Introduction

Auto dealers know the math has changed. Front-end gross profit collapsed to just $279 per unit by late 2025—a 52.4% year-over-year decline that forced dealerships to confront a harsh reality: F&I is no longer a secondary profit center; it's the primary engine keeping dealerships solvent. By December 2025, nearly 90% of gross profit per deal came from F&I departments, with F&I per vehicle retailed (PVR) reaching record highs above $2,000.

Yet despite this shift, many dealers—especially independent, Buy Here Pay Here (BHPH), and smaller franchise operators—are forfeiting millions in underwriting profits and investment income by avoiding F&I profit participation programs.

These programs, specifically admin obligor reinsurance structures, allow dealers to share in the underwriting income and investment returns from the vehicle service contracts, GAP insurance, and ancillary products they already sell. Without them, all that profit flows to third-party providers instead.

That surrender persists largely because of bad information. Widespread misconceptions cause dealers to dismiss these programs as too complicated, too risky, reserved for large operators, or tax nightmares. This article addresses the five most damaging myths keeping dealers from capturing the profits they've already earned.

TLDR

- Profit participation programs work for dealers of all sizes—structured programs scale down to dealers selling as few as 25–30 service contracts monthly

- Modern admin obligor reinsurance programs are straightforward when the right partner manages setup, compliance, and administration

- Dealers who own their reinsurance structure control claims experience and capture 100% of underwriting profits third-party providers currently keep

- Properly structured dealer-owned reinsurance companies deliver tax efficiency, not added tax burden

- Staying out of a profit participation program is the real financial risk—every month without one, dealers are funding a third-party provider's margins instead of their own

Misconception #1: Profit Participation Programs Are Only for Large Dealerships

Many dealers assume profit participation and reinsurance programs require high-volume franchise operations to generate meaningful returns, leaving small to mid-size independent dealers, BHPH operators, and smaller franchise stores convinced the opportunity doesn't apply to them.

Program structures today are scalable and tailored to a dealer's specific volume. Industry guidance shows that a Producer Owned Reinsurance Company (PORC) becomes financially viable at just 25 to 30 vehicle service contracts monthly — or 300 to 350 contracts annually. For Dealer Owned Warranty Company (DOWC) structures, break-even typically occurs around 100 to 150+ contracts per month.

How Admin Obligor Reinsurance Scales

Admin obligor reinsurance works regardless of size because the dealer establishes their own reinsurance company that receives ceded premiums from every F&I product sold—whether that's 10 units a month or 100. The accumulation of premiums over time, combined with investment income on reserves, creates compounding long-term wealth even at modest volume levels.

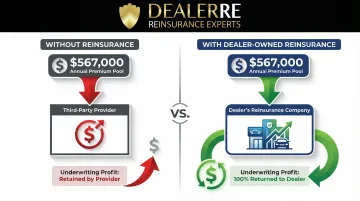

Run the numbers on a mid-size independent: a dealer selling 50 vehicles monthly with a 45% VSC attachment rate moves 22 service contracts per month. At an average selling price of $1,500 per contract, that's $396,000 in annual VSC premiums alone. Add 39% GAP penetration at $750 per policy, and the dealer generates another $171,000. Total annual premium pool: $567,000.

Without a reinsurance structure, the underwriting profit and investment income on that $567,000 flows entirely to third-party administrators. With a dealer-owned reinsurance company, 100% of underwriting profits return to the dealer.

BHPH and Independent Dealers Are Well-Positioned

BHPH dealers and independent used car dealers are often assumed to be excluded from reinsurance programs, but they're actually ideal candidates. The average BHPH dealer sold 1,080 units annually (90 per month) in 2020, easily clearing the 25-contract threshold. Independent dealers collectively sold 9.8 million vehicles in 2025, representing massive premium volume currently ceded to third parties.

BHPH customers are also reliable F&I buyers. Their purchase patterns generate consistent premium streams that translate directly into reinsurance returns:

- Purchase service contracts at high attachment rates relative to vehicle value

- Regularly add ancillary products like tire & wheel and debt cancellation coverage

- Provide predictable monthly volume that compounds over time inside a reinsurance structure

That consistent volume is exactly why DealerRE has helped more than 400 dealers — from single-lot independents to multi-rooftop franchise groups — establish and manage their own admin obligor reinsurance companies. Volume helps, but it's not the barrier most dealers assume it is.

Misconception #2: These Programs Are Too Complicated to Set Up and Manage

The legal and administrative language around reinsurance—terms like "ceded premiums," "obligor," "trust accounts," and "tax filings"—makes the process sound intimidating, causing dealers to assume the operational burden outweighs potential returns.

The Reality: Complexity is largely managed by the right program partner, not the dealer. A full-service provider handles company formation, legal filings, state compliance, tax returns, renewals, claims adjudication, and performance reporting—leaving dealers focused on selling F&I products and capturing profit.

What Dealers Actually Do Day-to-Day

Once your reinsurance company is established, your primary responsibility is simply selling F&I products through your normal dealership sales process. You continue offering vehicle service contracts, GAP, collateral protection, and ancillary products to customers. Premiums from those products flow into your reinsurance company, where they're held and invested according to regulatory guidelines.

Your day-to-day involvement ends there. The administrator manages:

- Monthly financial statements detailing all reinsurance operations

- Claims adjudication and payment authorization

- Billing services and premium collection

- Annual reports for tax preparers and registered agents

- License renewals and regulatory compliance

- Monitoring claims losses and projecting operations through contract earn-out periods

You receive periodic performance reviews with your reinsurance partner to discuss financial direction and results, but administrative burdens are handled entirely by your administrator.

That said, who you delegate to matters just as much as the delegation itself.

The Importance of Partner Quality

Choosing a partner who provides F&I training, onboarding, and ongoing support—not just a program structure—determines how smoothly the program runs and how profitable it becomes over time.

Quality training ensures your staff understands product benefits, selling processes, and compliance requirements, enabling higher penetration rates and better customer experiences. When staff knows how to sell reinsured products effectively, dealers capture more underwriting profits. When they understand compliance protocols, audit risk drops.

The difference between a good reinsurance program and a great one usually comes down to the partner behind it—their experience, their training depth, and how invested they are in your dealership's success.

Misconception #3: Participating in a Program Means Giving Up Control of Your F&I Business

Dealers often fear that entering a profit participation or reinsurance arrangement means surrendering authority over products, pricing, customer experience, or claims decisions to an outside entity—reducing their autonomy.

The Reality: Admin obligor reinsurance actually increases dealer control. In this structure, the dealer's own reinsurance company receives premiums and participates in claims outcomes, giving dealers direct influence over their claims experience—unlike passive third-party arrangements where the insurer controls every claims decision.

Claims Control Creates Customer Loyalty

When dealers control claims through their own reinsurance company, they ensure faster and fairer resolution for customers, which improves CSI scores, drives repeat business, and strengthens the service relationship. According to the J.D. Power 2026 U.S. Customer Service Index Study, when overall service satisfaction reaches 950 or higher, 86% of mass-market customers say they "definitely will" return to the dealer for paid service.

The repurchase effect is significant. Cox Automotive found that car owners serviced at the dealership are 74% more likely to buy their next car from that same location. That loyalty is at risk: dealerships have lost 12% of service visits to independent competitors since 2018, often because of poor claims experiences that push customers away.

Here's the difference:

| Claims Handling Model | Adjudication Incentive | Customer Experience Impact |

|---|---|---|

| Third-Party Administrator | Deny claims to preserve underwriting profit | High friction; customer feels abandoned |

| Dealer-Owned Reinsurance | Approve valid claims to drive service lane traffic and CSI | Seamless experience; dealer controls outcome |

Because the dealer owns the reserve, they can authorize borderline claims to ensure customer satisfaction, driving fixed operations revenue and future vehicle sales rather than optimizing for claim denial.

You're Not "On the Hook" for All Losses

That claims control naturally raises a follow-up question: what happens when losses run high? In an admin obligor reinsurance model, the dealer's reinsurance company is backed by A-rated insurers. Catastrophic risk is covered, while the dealer still participates in profitable underwriting experience—a financial safety net that doesn't require giving up the upside.

If the reinsurance company cannot meet its obligations, the ultimate liability rests with the direct writing insurance company—not your personal assets. In practice, your exposure is limited to formation costs plus accumulated earnings. The structure is designed so dealers capture profit without bearing unbounded risk.

Misconception #4: Third-Party F&I Providers Are Just as Profitable as Owning Your Own Program

Many dealers assume the revenue they earn from selling third-party F&I products—through reserve, backend profit, or commission—represents the full economic opportunity available to them. In reality, it represents only a fraction of total profit generated by those products.

Third-party warranty and insurance companies collect premiums, invest them, pay claims, and retain underwriting profit. That retained profit often exceeds what the dealer received in markup or reserve. The dealer provided the customer and made the sale; the provider captured the long-term financial outcome.

Where the Money Actually Goes

Underwriting profit is calculated as: Premiums - Claims - Expenses = Underwriting Profit

Authoritative filings show VSC loss ratios typically range from 40% to 65%. If an insurer maintains a 25% expense ratio and a 65% loss ratio, that yields a 10% underwriting margin. Any reserve not used to pay claims becomes pure profit for the provider.

Because VSC and GAP claims are paid out over 3 to 7 years, premiums sit in reserve generating investment income. In a standard commission model, the third-party insurer keeps 100% of that investment income.

Quantifying the Opportunity Cost

Two scenarios illustrate how much dealers leave on the table:

Scenario A — Retail Dealer ($500K annual premiums)

- 50% loss ratio: $250,000 pays claims

- 25% expense ratio: $125,000 covers admin costs

- Remaining $125,000/year in underwriting profit goes to the third party

- Over five years: $625,000 forfeited, excluding investment income

Scenario B — BHPH Dealer (20 VSCs/month, $800/contract in reserve)

- 50% loss ratio yields $400 in underwriting profit per contract

- That's $96,000 in additional net profit annually flowing to the provider instead of the dealer

Dealer-Owned Reinsurance Captures 100% of Profits

Once premiums are ceded to the dealer's own reinsurance company, all underwriting gains and investment returns flow back to the dealer, not to a third party. Accumulated funds can be used for real estate investment, reinvestment into the dealership, college funding, or other wealth-building purposes.

Revenue comparison:

| Revenue Component | Standard Commission Model | Dealer-Owned Reinsurance |

|---|---|---|

| Upfront Markup | Yes | Yes |

| Underwriting Profit | No (Retained by provider) | Yes (Dealer retains 100%) |

| Investment Income | No (Retained by provider) | Yes (Dealer earns interest) |

| Tax Efficiency | Taxed immediately as ordinary income | Yes (Potential capital gains treatment) |

The dealer maintains gross profit on the initial sale and captures all underwriting profits as policies expire. Every dollar that previously built wealth for a third-party provider now builds wealth for the dealership instead.

Misconception #5: The Tax Obligations Make Profit Participation Programs Too Risky

Dealers hear terms like "offshore structure," "IRS filings," and "corporate tax returns" and assume participating in a reinsurance program exposes them to significant tax liability, audit risk, or regulatory scrutiny—making the program more trouble than it's worth.

The Reality: Well-structured admin obligor reinsurance programs are designed with tax efficiency in mind, and recent IRS guidance has provided clear, documented protection for auto dealers.

The 2025 IRS Final Regulations: What They Mean for Dealer Captives

On January 14, 2025, the IRS and Treasury Department issued final regulations on micro-captive transactions that created a "Seller's Captive" (Consumer Coverage) exception specifically benefiting auto dealers. Under this exception, F&I captive reinsurance transactions are not deemed a "Listed Transaction" or "Transaction of Interest"—and therefore do not require filing Form 8886—if they meet specific criteria.

The primary requirement: at least 95% of the captive's business must come from issuing or reinsuring contracts purchased by customers unrelated to the dealership or the captive's owners. Since dealers sell F&I products to retail customers with no ownership relationship, compliant dealer F&I captives are effectively green-lit by the IRS.

How the 831(b) Election Makes Tax Efficiency Possible

Property and casualty insurance companies with less than $2.85 million in annual net premiums may elect to be taxed only on investment income under Internal Revenue Code Section 831(b). This means premiums received by the reinsurance company are not subject to federal income tax. Only the investment income earned on reserves is taxable.

This structure allows underwriting profits to accumulate tax-efficiently within the reinsurance entity, with taxation deferred until distributions occur. Dealers should always consult with a qualified tax advisor. That said, tax planning is one of the primary benefits of these programs—and proper structuring is what makes it work cleanly.

Compliance Is Manageable with the Right Partner

A full-service reinsurance partner handles the administrative side entirely, so dealers aren't managing tax complexity on their own. The compliance framework is straightforward when properly structured:

- Manages all legal forms, filings, tax returns, and annual renewals

- Prepares Form 1120PC returns through insurance tax experts

- Provides monthly financial statements for the dealer's tax preparer

- Reinsures only business written through the dealership's own F&I operations

Dealers own 100% of their reinsurance company. That clear separation between the dealership and the captive is what minimizes audit risk—and it's maintained automatically when the program is properly administered.

Frequently Asked Questions

What is an F&I profit participation program?

An F&I profit participation program allows auto dealers to share in the underwriting income and investment returns generated by F&I products they sell—vehicle service contracts, GAP, collateral protection—rather than those profits flowing entirely to third-party providers.

What is an admin obligor reinsurance program?

An admin obligor reinsurance program is a structure where the dealer owns a reinsurance company that receives ceded premiums from F&I product sales, participates in claims outcomes, and earns underwriting and investment profits. The dealer's company is backed by A-rated insurers for catastrophic risk coverage.

Do small or independent dealerships qualify for F&I profit participation programs?

Yes. Dealerships of all sizes—including independent, BHPH, and smaller franchise stores—can qualify. Modern programs are scalable and can be built around a dealer's specific volume and product mix, with some structures viable at as few as 25 to 30 service contracts monthly.

How long does it take to set up a dealer-owned reinsurance company?

Setup timelines vary by structure, but with a full-service partner handling legal formation, filings, and onboarding, most dealers are up and running within 30 to 60 days. The dealer isn't required to manage administrative details throughout the process.

What can dealers do with the profits earned through a reinsurance program?

Accumulated profits can be used for reinvesting in the dealership, purchasing real estate, funding education, or other personal and business goals. The structure acts as a dealer-owned financial asset that builds value over time.

How is dealer-owned reinsurance different from a standard third-party F&I arrangement?

In a third-party arrangement, the provider captures underwriting profits and investment income. In a dealer-owned reinsurance structure, those profits flow back to the dealer's own company, compounding over time as a long-term wealth-building tool the dealer controls.

Ready to stop funding someone else's profit center? DealerRE has helped more than 400 auto dealers nationwide establish and manage their own admin obligor reinsurance companies. Since 1994, DealerRE has managed all legal forms, filings, tax returns, and renewals for its dealer clients—so you can focus on selling F&I products and capturing the profits you've earned. Contact DealerRE today at (804) 824-9533 to request a free dealership analysis and discover how much profit you're leaving on the table.