monthly as customers pay, preserving cash flow and protecting your lending pool.

How the Trust Account Works

Premiums are held in a legally protected, non-commingled trust account in the U.S., managed by a third-party trustee. Key protections include:

- Cannot be used as a general bank account – Funds are reserved solely for claims per the trust agreement

- NAIC Model Act requires 40% funded reserve – Providers must maintain reserves of at least 40% of gross consideration received, less claims paid

- 5% financial security deposit – Minimum $25,000 in surety bond, securities, cash, or letter of credit

- Conservative investment guidelines – Reserves initially invested in government bonds to preserve capital

This structure is far more secure than informal reserves or relying on a third-party warranty company's solvency.

The Claims Process: Professional Adjudication, No Operational Burden

When a customer breaks down—even out of town—they contact a professional claims team via an 800-number. That team adjudicates the claim, arranges repair authorization with the shop, and deducts payment from the trust—not from your operating account.

You customize coverage parameters to fit your inventory and risk tolerance, while the claims team handles the rest operationally. Once claims are settled, whatever remains in the trust at contract expiration belongs to you.

What Happens to Unused Reserves: Your Underwriting Profit

At contract expiration, any premium not used to pay claims becomes your underwriting profit, distributed from the trust.

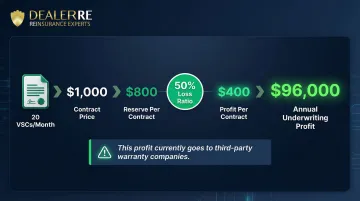

Here's how that looks in practice:

| Variable | Figure |

|---|---|

| VSCs sold per month | 20 |

| Contract price | $1,000 |

| Reserve per contract | $800 |

| Loss ratio (industry-typical) | 50% |

| Profit per contract | $400 |

| Annual underwriting profit | $96,000 |

That $96,000 is profit third-party warranty companies currently keep for themselves.

The DealerRE Admin Obligor Model: Full-Service Administration

DealerRE handles:

- Legal formation and filings

- Tax returns and IRS 831(b) compliance

- Claims adjudication through professional teams

- Trust account management and financial reporting

- Licensing renewals and regulatory compliance

- Monthly performance reports analyzing your program

You get the full benefit of owning your reinsurance company without the administrative burden.

Beyond VSCs: Other Products You Can Reinsure in a BHPH Program

Collateral Protection Insurance (CPI)

When customers let their insurance lapse—which happens with nearly 15% of consumers—your collateral is exposed. CPI is a single-interest insurance plan that protects the creditor if the debtor fails to maintain insurance.

Through reinsurance:

- The premium is customer-funded, collected monthly alongside their payment

- Your vehicle is protected from physical damage losses

- You eliminate administrative headaches with outside insurers

- You capture the underwriting profit

One important note: CPI covers only physical damage to the vehicle, not bodily injury or liability. Customers must still maintain state-required liability insurance independently.

Debt Cancellation Coverage (DCC) / Loss Damage Waiver (LDW)

Debt cancellation eliminates a loan if the borrower dies, or cancels monthly payments if the borrower becomes disabled, unemployed, or suffers a specified hardship. For BHPH customers who may not qualify for traditional insurance products, **DCC offers an affordable alternative to GAP insurance** that still protects your portfolio.

LDW is the lease-specific variant for LHPH (lease here pay here) operations. The CFPB has taken enforcement action against lenders for undisclosed LDW interest charges—highlighting the need for compliant, transparent programs like DealerRE's.

GAP Insurance

GAP covers the difference between the insurance payout and the remaining loan balance on a total loss. For BHPH dealers, it's one of the most practical products to reinsure because your customers genuinely need it and you're often absorbing the loss anyway.

When you reinsure GAP, you capture the underwriting profit on every contract sold. Claims go through your own reinsurance company, so there are no third-party delays, no denials from external providers, and no chasing payouts. Many BHPH dealers already forgive deficiency balances after total losses—effectively providing GAP at no charge. Reinsurance lets you formalize that protection, price it appropriately, and keep the proceeds.

The Financial Upside: Underwriting Profits, Tax Benefits, and Investment Income

Underwriting Profits: Capturing What Third Parties Currently Keep

Every dollar of premium reserve not used to pay claims becomes your profit. Unlike third-party arrangements where the provider retains all surplus, you capture 100%.

Underwriting margins vary by program design, customer profile, and claims experience—but the principle is consistent across well-run programs. If third-party warranty companies weren't profitable, they wouldn't be in business. That profit belongs to you.

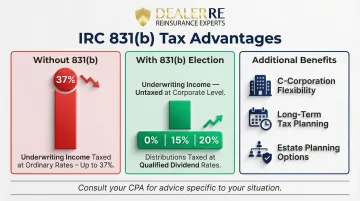

Tax Advantages Under IRC 831(b)

For taxable years beginning in 2026, IRC § 831(b) allows small insurance companies with net written premiums under $2,900,000 to elect taxation only on investment income, not underwriting income.

Key benefits:

- Underwriting profits are not taxed at the corporate level until distributed

- Distributions are taxed at the qualified dividend rate (0%, 15%, or 20% depending on income level)—not ordinary income rates (up to 37%)

- These are C-corporations, allowing long-term tax planning and estate planning flexibility

Important: This is general information, not tax advice. Consult your CPA to understand how IRC 831(b) applies to your specific situation.

Investment Income and Wealth-Building Flexibility

Trust reserves can be invested in stocks, bonds, or other securities once they exceed 125% of unearned premiums, adding a second income stream beyond underwriting profit.

Dealers put those earnings to work in a range of ways:

- Real estate acquisition

- Retirement planning

- College funding for children

- Reinvestment in dealership expansion

- Estate planning and wealth transfer

Frequently Asked Questions

How does reinsurance work for car dealerships?

A dealer-owned reinsurance company accepts premiums from VSCs and other F&I products sold to customers , holds them in a protected trust, and pays claims from that trust. Unused reserves stay with the dealer as profit, replacing the third-party provider that would otherwise keep that surplus.

What is a VSC payment?

A VSC (Vehicle Service Contract) payment is the amount a customer pays for a service contract covering mechanical repairs after purchase. In BHPH reinsurance, this payment is collected in prorated installments alongside the customer's regular car payment, eliminating the need for dealers to pay the full premium upfront.

What is VSC and GAP insurance?

A VSC covers the cost of mechanical repairs to a vehicle, while GAP (Guaranteed Asset Protection) covers the difference between the insurance payout and remaining loan balance if the vehicle is totaled. Both products can be reinsured through a dealer-owned company so the dealer captures the underwriting profit.

What are the two types of reinsurance contracts?

With quota share reinsurance, the dealer cedes a set percentage of premiums and losses proportionally. With excess of loss reinsurance, the dealer absorbs losses up to a threshold while the reinsurer covers anything above it. Most BHPH VSC programs use a quota share admin obligor structure backed by an A-rated insurer.

Do I need insurance for a buy here pay here?

State-required liability insurance must be carried by customers by law. Collateral Protection Insurance (CPI) is what BHPH dealers require contractually to protect the vehicle itself. Dealer reinsurance programs like CPI and DCC offer more affordable, dealer-controlled alternatives to traditional insurance for BHPH customers.

BHPH dealers face real cash flow risk every time a vehicle breaks down. Dealer-owned VSC reinsurance turns that risk into a funded system, protecting your lending pool, keeping customers on the road, and recapturing the underwriting profits that third-party providers currently keep. DealerRE has helped more than 400 auto dealers nationwide structure compliant, profitable reinsurance programs backed by A-rated carriers.

Ready to explore how reinsurance can transform your BHPH operation? Contact DealerRE at (804) 824-9533 for a free dealership analysis.