Introduction

Third-party warranty providers and administrators are capturing significant profits that dealers could be keeping—and a dealer-owned warranty company (DOWC) can change that equation, with major tax advantages built in.

When dealers sell extended warranties, GAP insurance, and other F&I products through third-party vendors, those vendors retain the underwriting profits (the difference between premiums collected and claims paid). That spread represents substantial wealth leaving the table.

A DOWC shifts that arrangement entirely. By owning the insurance entity that underwrites your F&I products, you capture 100% of the underwriting profits that third-party providers were keeping.

The tax advantages go well beyond capturing lost profits. DOWCs are treated as insurance companies for federal income tax purposes under IRC Section 816(a), which unlocks a set of tax rules most dealers never knew existed. These rules differ fundamentally from standard corporate taxation and offer multi-decade tax deferral through tools unavailable to typical dealership structures.

This guide covers:

- How a DOWC qualifies for insurance company tax treatment under federal law

- How taxable income is calculated using insurance-specific rules

- The major tax benefits available, including NOL carryforwards and the Section 831(b) election

- How DOWC taxation compares to other F&I participation structures

- Formation requirements, state selection considerations, and ongoing compliance obligations

If you're selling 30+ units a month and still sending underwriting profits to a third party, the tax structure alone may be reason enough to reconsider.

TLDR

- A DOWC is a domestic C-corporation qualifying under IRC Section 816(a) and taxed under insurance-specific rules, not standard corporate rules

- The defining tax benefit: DOWCs deduct 80% of unearned premium reserves annually, typically generating NOLs that offset taxable income for decades

- Non-life insurance company NOLs carry back 2 years and forward 20 years with no 80% income limitation

- Smaller DOWCs below the annual premium threshold may elect Section 831(b) treatment, taxing only investment income while excluding underwriting income entirely

- DOWC taxation requires specialized expertise; partnering with an experienced reinsurance and F&I administrator is critical to compliance and maximizing benefits

What Makes a DOWC an "Insurance Company" for Federal Tax Purposes

The IRC Section 816(a) Threshold

Under IRC Section 816(a), a company qualifies as an insurance company for federal income tax purposes if more than half of its business involves issuing insurance or annuity contracts, or reinsuring risks underwritten by insurance companies. This is a federal tax definition, separate from state insurance regulatory requirements.

The "more than half" threshold is strict. A DOWC that lets non-insurance administrative services or claims processing overshadow its underwriting activities risks losing this tax status entirely.

Per Se C-Corporation Classification

Meeting this threshold triggers a significant tax consequence: the DOWC is classified as a "per se" C-corporation under Treas. Reg. Section 301.7701-2(b)(4), meaning it cannot elect S-corp or pass-through treatment. The entity must:

- File a corporate tax return

- Pay tax under non-life insurance company rules in Subchapter L of the IRC

- Accept the 21% corporate tax rate under IRC Section 11(b) as amended by the Tax Cuts and Jobs Act (TCJA)

Note: Tax rates are subject to change. Dealers should consult with a tax professional about current rates and proposed legislative changes.

Risk Shifting and Risk Distribution Requirements

Insurance company tax classification requires both "risk shifting" and "risk distribution" in the contracts — the DOWC must actually bear insurance risk, not just act as a pass-through. Two distinct tests apply:

- Risk shifting: The dealership or consumer must transfer the financial consequences of vehicle breakdowns to the DOWC. The risk of loss must genuinely move away from the original party.

- Risk distribution: The DOWC must pool enough independent contracts to apply the law of large numbers, reducing the chance that a single large claim wipes out premium reserves. Pooling hundreds of vehicle service contracts satisfies this requirement.

In Private Letter Ruling 201314020, the IRS concluded that vehicle service contracts issued by obligor companies constituted insurance contracts because they were aleatory contracts indemnifying policyholders for economic loss, and the companies distributed risk by accepting a large number of risks.

How a DOWC Calculates Its Taxable Income

The Two-Part Gross Income Formula

Under IRC Section 832, gross income for a DOWC consists of "underwriting income" plus "investment income."

- Underwriting income = premiums earned minus losses incurred and expenses incurred

- Investment income = interest, dividends, and rents received during the year (adjusted for accruals)

The combination of both forms the DOWC's gross income base.

The Critical 80% Unearned Premium Reserve Deduction

The most significant tax advantage for DOWCs lies in the unearned premium reserve (UPR) deduction under IRC Section 832(b)(4). Only 20% of unearned premiums on outstanding business at year-end are treated as earned (taxable)—the other 80% is deducted.

Because premiums come in upfront but claims are paid out over time, this 80% deduction almost always creates net negative taxable income in the early years of operation.

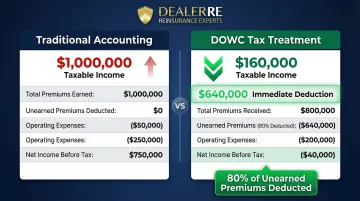

For example, if a DOWC writes $1,000,000 in premiums in year one and ends the year with $800,000 in unearned premiums (contracts still outstanding):

- Traditional accounting: $1,000,000 taxable income

- DOWC tax treatment: Only $160,000 taxable ($800,000 × 20%)

- Result: $640,000 immediate tax deduction ($800,000 × 80%)

Allowable Deductions Under IRC Section 832(c)

DOWCs can deduct:

- Losses incurred – claims paid on vehicle service contracts, adjusted for salvage and reinsurance

- Ordinary and necessary business expenses – operational costs and administrative fees

- Commissions paid – dealer commissions on contract sales are fully deductible

- Interest and other standard corporate deductions

Administration costs, acquisition costs, and sales commissions all reduce taxable income further, compounding the NOL effect.

The Net Operating Loss Mechanism

Stack the 80% UPR deduction on top of operating expenses, and most DOWCs generate net operating losses annually for an extended period—potentially 5 to 20 years, depending on premium volume and claims experience. The NOL doesn't eliminate income; it defers the tax obligation until contracts run off and the reserve unwinds. For dealers writing significant F&I volume, that deferral can represent hundreds of thousands of dollars held in the company rather than sent to the IRS each year.

Non-Life Insurance Company NOL Carryforward Rules

IRC Section 172(b)(1)(C) provides special NOL rules for non-life insurance companies:

- Carryback: 2 years

- Carryforward: 20 years

- 100% offset: Non-life insurance company NOLs are NOT subject to the 80% taxable income limitation that applies to most corporations—they can offset 100% of taxable income in carryforward years

This exemption survived the Tax Cuts and Jobs Act of 2017 intact. In practical terms, a DOWC that accumulates $2,000,000 in NOL carryforwards can fully offset $2,000,000 in future taxable income—dollar for dollar—once the reserve begins to unwind.

The Major Tax Benefits of a DOWC: Deferral, NOLs, and the 831(b) Election

Significant Long-Term Tax Deferral

The combination of the UPR deduction and NOL carryforward rules means a well-structured DOWC can have near-zero federal taxable income for 5 to 20+ years, depending on volume, product mix, and claim experience.

Inside the entity, underwriting profits and investment income accumulate without triggering immediate tax. This treatment mirrors the statutory framework property and casualty (P&C) insurance companies have operated under for decades — and it's what makes the DOWC structure a genuine long-term wealth-building tool for dealers.

Key reasons this deferral is powerful:

- Profits compound inside the entity without annual tax drag

- Investment income grows on a pre-tax basis until distributed

- NOL carryforwards can offset future taxable income across multiple years

The Section 831(b) Election: Tax-Free Underwriting Income

If a DOWC's net written premiums (or direct written premiums, if greater) fall below the annual threshold set by the IRS, the company can elect Section 831(b) treatment.

For 2026, the threshold is $2,900,000 according to IRS Revenue Procedure 2025-32.

Under this election:

- Underwriting income is excluded from taxation entirely

- Only investment income is taxed at the standard 21% corporate rate

- The tax savings on underwriting income can be substantial for dealers with high premium volume under the threshold

Two additional requirements apply:

- The DOWC must meet diversification requirements (no more than 20% of premiums from any single policyholder, or meet ownership tests)

- The election must be made by the filing deadline for that taxable year — it cannot be made retroactively

Once made, the election applies to all future years as long as requirements continue to be met. The election can only be revoked with IRS consent.

That continuity matters — because when premium volume fluctuates near the threshold, it creates a specific tax complication worth understanding before it becomes a problem.

Critical NOL Interaction Under IRC Section 831(b)(3)

NOLs cannot be carried to or from a year in which the company is under 831(b) treatment. If a dealer fluctuates between 831(a) and 831(b) years due to premium volume changes, NOLs may be stranded.

Takeaway: Careful volume planning with a qualified DOWC administrator is essential to avoid stranding NOLs and to maximize the value of both 831(b) treatment and NOL carryforwards.

DOWC Tax Treatment Compared to Other Dealer F&I Profit Participation Structures

| Structure | Tax Treatment | Key Characteristics |

|---|---|---|

| 1+ Commission & Guaranteed Retro | Ordinary income in year received | No deferral; immediate taxation at full ordinary rates |

| Retrospective Commission | Ordinary income with some timing difference | Payment delayed but still taxed as ordinary income when received |

| PARC/CFC | Distributions taxed as qualified dividends | Long-term capital gains rates; offshore complexity; TCJA reporting requirements |

| NCFC | Qualified dividend treatment with deferral | Involves multiple dealers; shared risk pool |

| DOWC | Multi-decade NOL deferral; 831(b) underwriting exclusion | Domestic formation; regulatory compliance costs; no 80% NOL limitation |

Key Practical Differences

Two distinctions stand out when comparing DOWCs to the alternatives:

- Premium taxes: DOWCs pay federal and state income taxes but are NOT subject to premium taxes — unlike products sold through third-party carriers, which carry that added cost.

- Regulatory complexity: Domestic formation requires compliance overhead that offshore structures avoid, but the tradeoff is greater transparency and simpler day-to-day management.

Admin obligor reinsurance programs offer similar tax planning advantages to the DOWC structure. If you're weighing volume, risk tolerance, and tax goals, a specialist can help you identify the right fit. DealerRE handles tax planning, filings, and compliance management as part of its program. Contact DealerRE at (804) 824-9533 to discuss your specific situation.

Formation, State Selection, and Ongoing Tax Compliance

State Selection and Capitalization Requirements

Because a DOWC is a licensed insurance entity, state of formation matters significantly for capitalization requirements and ongoing regulatory obligations.

Common captive insurance domiciles include:

- Delaware

- Utah

- Vermont

- Tennessee

- South Carolina

These states typically require minimum statutory capital in the range of $250,000 to $1,000,000+. This capital must be committed before the DOWC can begin writing coverage.

Exact minimums vary by state and are subject to change — dealers should verify current requirements with a licensed advisor before selecting a domicile.

Accepted forms of capital include cash, cash equivalents, or an irrevocable letter of credit from an approved bank.

The Seeding Period Concept

Once the DOWC is approved and operational, it typically takes 12 to 24 months for claim reserves to build to actuarial adequacy. During this seeding period, the tax benefits are not yet fully realized.

After the seeding period, the full deferral and NOL benefits come online. Dealers should factor this timeline into their financial planning before committing to a DOWC structure.

Ongoing Compliance Requirements

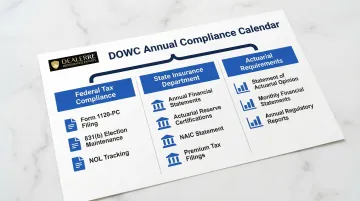

DOWCs must maintain strict compliance across multiple regulatory domains:

Federal tax compliance:

- Annual tax returns filed as a non-life insurance company on Form 1120-PC (distinct from standard corporate returns)

- Election and maintenance of 831(b) status if applicable

- NOL carryforward tracking and documentation

State insurance department compliance:

- Annual financial statements

- Actuarial reserve certifications

- National Association of Insurance Commissioners (NAIC) annual statement formats

- State premium tax filings (where applicable)

Actuarial and financial reporting requirements add another layer. A qualified actuary must issue a Statement of Actuarial Opinion (SAO) annually, while monthly financial statements track premiums, claims, and reserves. Annual reports to state regulators round out the calendar obligations.

Given the complexity across federal, state, and actuarial requirements, dealers need advisors with direct DOWC experience — not general CPA firms unfamiliar with insurance company taxation. DealerRE manages all legal forms, filings, tax returns, and renewals for dealer clients, removing that administrative burden entirely. Reach DealerRE at (804) 824-9533 to learn more.

Frequently Asked Questions

What is a dealer-owned warranty company?

A DOWC is a domestic C-corporation wholly owned by a dealer or dealer group, serving as the obligor for service contracts and F&I products. It lets the dealer capture underwriting profits and access insurance company tax treatment rather than paying those profits to a third party.

Are extended warranties included in the tax basis?

In a DOWC, extended warranty premiums form the gross premiums written—not a "tax basis" in the traditional asset sense. Tax treatment flows through the DOWC's underwriting income and UPR deduction, not the dealer's vehicle cost basis.

Are warranties taxable in FL?

Florida's taxability of service contracts depends on how the product is structured and sold. This is a state sales tax question separate from the DOWC's federal income tax treatment—consult a SALT advisor for state-specific guidance.

Are extended warranties taxable in New York?

New York's taxability of service contracts depends on how the contract is written and delivered. This is a state sales tax question distinct from DOWC federal tax structure—consult a SALT specialist for New York-specific rules.

What is the Section 831(b) election for a DOWC?

Section 831(b) is an optional IRS election available to qualifying small insurance companies (those below the annual written premium threshold of $2,900,000 for 2026). It allows the company to pay tax only on investment income—meaning underwriting income is completely excluded from federal taxation.

How long does it take to see tax benefits from a DOWC?

Formation and regulatory approval typically takes 3-6 months, followed by a 12-24 month seeding period before NOL-driven tax deferral reaches full effect. Most dealers see significant tax deferral in years 2-3, with benefits compounding over time.

Ready to explore whether a DOWC is right for your dealership? Contact DealerRE at (804) 824-9533 or visit dealerre.com to request a personalized business analysis. DealerRE specializes in admin obligor reinsurance programs, providing full-service administration, tax planning, and compliance management so dealers keep the profits that once went to third-party providers.