According to the Q2 2025 Haig Report, publicly traded auto retail groups reported an average F&I gross profit per vehicle of $2,515—making F&I one of the most reliable profit centres in today's market. Yet many dealers leave money on the table by treating VSCs as afterthoughts rather than strategic revenue drivers.

Whether you're new to selling VSCs or looking to refine your approach, this guide covers everything from legal definitions and compliance requirements to proven sales strategies, objection handling techniques, and what happens when customers later sell their vehicles. You'll learn how to present VSCs more effectively, meet FTC disclosure requirements, and potentially recapture profits that currently go to third-party warranty companies.

TLDR:

- VSCs are optional, separately purchased agreements—not warranties—that cover mechanical breakdowns for defined periods

- F&I PVR reached $2,515 in Q2 2025, with VSCs representing a top profit centre for dealers

- Dealer-owned reinsurance structures let you capture 100% of underwriting profits third-party providers currently keep

- Present VSCs in tiered formats early in the sales process to reduce resistance and improve acceptance

- Transferable VSCs can increase resale value and provide pro-rated refunds when vehicles are sold

What Is a Vehicle Service Contract—and How Does It Differ from a Warranty?

A vehicle service contract (VSC) is an optional, separately purchased agreement that commits a seller or third party to cover specific repairs or services on a vehicle for a defined period or mileage. Although commonly called an "extended warranty," federal law does not classify VSCs as warranties.

The Legal Distinction That Matters

Under the Magnuson-Moss Warranty Act and 16 CFR § 700.11, a manufacturer's warranty is included in the vehicle's purchase price with no additional cost. A VSC always costs extra and is sold as a separate product. Because of that distinction, the FTC explicitly prohibits representing VSCs as warranties—even when marketed as "extended warranties." This isn't just semantics; it directly affects your compliance obligations and how F&I staff must present the product.

What VSCs Cover vs. Exclude

Most VSCs cover mechanical breakdowns of major components but exclude normal wear and tear, accident damage, and certain maintenance items. Coverage typically includes:

What's typically covered:

- Engine components (engine block, cylinder heads, internally lubricated parts)

- Transmission systems (torque converter, internal linkage)

- Major electrical components

- Brake system components (master cylinder, calipers)

What's typically excluded:

- Routine maintenance (oil changes, filters, fluids)

- Normal wear items (brake pads, brake shoes, wiper blades)

- Manual clutch components (friction clutch disc, pressure plate)

- Cosmetic items (paint, trim, upholstery)

- Damage from accidents or neglect

For example, if a customer's transmission fails at 65,000 miles, a comprehensive VSC would typically cover the repair. But if their brake pads wear out from normal use, that's excluded unless specifically listed in the contract. Reviewing the coverage schedule line by line during the F&I conversation prevents disputes later—and builds the kind of trust that drives repeat business.

Why VSCs Are a Critical F&I Profit Driver for Dealers

VSCs often represent the highest per-unit profit product in F&I, making them essential to dealership margins—especially for independent and BHPH dealers who can't rely solely on vehicle gross profit.

The Traditional VSC Profit Model

When dealers sell third-party VSCs, the majority of the premium goes to the administrator or warranty company rather than back to the dealership. IBISWorld estimates the US auto extended warranty market at $32.7 billion for 2026, with third-party providers capturing substantial underwriting profits.

Here's how the traditional model works: you sell a VSC for $2,500, earn a $600 commission, and the warranty company keeps the remaining premium minus claims costs. If claims run 40% of premium, that warranty company retains approximately $1,340 in underwriting profit per contract. That's profit you helped generate but never see.

The Dealer-Owned Reinsurance Opportunity

Dealers who establish their own admin obligor reinsurance company can recapture 100% of the profits that third-party warranty companies would otherwise keep. Instead of sending premiums to external vendors, you retain them in your own reinsurance structure—turning VSC sales into a direct revenue stream. DealerRE helps dealers set up and manage exactly this kind of structure.

DealerRE's admin obligor model allows dealers to:

- Maintain the same gross profit earned with third-party providers

- Capture all underwriting profit (premiums minus claims) previously lost to warranty companies

- Control the claims experience and customer service post-sale

- Invest premium reserves to generate additional ROI beyond claims profits

Customer Retention Benefits

When dealers control the VSC and claims process, they also control the customer experience post-sale. Third-party administrators may have incentives to deny or delay payments—your own warranty company doesn't have that conflict.

Owning the claims process creates direct loyalty advantages:

- Smooth claims experiences drive repeat vehicle purchases

- Faster claim resolution builds trust that third-party admins rarely deliver

- Direct customer contact post-sale keeps your dealership top of mind

Compounding Financial Benefits

VSC premiums held in a reinsurance structure can be invested, generating additional returns beyond underwriting profits. Initially, reserve funds must be invested conservatively in government bonds through a Trust Company structure.

Once balance sheet cash exceeds 125% of unearned premiums, excess funds may be invested more aggressively at the direction of company ownership, providing dealers with additional income and long-term asset growth.

What Dealers Must Disclose When Selling a VSC

The FTC's Combating Auto Retail Scams (CARS) Rule, effective July 2024, strictly prohibits dealers from misrepresenting that optional add-ons like VSCs are required to purchase, lease, or finance a vehicle. Compliance isn't optional—violations can result in significant penalties.

Key FTC Requirements

Dealers must obtain express, informed consent for any charge and clearly disclose that optional add-ons are not required. You cannot:

- Imply a VSC is required to obtain financing

- Present it as a manufacturer's warranty

- Include it in contract paperwork without explicit customer acknowledgment

Essential Point-of-Sale Disclosures

At the point of sale, dealers should clearly communicate:

- Who backs the contract — manufacturer, your dealership, or a third-party administrator — so customers know who handles their claims

- Coverage details, including specific components covered and excluded, plus any deductibles per visit or repair

- Cost structure — total contract price, monthly payment if financed, and how it affects the overall purchase

- Claims process — how customers file claims, where they can get service, and expected turnaround times

- Cancellation and transfer policies, including whether the contract transfers to subsequent buyers and what refund applies on cancellation

The Administrator Insolvency Scenario

State laws vary on what happens if the administrator or dealer closes. In many states, one party assumes the other's obligations, but this varies by jurisdiction:

- California requires VSC providers to carry backup insurance from admitted insurers covering 100% of obligations, unless the obligor proves a net worth of $100 million

- Florida requires associations to maintain a deposit, surety bond, or contractual liability insurance to protect consumers

- Texas mandates reimbursement insurance policies, funded reserve accounts with security deposits, or $100 million net worth

Review your state's specific laws and disclose this information to customers so they understand their protection.

Present Terms in Writing

Verbal explanations are insufficient. Use a clear, itemized F&I menu that lets customers see coverage options, costs, and payment choices side by side. This transparency builds trust and ensures compliance with federal disclosure requirements.

How to Present and Sell VSCs More Effectively to Every Buyer

Dealers who see the highest VSC acceptance rates share one habit: they introduce coverage early and consistently, so the F&I conversation feels like a natural next step rather than a last-minute add-on.

Introduce VSCs Early in the Sales Process

Cox Automotive research shows that 63% of consumers are more likely to buy F&I products if introduced before finalizing the vehicle purchase. When salespeople mention service protection during the vehicle walk-around or test drive, the F&I manager's conversation becomes a continuation rather than a surprise, reducing resistance.

Train your sales team to plant seeds early: "This vehicle comes with the remainder of the factory warranty, and we also offer extended coverage options that can protect you after that expires. Our F&I manager will show you the available plans when we finalize paperwork."

Use a Tiered Offering Strategy

Present VSCs at multiple coverage levels so customers can choose rather than simply saying yes or no. A tiered structure might look like this for a used vehicle:

Basic Powertrain ($995):

- 12 months / 12,000 miles

- Covers engine, transmission, drivetrain

- $100 deductible per visit

Mid-Tier Major Components ($1,795):

- 24 months / 24,000 miles

- Covers powertrain plus electrical, A/C, steering, brakes

- $50 deductible per visit

Comprehensive Coverage ($2,695):

- 36 months / 36,000 miles

- Exclusionary coverage (everything except wear items and maintenance)

- $0 deductible

This approach gives budget-conscious customers an entry point while allowing others to select more comprehensive protection.

Show the Cost Comparison Side by Side

Present real-world repair costs versus the monthly VSC payment. Transmission replacements now average $5,892 to $6,402, according to RepairPal. An A/C compressor replacement runs $1,004 to $1,356.

Frame it this way: "This mid-tier coverage adds $75 per month to your payment. A single transmission repair would cost you $6,000 out of pocket—that's 80 months of VSC payments. If your transmission fails in year two, you've saved $4,500."

When buyers see the numbers side by side, the monthly cost stops feeling like an add-on and starts feeling like a hedge against a much larger expense — which is exactly where the emotional conversation picks up.

Emphasize Peace of Mind Over Features

Buyers who aren't mechanically inclined or who have tight monthly budgets often respond better to emotional value than component lists. Tailor your pitch to different profiles:

For the budget-conscious buyer: "I know every dollar counts for you. This plan ensures you'll never face a surprise $5,000 repair bill you can't afford. You'll know exactly what your transportation costs are every month."

For the risk-averse professional: "You depend on this vehicle to get to work every day. This coverage gives you peace of mind that if something goes wrong, you're protected—no stressful decisions about whether you can afford the repair."

For the first-time buyer: "This is a big purchase, and we want you to feel confident. This protection means you can enjoy your vehicle without worrying about what might break."

Structure Post-Delivery Follow-Up

Customers who decline VSCs at delivery aren't lost causes. Implement a follow-up schedule:

- At 90 days: Check in on the vehicle, then mention how much factory warranty time remains. "We can still add extended coverage if you'd like that protection before it expires."

- At 6 months: Flag the approaching warranty expiration directly. "Would you like to schedule a time to review coverage options before you lose that protection?"

- Service department visit: Invite declined customers to tour the repair bay. Seeing the shop floor and hearing techs discuss common repairs makes the cost of going unprotected concrete — a low-pressure approach that often reopens the conversation.

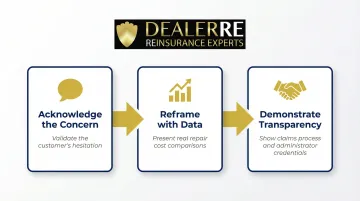

Handling Common Customer Objections to VSCs

Even with perfect presentation, objections happen. Here's how to address the most common concerns with confidence and data.

"It's too expensive" / "I'll just pay out of pocket if something breaks"

Respond with concrete cost comparisons. A single transmission repair can easily exceed the total cost of a multi-year VSC. CarMD reports that catalytic converter replacements average $1,348, and that's a moderately priced repair.

"I understand $2,200 seems like a lot right now. But let's look at what repairs actually cost: a transmission replacement runs $6,000, an A/C compressor is $1,200, and a catalytic converter is $1,350. If you face just one of these repairs, you're already ahead. Can you comfortably afford a $6,000 surprise expense six months from now?"

Most customers can't, and this reframing makes the VSC premium feel reasonable.

"The new car already has a warranty—I don't need this"

Clarify that manufacturer warranties are limited in duration and scope. Position the VSC as picking up where factory coverage leaves off.

"You're right that you have a three-year, 36,000-mile factory warranty. But what happens in year four when that expires and you still have two years of payments left? This VSC is structured to begin coverage after your factory warranty expires, so you're not paying for overlapping protection—you're extending your coverage for the life of your ownership."

"I've heard these contracts never pay out"

The reputation of your VSC administrator matters here, and transparency is what overcomes skepticism.

"That's a fair concern, and unfortunately some companies have earned that reputation. That's why we only work with [administrator name], which is backed by an A-rated insurance carrier. They processed over 437,000 claims last year alone. Let me show you exactly how the claims process works, what's covered, and what recourse you have if a claim is denied. We want you to understand exactly what you're getting."

If you've transitioned to a dealer-owned reinsurance structure, emphasize that you control the claims process: "We administer these contracts ourselves, which means when you file a claim, you're working with us—not some distant third party looking for reasons to deny coverage. Our reputation depends on taking care of you."

That kind of openness converts skeptics into buyers.

What Happens to a VSC When the Car Is Sold?

When a customer sells their vehicle before a VSC expires, two outcomes are possible: the contract transfers to the new buyer, or the original owner cancels it for a refund. Knowing how each scenario works lets you present VSCs accurately at the point of sale—and handle post-sale requests without friction.

VSC Transferability as a Selling Point

Many VSCs can be transferred to a subsequent buyer if the original owner sells the vehicle before the contract expires. This transferability increases resale value and marketability, especially for used vehicles, where repair cost uncertainty is a top buyer concern.

Frame it this way during the initial sale: "If you decide to sell this vehicle before the coverage expires, you can transfer this contract to the new buyer. That makes your vehicle more attractive and can support a higher asking price. It's protection for you now and added value when you sell."

The Transfer Process and Typical Fees

Most contracts require a transfer application and a fee. Florida statute caps assignment fees at $40, and sample contracts from major administrators show transfer fees of $50. Transfers usually require:

- Copies of maintenance records proving proper vehicle care

- Bill of sale showing ownership transfer

- Transfer application submitted within 30 days of vehicle sale

- Transfer fee payment

Contracts typically cannot be transferred to another dealership or commercial entity—only to private purchasers.

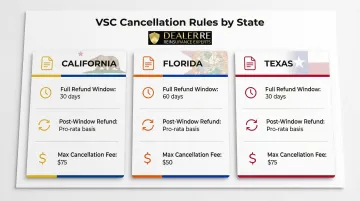

Cancellation Rules for Customers Who Sell

If the new buyer doesn't want the VSC or the contract is non-transferable, the original buyer may be entitled to a pro-rated refund. State laws dictate the specifics:

| State | Full Refund Window | After Window | Max Fee |

|---|---|---|---|

| California | 30–60 days (no claims filed) | Pro-rata by time/mileage | 10% or $25, whichever is less |

| Florida | 60 days (less claims + 5% fee) | 90% unearned pro-rata refund | 5% of contract price |

| Texas | 30 days | Pro-rata refund | $50 cancellation fee |

Walk customers through cancellation terms at signing. When they understand the refund process upfront, post-sale requests are handled faster—and your F&I office spends less time managing disputes.

Frequently Asked Questions

How much should an auto service contract cost?

VSC pricing depends on the vehicle's make, model, age, mileage, coverage level, and contract length. ConsumerAffairs data based on 500+ quotes shows typical costs range from $2,000 to $5,000 total, with most plans averaging around $3,000. Deductibles may apply per visit or per repair, affecting the overall value.

What is the difference between a vehicle service contract and a warranty?

A warranty is included in the purchase price of a new vehicle and requires no separate payment, while a VSC is always sold as an optional add-on at additional cost. Federal law does not classify VSCs as warranties even when marketed as "extended warranties."

Can a vehicle service contract be transferred when the car is sold?

Many VSCs are transferable to a new owner before the contract expires, usually for a fee of $40 to $50. This can make the vehicle more attractive to buyers and potentially support a higher asking price. Terms vary by provider, so review the contract for specific transferability clauses.

Does having a vehicle service contract increase a car's resale value?

A transferable VSC gives buyers confidence by reducing their exposure to repair costs — a major concern with used vehicles. That peace of mind can accelerate the sale, particularly when buyers are weighing the risk of purchasing a vehicle without any remaining factory coverage.

What happens to a VSC if the dealership that sold it goes out of business?

If the dealer closes, the administrator backing the contract is typically still responsible for fulfilling coverage, and vice versa. State laws vary, but most require financial protections like backup insurance policies, surety bonds, or contractual liability insurance. Customers should confirm who the administrator is and what protections apply under their state's laws.

Are vehicle service contracts worth it for used cars?

VSCs offer real value on used vehicles, which carry higher repair risk than new cars — especially once the factory warranty has expired. The contract cost often compares favorably to a single major mechanical repair on a higher-mileage vehicle.

Want to keep the profits your VSC program is already generating? DealerRE helps dealers selling 30+ vehicles monthly establish admin obligor reinsurance companies that capture 100% of underwriting profits. With 28 years of proven success and full-service administration including training, compliance, and claims management, DealerRE enables you to take back the profits third-party warranty companies currently keep. Contact the team at (804) 824-9533 to schedule your free dealership analysis.