Introduction

Franchise auto dealerships face a more complex insurance landscape than independent used-car lots. Large inventories, busy service departments, and dozens of employees across sales and service all create coverage obligations that generalist policies cannot meet.

Contractual relationships with Original Equipment Manufacturers (OEMs) add another layer — most mandate specific minimum limits that go well beyond what state law requires.

This guide covers the core coverage types franchise dealers need, what makes their insurance requirements unique compared to independents, the key cost drivers that affect premiums, and how to secure the right quote for your operation. Standard dealership insurance addresses physical and liability risks — hail damage, customer slip-and-falls, employee injuries — but franchise dealers also run F&I operations that carry their own distinct financial exposure, covered separately in this guide.

TLDR:

- Franchise dealers need specialized insurance packages including garage liability, dealer's open lot (DOL), garage keepers, dealer plate, E&O, and workers' comp

- OEMs typically mandate $1 million+ combined single limits—far exceeding state minimums

- Average new vehicle values now exceed $48,000, making inventory protection critical

- Bundling coverages and implementing risk controls significantly reduce premiums

- Specialty brokers understand OEM requirements better than generalist agents

What Is Auto Franchise Dealership Insurance?

Franchise dealership insurance is a package of commercial coverages designed specifically for OEM-authorized new-car dealers—those operating under manufacturer agreements with brands like Ford, Toyota, General Motors, or Honda. This insurance differs from independent or used-car dealer coverage because of operational scale, manufacturer requirements, and risk complexity.

The Franchise vs. Independent Distinction

The core difference is contractual. Franchise dealers have formal agreements with manufacturers that require them to:

- Operate under brand standards and maintain OEM-specified facilities

- Carry substantial new vehicle inventory alongside certified pre-owned programs

- Run full-service departments with staffed technicians and active test drive programs

- Maintain floorplan financing lines worth millions of dollars

Independent dealers, by contrast, typically sell used vehicles without OEM authorization, operate smaller lots, and carry no manufacturer obligations.

That operational gap has direct insurance consequences. OEMs often mandate minimum coverage levels as part of dealer agreements—Toyota, for example, requires partners to carry at least $1,000,000 combined single limit (CSL) for commercial general and automobile liability. A franchise dealer's risk profile—higher inventory values, larger service departments, more employees, and millions in floorplan financing—is simply not comparable to a small independent lot running on state minimums.

Core Coverage Types Every Franchise Dealership Needs

Garage Liability Insurance

Garage liability insurance forms the foundational coverage for franchise dealerships. This policy covers bodily injury and property damage arising from day-to-day operations: accidents in service lanes, customer slip-and-falls in showrooms, damage caused by employees while moving vehicles, and liability from test drives.

Franchise dealers must carry far higher liability limits than state minimums. While California requires only $15,000 per person and Texas mandates just $85,000 CSL, OEMs and floorplan lenders typically require $1,000,000 CSL as the industry benchmark. Operating below these thresholds places dealers in breach of contract and exposes dealership assets to catastrophic lawsuits.

Dealer's Open Lot (DOL) Coverage

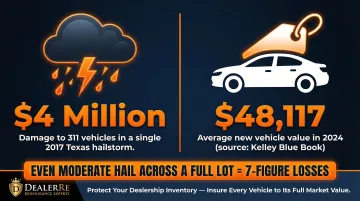

DOL coverage protects physical inventory on your lot from non-collision damage, including hail, fire, flood, theft, and vandalism. For franchise dealers carrying millions in new vehicle inventory, this is often the most expensive yet critical coverage you'll carry.

The financial risk of uninsured inventory loss is staggering. A 2017 hailstorm in Plano, Texas inflicted $4 million in damage to 311 vehicles at a single Subaru dealership. With average new vehicle values reaching $48,117 in late 2024, even moderate storm damage across your lot can produce seven-figure losses.

Critical consideration: Ensure your lot is "insured to value"—meaning your policy limit matches the actual maximum inventory value. Underreporting to save premiums triggers coinsurance penalties that drastically reduce claim payouts when you need coverage most.

Garage Keepers Insurance

Garage keepers insurance covers damage to customer vehicles while in your dealership's care, custody, or control. For franchise dealers with service departments handling hundreds of customer vehicles monthly, a single disputed repair bill can escalate into a costly liability claim without it.

Understanding coverage types:

| Coverage Type | How It Responds | Customer Impact |

|---|---|---|

| Legal Liability | Pays only if dealership is legally negligent | Customer must file on personal insurance for non-negligence events like hail or theft |

| Direct Primary | Pays regardless of fault or liability | Dealership policy covers all damage, protecting customer relationships |

Franchise dealers with high service volume should strongly consider direct primary coverage. While premiums run higher, this structure prevents the severe reputational damage of forcing loyal service customers to file claims on their personal policies for damage occurring on your property.

Dealer Plate & Test Drive Insurance

Dealer plate insurance covers vehicles, drivers, and third parties during test drives and dealer-to-dealer transport. Franchise dealers conducting dozens of test drives weekly need adequate limits: a single at-fault test drive accident resulting in serious injury can produce a $500,000+ liability claim, well above minimum coverage levels.

Errors & Omissions (E&O) Insurance

E&O insurance protects franchise dealers from lawsuits stemming from mistakes in paperwork, financing documentation, vehicle history disclosures, or F&I product sales. High transaction volume creates frequent exposure. Regulatory scrutiny around consumer financial protection means even minor documentation errors can trigger CFPB complaints or class-action suits.

Workers' Compensation Insurance

Franchise dealerships employ large workforces spanning sales, service, detail, parts, and administrative roles. State law generally requires workers' comp coverage, and premium calculations vary widely by department risk profile. Service technicians working with heavy equipment face higher injury risks than desk staff, affecting classification codes and costs.

Franchise-Specific Insurance Considerations

OEM Contractual Insurance Mandates

OEM dealer agreements mandate specific minimum insurance coverages and limits as conditions of franchise authorization. Falling short places you in breach of contract and jeopardizes your franchise relationship.

Review your manufacturer agreements annually to stay compliant:

- Confirm all policy limits meet or exceed OEM thresholds

- Update coverage when adding new franchises or locations

- Document compliance for each active manufacturer agreement

Additional Critical Coverages

Employment Practices Liability Insurance (EPLI) protects against claims of discrimination, harassment, and wrongful termination. For dealerships with 51-250 employees, industry benchmarks recommend at least $3 million in EPLI limits. Given larger staff sizes, franchise dealers face significantly higher exposure than small independent operations.

Cyber Liability Insurance has become essential for franchise dealers. The June 2024 CDK Global ransomware attack crippled approximately 15,000 North American dealerships, halting sales, financing, and service operations for days. The FTC Safeguards Rule now requires dealers to notify the FTC within 30 days of discovering breaches involving 500+ consumers' unencrypted information.

Franchise dealers collect massive volumes of customer financial and personal data through DMS systems and digital financing platforms — making cyber coverage a compliance requirement, not just a precaution.

The F&I Insurance Dimension

Franchise dealers generate substantial revenue selling F&I products — vehicle service contracts, GAP insurance, and ancillary protection packages. Traditionally, profits from these products flow to third-party administrators and insurers, not the dealership.

Forward-thinking franchise dealers are exploring dealer-owned reinsurance structures that allow them to capture underwriting profits internally rather than passing them to outside companies. DealerRE specializes in helping franchise dealers establish their own reinsurance companies to retain F&I profits while maintaining control over the customer experience. Contact DealerRE to find out how much your dealership is currently leaving on the table — and what a reinsurance structure could return to your bottom line.

What Affects the Cost of Franchise Dealership Insurance?

Primary Cost Drivers

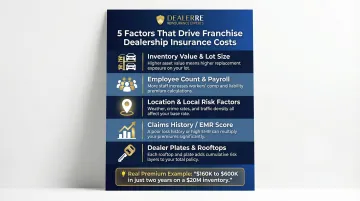

Five variables account for the bulk of what franchise dealers pay:

- Inventory value and lot size — Higher vehicle counts drive up DOL premiums, particularly in hail-prone regions. One Denver Cadillac dealership saw DOL premiums jump from $160,000 to nearly $600,000 over two years on $20 million in inventory.

- Employee count and payroll — Workers' comp is calculated by payroll classification codes. Service technicians carry higher risk ratings than sales staff, so shops with large service departments pay more per payroll dollar.

- Location and local risk factors — Hail belt exposure (Texas, Colorado, the Great Plains) raises DOL costs. Local crime rates affect theft coverage, and state regulatory environments shape overall pricing.

- Claims history — Your Experience Modification Rate (EMR) compares your loss history to industry averages. Scores below 1.0 reduce premiums; scores above 1.0 increase them.

- Dealer plates and rooftops — Each additional plate or location expands liability exposure across multiple coverage lines.

The Bundling Advantage

Franchise dealers packaging multiple coverages—garage liability, DOL, garage keepers, E&O, and workers' comp—with a single carrier or specialty program typically receive better rates and less administrative overhead. While small used lots might pay $15,000 annually, large franchise dealerships with multiple locations can easily pay $100,000+ for comprehensive coverage.

Proactive Risk Management = Cost Savings

Franchise dealers with clean claims histories, robust security systems, and documented employee safety training programs earn lower premiums. Dealerships with enclosed lots, fencing, and theft deterrents generally receive better rates and lower deductibles. Implementing strict safety protocols in service drives to prevent slips, trips, and lifting strains reduces claim frequency—the key factor in lowering your EMR and controlling workers' comp costs.

How to Get the Right Insurance Quote for Your Franchise Dealership

Documentation to Prepare

Before seeking quotes, franchise dealers should gather:

- Current OEM dealer agreement — identifies minimum required coverages and limits

- Inventory value and vehicle count, including average and maximum lot values

- Employee headcount by department for accurate workers' comp classification

- Existing claims history — loss runs for the past 3-5 years

- Service department volume and monthly repair order counts

- Detailed month-end financial statements

Work With Specialty Brokers

Partner with a commercial insurance specialist or broker who has direct experience with franchise auto dealers. Generalist agents frequently miss OEM-specific requirements, under-insure high-value inventory, or fail to structure policies that account for franchise dealer operations.

Specialty programs designed specifically for franchise dealers often offer broader coverage at competitive rates because underwriters understand your unique risk profile. These specialists know to include endorsements like "False Pretense" protection and understand the nuances of OEM indemnity requirements and floorplan lender mandates.

Addressing the F&I Side

Getting the right dealership insurance is one piece of the financial picture. The other is what happens inside your F&I office — specifically, whether you're keeping the underwriting profits from warranties and protection products or sending them to a third-party provider.

For franchise dealers looking to recapture those profits, DealerRE offers a free consultation. Their team helps dealers evaluate reinsurance options and build dealer-owned F&I programs that keep profits in-house while preserving control over customer relationships. Contact DealerRE at (804) 824-9533 to explore whether dealer-owned reinsurance makes sense for your operation.

Frequently Asked Questions

How much is dealer insurance per month?

Cost varies widely by dealership size, location, and coverage package. Small independent lots might pay $1,250 monthly ($15,000 annually), while large franchise dealerships with substantial inventory, multiple locations, and comprehensive coverage programs pay $8,000-$15,000+ monthly. Hail-belt locations face notably higher DOL premiums.

What insurance do dealerships use?

Most dealerships carry a core package: garage liability, dealer's open lot (DOL), garage keepers, dealer plate coverage, errors and omissions (E&O), and workers' compensation. Franchise dealers typically add employment practices liability (EPLI) and cyber liability insurance to address larger staff sizes and customer data exposure.

What is a franchise policy in insurance?

In the dealership context, "franchise policy" refers to insurance programs specifically tailored to OEM-authorized dealerships, often shaped by manufacturer contractual requirements. This differs from the insurance industry's separate use of "franchise" to describe deductible structures where insurers only pay claims exceeding a threshold amount.

What is the difference between a franchise dealership and an independent dealership?

Franchise dealerships operate under manufacturer agreements and sell new vehicles under specific OEM brands, while independent dealers sell used vehicles without manufacturer authorization. This difference changes insurance needs directly: franchise dealers carry higher inventory values, stricter coverage mandates, and greater liability exposure than their independent counterparts.

What is covered in all risk insurance?

"All risk" or "open perils" insurance covers physical damage from any cause not specifically excluded in the policy. For dealerships, this typically applies to DOL (dealer's open lot) coverage, protecting inventory against fire, theft, vandalism, hail, flood, and wind — unlike "named perils" policies that only cover specifically listed events.