Introduction

Powersports vehicles—ATVs, UTVs, motorcycles, personal watercraft, and snowmobiles—represent significant investments that face brutal operating conditions. Off-road terrain, high-performance demands, and seasonal storage create mechanical stress far beyond what passenger vehicles experience.

Breakdowns are inevitable, and they're expensive. Labor rates at powersports dealerships typically range from $120 to $175+ per hour, with the average repair bill reaching $4,818 in 2025.

Yet most powersports manufacturers offer factory warranties of just 6 to 12 months—a fraction of the 3-year/36,000-mile standard in passenger vehicles. This gap leaves owners exposed for years of actual riding, creating a massive opportunity for powersports dealers to offer extended service contracts (ESCs) that protect customers and generate substantial F&I profit.

That opportunity comes with a catch. Most dealers who sell third-party warranty products capture only the front-end markup—while the underwriting profit, often the largest share of the revenue, flows straight to the warranty company. Dealers who recognize this are moving toward dealer-owned reinsurance programs that let them capture 100% of the profit stream instead.

This guide explains what powersports extended service contracts are, what they cover, how they generate dealer profit, and—critically—how to build a reinsurance-backed F&I program that transforms service contracts from a commission product into a wealth-building asset.

TLDR

- Powersports ESCs cover mechanical breakdowns on ATVs, UTVs, motorcycles, and PWC after short OEM warranties expire

- OEM coverage on powersports vehicles often lasts just 6-12 months — far shorter than most owners expect

- ESCs are high-margin F&I products, but traditional third-party models send underwriting profit to the provider — not the dealer

- Dealer-owned reinsurance lets dealers capture underwriting profit, control claims, and build long-term assets

- Customers close faster on ESCs that offer low deductibles, transferability, and broad repair networks

Why Powersports Extended Service Contracts Are a Growing Dealer Opportunity

The global powersports market is projected to reach $58.94 billion by 2031, growing at 6.49% annually. North America retained 46.06% of global revenue in 2025 — a significant opportunity for U.S. dealers focused on F&I optimization.

Why breakdowns are more frequent and costly:

Powersports vehicles face operating conditions that accelerate wear:

- Off-road terrain creates constant stress on suspensions, drivetrains, and electrical systems

- High-performance demands push engines and transmissions harder than passenger vehicles

- Seasonal storage and intermittent use introduce maintenance challenges

Repair costs are climbing. Automotive parts prices increased 6.0% in 2025, and powersports components are tracking the same trend. With labor rates above $120/hour and complex systems requiring specialized knowledge, a single major repair can exceed $2,000.

The OEM warranty gap is massive:

| Manufacturer | Vehicle Type | Standard Warranty |

|---|---|---|

| Polaris | ATV, RZR, GENERAL | 6 months |

| Polaris | RANGER, Snowmobiles | 1 year |

| BRP (Can-Am/Sea-Doo) | ATV, SxS, PWC | 1 year |

| Yamaha | WaveRunner | 1 year |

Compare this to passenger vehicles, which typically receive 3-year/36,000-mile basic warranties. The powersports gap leaves customers unprotected for the majority of their ownership period — exactly when mechanical issues are most likely to occur.

That unprotected window is where dealers can step in — and where the real F&I revenue sits.

The dealer-level F&I opportunity:

F&I products have become critical to dealership profitability. By December 2025, nearly 9 out of 10 gross dollars per automotive deal came from F&I, offsetting compressed front-end margins. Top-performing powersports dealers generate $1,800 to $2,500+ in F&I profit per vehicle retailed, compared to the industry average of around $700.

The U.S. extended warranty market grew at 2.7% annually from 2020 to 2025, with projections showing continued expansion. Dealers who structure ESC programs under a dealer-owned reinsurance model — rather than paying third-party providers — keep the underwriting profit on every contract sold, compounding that $700–$2,500 per-unit gap in their favor.

What Powersports Extended Service Contracts Actually Cover

Covered Components and Vehicle Types

Powersports ESCs typically cover these vehicle categories:

- On-road motorcycles and scooters

- ATVs (all-terrain vehicles)

- UTVs and side-by-sides

- Personal watercraft (PWC)

- Snowmobiles

- Golf carts and autocycles

Both new and pre-owned units generally qualify, and most programs accept domestic, Asian, and European-manufactured vehicles.

Coverage tiers:

| Tier | Scope | Components |

|---|---|---|

| Powertrain | Core mechanical components | Engine block, transmission, primary drive, crankshaft, internal gears |

| Stated-Component | Listed parts only | Fuel pump, radiator, alternator, steering rods, master cylinder |

| Exclusionary | Everything except exclusions | Advanced electronics, ABS modules, power windshields, Bluetooth systems |

Exclusionary contracts offer the widest protection: they cover all mechanical and electrical components except items specifically listed as excluded. This structure maximizes customer protection and speeds up the claims process.

Common add-on benefits:

- 24/7 roadside assistance for breakdowns anywhere

- Towing reimbursement to the nearest repair facility

- Trip interruption benefits covering lodging and meals when stranded far from home

- Rental reimbursement while the vehicle is being repaired

- Tire and wheel protection for road hazard damage

- GAP coverage to eliminate total-loss deficiency balances

What's Not Covered

Standard exclusions include:

- Pre-existing damage present before the contract effective date

- Failures caused by inadequate oil, coolant, or missed manufacturer service intervals

- Normal wear items: brake pads, tires, batteries, filters, and cosmetic damage unless explicitly included

- Damage tied to non-OEM aftermarket parts or performance modifications

- Misuse events: racing, commercial operation, towing beyond rated capacity, or negligence

Critical point for dealers: Claims can be denied if owners cannot prove regular maintenance. Communicate this requirement clearly at point of sale and encourage customers to keep service records.

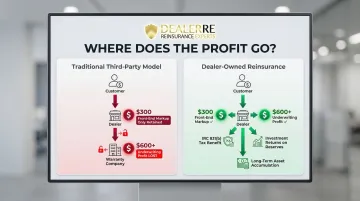

The Powersports Service Contract Profit Problem: Where Dealer Money Goes

Most dealers understand they make money when they sell an extended service contract—they mark up the cost and earn a commission. But what they don't realize is that the bigger profit opportunity happens after the sale.

Here's how the economics work:

When a dealer sells a third-party service contract for $1,500, the warranty company might pay the dealer $1,200 wholesale cost. The dealer marks it up to $1,500 and earns $300 in front-end profit.

But what happens to that $1,200 the warranty company received? Over the life of the contract, the company pays out claims—let's say $600. That leaves $600 in underwriting profit, which the warranty company keeps entirely. The dealer never sees that money again.

What Loss Ratios Reveal

The NAIC reports a 66.50% direct loss ratio for the aggregate warranty line in 2024. This means warranty companies pay out 66.50% of premiums in claims and retain approximately 33.50% to cover administrative expenses and underwriting profit.

If a dealer sells $500,000 in service contract premiums annually and loss ratios run at 50%, that's $250,000 in underwriting profit the dealer forfeited to third-party providers.

How Dealer-Owned Reinsurance Recaptures That Profit

Dealer-owned reinsurance restructures this model entirely. Instead of acting as a sales channel for a warranty company, the dealer becomes the underwriter—establishing their own reinsurance company (typically through an admin obligor structure) and capturing both the front-end markup and the long-term underwriting profit.

How the Admin Obligor Model Works

- The dealer's reinsurance company is the obligor on the contract

- An A-rated insurance carrier backs the program, ensuring customer protection and regulatory compliance

- A third-party administrator (like Assured Vehicle Protection) handles claims adjudication, accounting, and compliance

- The dealer retains control over claims experience and reserves

Beyond Underwriting: The Compounding Financial Benefits

Beyond underwriting profit, dealer-owned reinsurance creates several compounding financial advantages:

- Reduces tax exposure through IRC 831(b), which allows small P&C insurers under $2.2 million in annual net premiums to be taxed only on investment income—not underwriting income

- Generates investment returns on accumulated premiums held in reserve

- Builds a long-term financial asset that can fund real estate purchases, education expenses, or direct dealership reinvestment

DealerRE helps powersports and auto dealers set up and manage these programs with full compliance support, claims administration, and F&I training—handling the complexity while dealers capture the economics.

Key Features Customers Look For in a Powersports Service Contract

Deductible Structure

Customers buy service contracts to eliminate surprise costs. A $500 deductible defeats that purpose.

What works:

- $0 deductible on new units is the strongest selling point

- $25 or less on pre-owned units keeps the value proposition clear

Dealers should understand that a low-deductible contract at a slightly higher price outperforms a high-deductible contract at a lower price. The psychological benefit of "no out-of-pocket cost" is more powerful than marginal savings.

Transferability

A transferable contract increases the vehicle's resale value and makes it more attractive to secondary buyers.

Why it matters:

- Vehicles with transferable warranties command higher resale prices and sell faster

- The warranty acts as a "seal of quality," signaling the vehicle was well-maintained

- Transferability removes buyer objections and builds confidence

Frame this during the F&I presentation: "If you sell or trade this ATV, the warranty transfers to the next owner for a small fee—which can add $500+ to your resale value."

Repair Network Breadth

Customers want assurance they can get service anywhere—at your dealership, a shop near their cabin, or across state lines during a trip.

Strong programs allow repairs at:

- The selling dealer's service department

- Any licensed repair facility in North America

- Manufacturer-authorized service centers

Restricted networks create friction. Customers will ask, "Can I get this fixed anywhere?" Have a clear, confident answer ready before they do.

How Powersports Dealers Can Build a Smarter F&I Program Around Service Contracts

The question isn't "which warranty company should I use?" It's "how do I structure my F&I program so every service contract sold builds long-term profitability?"

Third-party reseller vs. reinsurance-backed program:

| Model | Front-End Profit | Underwriting Profit | Control | Asset Value |

|---|---|---|---|---|

| Third-Party Reseller | Yes | No | Low | None |

| Dealer-Owned Reinsurance | Yes | Yes | High | Accumulates |

Transitioning to a reinsurance-backed model requires setup, compliance management, and ongoing administration — but the payoff is real. Dealers who shift to a dealer-owned structure consistently capture underwriting profits they were previously leaving with a third party — adding a second income stream on every contract sold.

For directional context, top-performing auto dealerships (a closely adjacent benchmark) achieve VSC penetration rates near 84%, versus a national average of 47% — a gap driven almost entirely by structured programs and trained F&I staff.

F&I Training Drives Penetration:

The best service contract program in the industry won't generate penetration if your F&I manager doesn't know how to present it. Dealers should partner with providers who offer:

- Ongoing F&I training (online and in-person)

- F&I menus and presentation tools

- Performance reporting and analytics

DealerRE provides F&I development, training classes, and full administrative support as part of its dealer reinsurance program—ensuring dealers have both the product structure and the selling skills to maximize results.

Three Strategies That Compound F&I Profitability:

Focus on:

- Consultative selling – Position the contract as financial protection, not an upsell

- Bundling – Package service contracts with GAP, tire/wheel, and ancillary products

- Service integration – Route contract claims back to your service department to capture repair revenue alongside the warranty payout

If you're unsure where your current program stands, a dealer analysis is the natural first step — DealerRE's process starts there before recommending any structural changes.

Frequently Asked Questions

What is a powersports extended warranty service contract?

A powersports extended service contract is a contractual agreement that covers the cost of mechanical repairs on ATVs, motorcycles, UTVs, PWC, and similar vehicles after the manufacturer's warranty expires. It can be sold by the dealer, a third-party provider, or backed by the dealer's own reinsurance program.

How long does a powersports extended service contract last?

Coverage duration varies by program. New units can typically receive up to 5 years of additional coverage once the OEM warranty ends. Pre-owned units are often eligible for up to 48 months, depending on mileage and condition.

What does a powersports service contract not cover?

Common exclusions include pre-existing conditions, damage from deferred maintenance, wear-and-tear items (unless specified), and damage from modifications, abuse, or negligence. Always review the contract terms for full exclusion details.

Are powersports extended service contracts worth it for dealers to offer?

ESCs are among the highest-margin F&I products a powersports dealer can offer. Dealers who participate in underwriting profit through reinsurance structures can increase per-unit profitability while improving customer retention and driving service revenue.

Can a powersports service contract be transferred to a new owner?

Transferability depends on the program. The best contracts allow transfer for a small fee, which increases the vehicle's resale value and can help dealers move pre-owned inventory more easily. Confirm transfer provisions before selecting a provider.

What's the difference between an extended warranty and a service contract for powersports vehicles?

A manufacturer's warranty is included with the vehicle purchase and backed by the OEM. A service contract — sometimes called an extended warranty — is a separate agreement purchased through the dealer or a third party, with the obligor being the dealer, a warranty company, or an insurance carrier.

Ready to capture the full profit opportunity from powersports service contracts? DealerRE helps dealers nationwide establish dealer-owned reinsurance programs that turn F&I products into long-term financial assets. For over 28 years, DealerRE has provided compliance support, staff training, and full program administration — making the transition from third-party products to a dealer-owned program straightforward. Contact DealerRE at (804) 824-9533 to learn how reinsurance can transform your F&I performance.