This guide provides a step-by-step roadmap for auto dealers who want to design and launch their own extended warranty program. You'll learn how to structure your program, design coverage tiers, build compliant claims infrastructure, train your team, and track performance. Most importantly, you'll discover why the admin obligor reinsurance model offers the most profitable path: full control of revenue, claims, and customer experience while backed by A-rated insurance carriers.

TLDR

- Dealer-owned extended warranty programs let you capture 100% of underwriting profits instead of paying third-party providers

- The admin obligor reinsurance model combines institutional risk protection with complete brand control and profit retention

- Building a successful program means choosing the right structure, designing coverage strategically, and training F&I staff to sell it

- Admin obligor reinsurance also opens tax planning advantages and lets dealers invest premium income for additional ROI

- Over 400 dealers have used DealerRE to set up and run their own reinsurance programs — handling everything from compliance to claims adjudication

Why Auto Dealers Should Create Their Own Extended Warranty Program

When dealers sell vehicle service contracts through third-party providers, they capture only a flat commission while the provider retains the underwriting profit—the premium reserves remaining after claims are paid. F&I income represents 25.5% of total dealership gross profit, making it a critical stabilizer when vehicle margins compress. Third-party providers extract the lion's share of that value — and dealer-owned programs are how you take it back.

Dealer-owned programs let you capture 100% of the underwriting profits that third-party companies currently keep, growing with every unit sold. Instead of sending premium dollars out the door, you retain them in your own reinsurance company — building wealth while keeping control of the customer relationship.

Control over the claims experience also drives measurable loyalty gains. When service satisfaction exceeds 950 points (on a 1,000-point scale), 86% of customers say they "definitely will" return to the dealer for paid service. Third-party providers profit from claim denials; you profit from customer retention. That difference shows up in faster approvals, better outcomes, and repeat service bay visits.

Dealer-owned reinsurance structures also carry tax and investment advantages that third-party arrangements simply don't offer. Once your reinsurance company exceeds reserve thresholds, earned income from premiums can flow into real estate, dealership expansion, college funding, or other assets — turning F&I profits into personal and business wealth rather than leaving them on the table.

DealerRE has helped over 400 franchise, independent, and BHPH dealers establish admin obligor reinsurance companies since 1994. The team manages all legal forms, filings, tax returns, and renewals — and a number of their clients have been recognized as National Quality Dealer of the Year, across dealer types and market sizes.

Step 1: Choose Your Extended Warranty Program Structure

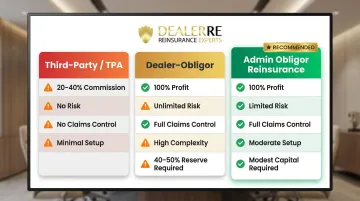

Your program structure determines profit potential, risk exposure, and operational control. Three primary models exist:

Third-Party/TPA Model

You sell another company's product, receive a flat commission (typically 20-40% of premium), and retain zero control over claims, profits, or branding. This is the lowest complexity option but offers minimal upside. The third-party provider captures underwriting profit, manages claims according to their priorities (not yours), and controls the customer experience. You're a commissioned salesperson for someone else's profit center.

Dealer-Obligor (Self-Insured) Model

You assume direct risk for all claims, requiring substantial capital reserves and careful actuarial planning. NAIC Model 685 requires obligors to maintain a 40% funded reserve plus a 5% security deposit, creating significant cash flow strain.

While you gain full control and profit retention, financial exposure is substantial and unbounded. Most dealers lack the capital cushion to manage this risk prudently.

Admin Obligor Reinsurance Model (Recommended)

Your dealership establishes its own reinsurance company that becomes the obligor on vehicle service contracts, but institutional risk is backed by A-rated insurance carriers. You capture the economics without unbounded liability. This model combines brand control and profit capture with institutional risk protection—the optimal balance for independent, franchise, and BHPH dealers.

In practice, your reinsurance company administers and underwrites F&I products sold to customers. Claims are paid from premium reserves you control. Ultimate liability rests with A-rated carriers that reinsure your company, limiting personal exposure to formation costs plus accumulated earnings.

That risk protection in place, the setup process is more straightforward than most dealers anticipate. DealerRE coordinates company formation, state filings, and compliance documentation — typically completing the process within a few weeks. For BHPH dealers, admin obligor programs can also protect vehicles from mechanical breakdown and insurance losses funded by the customer base, directly addressing the challenge of keeping customers on the road and making payments.

Comparison Summary:

| Feature | Third-Party/TPA | Dealer-Obligor | Admin Obligor Reinsurance |

|---|---|---|---|

| Profit Retention | 20-40% commission | 100% | 100% |

| Risk Exposure | None | Unlimited | Limited to capital invested |

| Claims Control | None | Complete | Complete |

| Setup Complexity | Minimal | High | Moderate (handled by partner) |

| Capital Requirements | None | 40-50% reserve | Modest initial investment |

Step 2: Design Your Coverage Options and Contract Terms

Effective coverage design balances customer affordability with sustainable profitability. Structure your program around three coverage tiers:

| Tier | What's Covered | Typical Cost (3-Year) | Why It Sells |

|---|---|---|---|

| Powertrain | Engine, transmission, drivetrain | $1,800–$2,500 | Addresses catastrophic failure fear at lowest price; highest penetration rates |

| Mid-Level / Stated Component | Powertrain + electrical, A/C, steering, suspension | $2,500–$3,500 | Middle ground between affordability and broader protection |

| Comprehensive / Bumper-to-Bumper | Everything except explicitly excluded components | $3,000–$5,000+ | Luxury and European vehicles command premium pricing due to higher parts and labor costs |

Common add-ons increase per-vehicle profitability:

- GAP Protection: Covers loan deficiency in total loss situations

- Tire and Wheel: Protects against road hazard damage

- Roadside Assistance: 24/7 towing and emergency services

- Appearance Coverage: Paint, fabric, and windshield protection

Rate-setting requires actuarial grounding. Coverage pricing depends on vehicle age, mileage, make/model, and historical claims data — work with your reinsurance partner or an actuarial consultant to establish sustainable rates. Asian manufacturers typically generate lower claims frequency than European brands; high-mileage vehicles require higher premiums than late-model inventory.

Define contract terms clearly to avoid disputes:

- Coverage period: Duration in months AND miles (e.g., 48 months/48,000 miles)

- Deductible structure: $0, $100, or $200 per visit

- Exclusions: List ineligible components explicitly

- Transferability: Allows coverage transfer to subsequent owners, increasing vehicle resale value

- Cancellation/refund terms: Pro-rata or flat cancellation fee structure

F&I menu presentation shapes how customers respond to each tier. Position warranties as value and protection — not cost — and use a tiered menu that lets customers choose their coverage level visually. Present it after discussing the vehicle purchase, when customers are already thinking about ownership costs. DealerRE's F&I menus are built specifically for this moment, with tiered layouts that walk customers through their options clearly without overwhelming them.

Step 3: Set Up Claims Processing and Compliance Infrastructure

Claims Administration Requirements

A compliant, customer-friendly claims process requires:

- Intake mechanism: Establish clear pathways for customers to file claims — phone hotline, online portal, or direct authorization through repair shops. Fast, accessible intake reduces frustration and improves satisfaction scores.

- Eligibility verification: Define criteria for covered repairs (component failure due to defect or normal wear) versus exclusions (lack of maintenance, abuse, pre-existing conditions). Clear criteria speed adjudication and cut disputes.

- Timely adjudication: Process claims within 24–48 hours to minimize customer downtime. Delays push customers toward competitors' service bays.

- Payment workflow: Establish direct payment to repair facilities or reimbursement to customers. Straightforward payment processes improve service retention and encourage repeat business.

Compliance Landscape

Federal requirements: The FTC's Magnuson-Moss Warranty Act governs service contract disclosure and documentation. Contracts must clearly state terms, coverage, and exclusions in plain language.

State-level regulations vary significantly. Most states require either heavily funded reserve accounts (40-50% of premiums) or a Contractual Liability Insurance Policy (CLIP) to guarantee claims. California, Florida, Texas, and other states maintain distinct reserve and licensing requirements. Work with a qualified reinsurance specialist to ensure compliance across all states where you do business — attempting to navigate this independently creates legal and financial risk.

Financial Tracking and Reporting

Track these metrics consistently:

- Premium income — total premiums collected by product line

- Claims paid — aggregate and per-contract claim costs

- Reserve balances — unearned premiums and claim reserves

- Program profitability — underwriting profit after claims and administrative costs

DealerRE's full-service administration includes financial reporting and bookkeeping — monthly statements and annual reports covering all reinsurance operations — so dealers avoid managing complex insurance accounting in-house.

Step 4: Train Your Team, Launch, and Continuously Optimize

Prepare Your F&I and Sales Staff

Even perfectly structured programs underperform without trained staff. F&I managers must understand product details, position warranties as customer value rather than dealer profit, and handle objections confidently. When staff can't answer questions clearly, customers disengage — no matter how strong the product.

A phased launch reduces risk significantly. Start with your top 2-3 F&I managers to:

- Refine the pitch and identify common objections

- Validate pricing against real customer responses

- Collect feedback before standardizing the presentation

Then roll out dealership-wide with a uniform F&I menu and process. This builds internal advocates who can train peers rather than relying entirely on outside instruction.

DealerRE provides dealership-specific F&I training in both classroom and online formats, including mobile-accessible daily lessons through their certification program "F&I Products and Professional F&I Selling Process & Disclosures." The program covers product knowledge, ethical selling practices, and disclosure compliance — giving staff a foundation they can apply immediately on the floor.

Track Performance and Scale

Monitor these key metrics monthly:

Warranty penetration rate: Percentage of vehicles sold with a service contract. NADA reports penetration rates of 45.7% for new vehicles and 47.6% for used vehicles as national benchmarks. If you're below 40%, investigate pricing, presentation, or training gaps.

Average contract revenue per unit: Public dealer groups reported average F&I PVR of $2,515 in Q2 2025. Track your warranty-specific revenue contribution to understand program impact on overall F&I performance.

Claims loss ratio: Claims paid divided by premiums earned. Loss ratios consistently exceeding 70-80% signal mispriced coverage or adverse selection. Adjust pricing for high-loss segments promptly.

Customer retention rate: Measure how many warranty customers return for service versus one-time visitors. 78% of owners with factory warranties and 86% with service contracts report being "very satisfied" and always visit the dealership for service. Your dealer-owned program should match or exceed these benchmarks.

Use these metrics to drive ongoing improvements:

- Adjust pricing for vehicle segments with unfavorable loss ratios

- Add coverage tiers based on customer demand patterns

- Identify top-performing F&I managers and replicate their approach across the team

- Test bundled offerings (warranty + GAP + tire/wheel) to increase penetration and per-vehicle revenue

Frequently Asked Questions

How much does an extended warranty usually cost?

Extended warranty costs vary widely based on vehicle age, mileage, make/model, and coverage level. Powertrain-only coverage typically costs between $1,800 and $2,500, while comprehensive bumper-to-bumper plans range from $3,000 to $5,000+. Dealer-branded programs can be priced competitively, with the dealer capturing profit margin rather than a third party.

What is the difference between a dealer-branded warranty and a third-party extended warranty?

A dealer-branded program keeps all underwriting profit and claims control within your dealership, allowing you to deliver faster, more favorable claim outcomes and drive service revenue. Third-party warranties route premiums and profits to external companies, leaving you with only a flat commission and no control over the customer's claim experience.

What is an admin obligor reinsurance company and how does it benefit dealers?

In an admin obligor reinsurance structure, your own reinsurance company is the obligor on vehicle service contracts, backed by A-rated insurance carriers. You capture 100% of warranty program economics while institutional insurance provides the risk backstop, limiting your liability and ensuring claim-paying ability.

How long does it take to set up a dealer-owned extended warranty program?

Setup timelines vary based on program complexity and your reinsurance partner's process. With a full-service partner like DealerRE, company formation and onboarding typically wrap up in a matter of weeks, with all legal filings, compliance documentation, and staff training handled on your behalf.

Do BHPH dealers need a different type of extended warranty program?

Yes. BHPH dealers benefit from admin obligor reinsurance programs specifically structured to protect vehicles from mechanical breakdown while being funded by the customer base. This delivers both risk management and a built-in profit tool tailored to the BHPH model.

What compliance requirements apply to dealer-run extended warranty programs?

Requirements include FTC Warranty Rules, state-level service contract regulations, and reserve or licensing obligations that vary by state. Most states require 40–50% funded reserves or a Contractual Liability Insurance Policy (CLIP). Work with a qualified reinsurance specialist to ensure all filings, renewals, and compliance documentation remain current across all jurisdictions where you operate.