Introduction

Most auto dealers selling vehicle service contracts (VSCs) are handing over a significant share of backend F&I profits to third-party warranty companies—money that could flow directly to the dealer's own business. The fundamental question is simple: if your warranty company weren't making a profit from the VSCs you sell, would they continue doing business with you? The answer reveals the core opportunity: third-party providers profit from premium reserves not used to pay claims, and those profits rightfully belong to dealers who generate the sales volume.

This article covers what a VSC reinsurance subsidiary is, what changed in 2008 for dealer-owned reinsurance structures, how the admin obligor model works, and what dealers need to know to evaluate forming their own subsidiary.

TLDR:

- Dealer-owned reinsurance subsidiaries capture underwriting profits that third-party warranty companies typically retain

- IRS Private Letter Ruling 200843026 (2008) established clear tax treatment for VSC reinsurance entities

- Admin obligor structures use A-rated carrier backing to protect dealers while allowing profit capture

- Franchise, independent, retail, and BHPH dealers can each form a subsidiary tailored to their operations

What Is a Vehicle Service Contract Reinsurance Subsidiary?

A vehicle service contract (VSC) is a contractual agreement sold at the dealership that protects the vehicle buyer against economic loss from mechanical breakdowns not covered by the manufacturer's warranty. Coverage typically includes repair costs, rental reimbursement, and roadside assistance for a defined term or mileage period.

Reinsurance is a contract whereby one insurer transfers or "cedes" to another insurer all or part of the risk it has assumed—essentially, insurance for insurance companies. In the dealership context, a VSC reinsurance subsidiary is a company owned by the dealer that accepts the insurance risk underlying VSCs sold at the dealership.

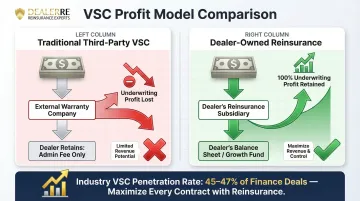

How Dealer-Owned Reinsurance Differs from Third-Party VSC Sales

Rather than remitting premiums to an outside warranty company and watching those reserves and profits disappear, the dealer's own entity captures:

- Underwriting income

- Reserve investment returns

- Unearned premium balances

When dealers sell third-party VSC products, they earn front-end commission but forfeit all backend underwriting profit. The dealer-owned model allows dealers to maintain the same gross profit at the point of sale and capture the underwriting profits as contracts expire.

History and Dealer Types

The concept of dealer-owned reinsurance has existed for more than thirty years, when dealers first began marketing credit life and extended vehicle service contracts through their own entities. Since then, dealer-owned reinsurance structures have expanded significantly—today covering VSCs, GAP, collateral protection, and ancillary products, giving dealers a direct stake in every contract they sell.

Dealers who can benefit include:

- Franchise dealers

- Independent dealers

- Retail dealers

- Buy Here Pay Here (BHPH) operators

The structure adapts to different sales volumes, product mixes, and risk profiles, making it accessible to dealers selling 30+ vehicles per month.

Why 2008 Was a Turning Point: The IRS Private Letter Ruling

IRS Private Letter Ruling 200843026, issued July 21, 2008, settled a long-standing question for dealer-owned VSC reinsurance. The IRS ruled that vehicle service contracts issued by a dealer-affiliated entity qualify as insurance contracts for federal income tax purposes, confirming that the entity qualifies as an "insurance company" under IRC §831(c) when more than half its business involves issuing such contracts.

What the Ruling Confirmed

The IRS determined that the indemnification agreement between the VSC issuer and the backing insurer constitutes a reinsurance contract for federal income tax purposes, satisfying three core elements: insurance risk, shifting and distribution of that risk, and the arrangement qualifying as insurance in its commonly accepted sense.

The ruling explicitly noted that the VSC arrangement distributed risk because the taxpayer accepted a "large number of risks" and indemnified holders for economic loss arising from mechanical breakdowns—satisfying the "law of large numbers" principle essential to legitimate insurance operations.

Practical Impact for Dealers

This ruling gave dealer-owned subsidiaries clear guidance on how to account for premiums, claims reserves, and ceding arrangements under subchapter L of the Internal Revenue Code—removing the legal and tax uncertainty that had kept many dealers on the sidelines.

The tax benefits followed directly from that clarity. Under the IRC §831(b) election, qualifying small insurance companies can elect to be taxed only on investment income, provided net written premiums don't exceed $2,200,000 annually (subject to inflation adjustments). In practice, this means underwriting income—premiums minus claims—flows to the dealer's reinsurance company largely tax-free, with only investment earnings subject to federal income tax.

Industry Context Around 2008

By 2008, dealer-owned reinsurance programs had already expanded well beyond early adopters—reinsurance companies were actively driving how extended vehicle service contracts were structured and sold across the country. The IRS ruling confirmed the tax treatment that dealers and their advisors had been building toward for years. It also established compliance standards that separated legitimate VSC reinsurance structures from abusive micro-captive arrangements later targeted by IRS Notice 2016-66.

How the Admin Obligor VSC Reinsurance Model Works

The admin obligor structure positions the dealer's reinsurance subsidiary as the obligor on vehicle service contracts—the entity legally responsible for paying covered claims—while critically, the subsidiary itself is insured by an A-rated insurance carrier. This provides dealers with profit upside while maintaining institutional insurance backing.

Premium Flow

- Customer purchases VSC at the dealership; premium is collected

- Premium is ceded to the dealer's reinsurance subsidiary

- Subsidiary retains funds in a reserve account (rather than sending them to a third-party warranty company)

- A-rated carrier provides backstop coverage, guaranteeing claims payment

For franchise and retail dealers, the full premium flows into the reinsurance company immediately. For BHPH dealers, premiums are financed over the contract term—dealers are billed monthly as they receive customer payments, protecting cash flow and lending pool resources.

Claims Adjudication and Reserve Control

When a covered mechanical breakdown occurs:

- Claim is submitted and adjudicated per contract terms

- Payment is made from reserves held within the dealer's own reinsurance structure

- Dealers gain direct visibility into claims experience and reserve levels

Unlike third-party VSC providers, this structure lets dealers route claims back to their own service facilities, keeping repair revenue inside the dealership.

Investment Component

Premium reserves accumulate within the dealer's subsidiary rather than a third party's balance sheet. These reserves can be invested to generate additional return:

- Conservative phase: Initially, funds are invested in government bonds per regulatory guidelines until reserves exceed 125% of unearned premiums

- Aggressive phase: Once reserves exceed the 125% threshold, excess funds may be invested at the direction of company ownership

Investment uses:

- Real estate purchases

- Reinvestment into dealership operations

- Education funding for children

- Other vehicles (watercraft, etc.)

Under an IRC §831(b) election, investment income is the only taxable portion of the entity's revenue, making this structure a tax-efficient way to build long-term wealth outside the dealership's operating income.

Risk Management Layer

The A-rated insurer backing means that even if the dealer's subsidiary experiences an adverse claims period, the institutional carrier absorbs losses that exceed the reserve threshold. This gives dealers the profit upside of self-insurance without the catastrophic downside risk of being fully self-insured.

If the dealer's reinsurance company cannot meet its financial obligations due to inadequate reserves, ultimate liability for claim payments rests with the direct writing insurance company—not the dealer's personal assets or dealership operations.

Key Benefits of a Dealer-Owned VSC Reinsurance Subsidiary

Profit Recapture

VSC penetration runs approximately 45.7% for new vehicles and 47.6% for used vehicles, with average retail prices ranging from $1,500 to $3,500. Third-party warranty companies profit from the spread between premiums collected and claims paid — profits that dealers forfeit under traditional commission arrangements.

By owning their own reinsurance subsidiary, dealers capture 100% of the underwriting profit that third-party providers were previously retaining. Dealers maintain the same front-end gross margin while adding a substantial backend profit layer as contracts expire.

Tax Planning Advantages

Qualifying as an insurance company under §831(c) provides meaningful tax planning opportunities. Companies with less than $2,200,000 in annual net premiums may elect IRC §831(b) status, and pay taxes only on investment income. Underwriting income flows to the reinsurance company tax-deferred, creating a tax-deferred wealth-building structure.

Dealers should work with a qualified tax advisor to quantify the benefit for their specific business structure. DealerRE coordinates with insurance tax experts who prepare Form 1120PC annually, ensuring compliance with IRS standards and minimizing audit risk.

Customer Experience and Claims Control

When dealers control the claims adjudication process, they can set service standards that align with their dealership's customer experience goals. This reduces disputes, improves satisfaction, and protects the dealer-customer relationship for future vehicle purchases.

Direct claims control creates advantages that third-party programs simply can't replicate:

- Faster claim resolution by keeping repairs in-house or at approved shops

- Service standards set to match the dealership's own customer experience benchmarks

- Stronger retention, since a positive ownership experience drives repeat vehicle purchases

Forming a VSC Reinsurance Subsidiary: What Dealers Need to Know

Formation Requirements

Forming a VSC reinsurance subsidiary involves several steps:

- Establishing a legal entity (typically in a favorable domicile state with minimal capital investment requirements)

- Completing state insurance filings and securing regulatory approvals

- Capitalizing the company to meet regulatory minimums

- Selecting an administrator to handle claims adjudication, compliance, and financial reporting

- Training F&I staff on the new product structure

DealerRE describes its setup as "fast and easy," though timelines vary by domicile state and capitalization. The company coordinates all licensing, tax preparation, legal forms, filings, and renewals on behalf of dealers.

Ongoing Administrative Obligations

Once formed, the subsidiary requires ongoing management:

- Tax return preparation (Form 1120PC for §831(b) companies)

- State filing renewals

- Actuarial reserve reviews and claims monitoring

- Performance reporting and financial statements

- Regulatory compliance and documentation

DealerRE partners with Assured Vehicle Protection (AVP) to handle all of the above — claims adjudication, accounting records, monthly financial statements, annual reports, and ongoing compliance — so dealers stay focused on selling cars, not managing paperwork.

Key Selection Criteria When Choosing a Reinsurance Partner

Not all reinsurance programs are structured the same. Here's what to evaluate before committing:

- Track record with comparable dealers — DealerRE has 28 years of experience serving over 400 dealers nationwide, including National Quality Dealer of the Year recipients and NIADA board members.

- A-rated insurer backing — Programs should be backed by an A-rated carrier to guarantee claims payment and protect against catastrophic loss. DealerRE's admin obligor structure meets this standard.

- F&I training depth — A strong partner provides more than setup. DealerRE offers online and in-person F&I training, development programs, and customized menus so your team can sell and administer reinsured products with confidence.

- Transparent fee structure — All program economics should be disclosed upfront, with no surprises. DealerRE commits to no hidden fees as a baseline expectation.

- End-to-end administration — From initial setup through ongoing compliance, confirm your partner handles the full operational load. (See the administrative obligations outlined above for the full scope.)

Frequently Asked Questions

What is reinsurance in the automotive industry?

In the automotive context, reinsurance refers to arrangements where a dealer-owned or affiliated company assumes the insurance risk underlying vehicle service contracts and F&I products. This allows the dealership to capture underwriting profits and reserve investment returns that would otherwise go to third-party warranty or insurance companies.

What is a vehicle service contract reinsurance subsidiary?

A VSC reinsurance subsidiary is a company owned by the dealer (or dealer's principals) structured as an insurance entity. It accepts ceded risk from vehicle service contracts sold at the dealership and is backed by an A-rated insurer under the admin obligor model, allowing the dealer to retain premiums and profits within their own business.

What is the admin obligor model in dealer reinsurance?

The admin obligor model means the dealer's reinsurance company is named as the obligor on the VSC (responsible for paying claims) while simultaneously being insured by an A-rated carrier. This gives the dealer control of the reserves and profits while maintaining institutional insurance backing against catastrophic loss.

What are the tax advantages of a dealer-owned reinsurance company?

Per IRS guidance including Private Letter Ruling 200843026 (2008), VSC-issuing entities can qualify as insurance companies under IRC §831(c), potentially enabling favorable tax treatment on underwriting income through the §831(b) election. A qualified tax advisor can help determine the specific benefit for each dealer's situation.

How long does it take to set up a VSC reinsurance subsidiary?

Formation timelines vary based on domicile state, capitalization, and chosen administrator. Working with an experienced reinsurance consultant who handles all filings and legal requirements can significantly accelerate the process — DealerRE's specialists manage every step to keep setup fast and straightforward.

Can any type of auto dealer form a VSC reinsurance subsidiary?

Franchise dealers, independent dealers, retail dealers, and BHPH operators can all form a VSC reinsurance subsidiary. Dealers selling 30+ vehicles monthly are the strongest candidates. Optimal structure, reserve requirements, and product mix vary by dealer type and are best assessed with an experienced reinsurance advisor.