Introduction

Most auto dealers are sitting on a substantial untapped profit source they're unknowingly giving away. Every time your F&I office sells an extended warranty, GAP insurance, or tire protection, a significant portion of the profit flows directly to third-party providers.

F&I profit per vehicle retailed (PVR) reached $1,995 in Q4 2025, yet many dealers capture only a fraction of what these products actually generate.

The products aren't the problem. Profit control is. Third-party warranty and insurance companies wouldn't continue doing business with your dealership unless they were making substantial money. That money — underwriting profits, investment income on premium reserves, and claims savings — could stay in your pocket instead.

This guide covers what auto ancillary products are, why they're critical to dealership profitability, which products drive the most revenue, and, critically, how dealers can reclaim the profits they're currently giving away.

What Are Auto Ancillary Products in Car Sales?

Auto ancillary products are optional protection, coverage, and financial products offered alongside the primary vehicle purchase. These products supplement—rather than replace—the core transaction and are typically presented in the F&I (Finance & Insurance) office after the customer has agreed to purchase the vehicle.

The vehicle itself is the primary product; everything else falls into the ancillary category. Extended warranties, insurance add-ons, tire protection, and appearance packages all qualify as ancillary products because they protect or enhance the vehicle purchase rather than constitute the purchase itself.

The Role of Financed Products

"Auto ancillary products on a car loan" specifically refers to add-on protections financed alongside the vehicle loan amount. Rather than paying separately at the time of purchase, customers roll the cost of products like GAP insurance or credit life insurance into their monthly payments. The FTC defines these add-ons as optional products that dealers must disclose are not required and for which dealers must obtain express, informed consent.

Dual Purpose: Customer Protection and Dealer Revenue

Ancillary products serve two distinct functions depending on which side of the deal you're on:

- For customers: Protection against financial risk—unexpected repair bills, loan shortfalls after a total loss, or hardship scenarios that could derail monthly payments

- For dealerships: An additional revenue stream beyond vehicle margin, often the most profitable component of the entire transaction

The F&I office is the primary channel for presenting these products. A well-structured program—trained staff, transparent menus, and competitive offerings—determines how much of that potential revenue a dealership actually captures. Dealers averaging $1,200–$1,800 per copy in F&I typically attribute a significant share to ancillary product sales.

The Most Common Auto Ancillary Products Dealers Offer

Understanding which ancillary products generate the most revenue and serve customers best helps dealers prioritize their F&I strategies. Here are the most widely offered products:

Vehicle Service Contracts (VSCs)

VSCs—often called extended warranties—are the most widely sold and highest-revenue ancillary product per deal. They cover mechanical breakdown costs after the factory warranty expires, with coverage tiers ranging from powertrain-only to comprehensive bumper-to-bumper protection.

VSC penetration reached 45% in Q4 2025, making them the top F&I product by adoption rate. Customers value VSCs because they provide predictable protection against expensive repair bills, while dealers benefit from both the initial sale profit and—for dealers with their own reinsurance companies—the underwriting profits on claims not paid.

GAP Insurance (Guaranteed Asset Protection)

GAP covers the difference between what a customer owes on a financed vehicle and what their auto insurance pays in the event of a total loss or theft. This protection is especially critical for customers who finance with low down payments or on loan terms exceeding 60 months, where depreciation rapidly outpaces loan payoff.

GAP penetration reached 39% in Q4 2025, making it the second most popular F&I product. The GAP Insurance Market is valued at $4.2 billion in 2026, a figure that spans franchise, independent, and BHPH dealerships nationwide.

Tire & Wheel Protection

This product covers repair or replacement of tires and wheels damaged by road hazards such as potholes, nails, or curb damage—costs standard auto insurance typically doesn't cover. Tire and wheel protection ranks among the top five F&I products by penetration and appeals particularly to customers in regions with poor road conditions or harsh winters.

Appearance Protection

Interior and exterior appearance protection packages include paint sealants, fabric protection, ceramic coatings, and leather or vinyl conditioners. These products help preserve resale value and reduce reconditioning costs when the vehicle returns to the dealer as a trade-in. Paint and fabric protection ranks third in penetration among F&I products nationwide.

Credit Life and Credit Disability Insurance

Credit life insurance pays off the loan balance if the borrower dies, while credit disability insurance makes loan payments if the borrower becomes disabled and cannot work. These products are especially relevant in the BHPH and subprime financing space, where customer financial stability is less predictable and lenders need more security against default-related losses.

Additional Ancillary Products

Other common offerings include:

- Roadside assistance – towing, lockout service, and 24/7 emergency support at no out-of-pocket cost

- Key and fob replacement – reimburses the $300–$600 cost of replacing modern electronic keys

- Paintless dent repair (PDR) – removes door dings and minor dents without repainting or voiding warranties

- Theft deterrent and GPS tracking – combines window etching with real-time vehicle location technology

Dealers who structure these products under a reinsurance program—rather than paying third-party providers—retain the underwriting profits on every contract sold, turning each product line into a direct contribution to the dealer's bottom line.

How Auto Ancillary Products Drive Dealership Revenue and Retention

The F&I office consistently ranks as one of the highest-margin departments in any dealership. While front-end vehicle margins have compressed dramatically—falling from $2,926 per vehicle in December 2021 to just $279 per deal by late 2025—F&I has become the foundation of dealership profitability.

The Revenue Multiplier Effect

Every ancillary product sold on a deal adds incremental profit. Dealerships with high ancillary penetration rates (the percentage of customers who purchase at least one product) consistently outperform those with low penetration. F&I PVR rose 14% from January through December 2025, demonstrating that dealers who focus on structured F&I programs are capturing more revenue per transaction.

The compounding effect is substantial: a dealer selling VSCs to 45% of customers, GAP to 39%, and tire protection to 30% will generate far more total F&I revenue than a dealer selling only VSCs to 25% of customers. That spread in penetration rates can represent hundreds of thousands of dollars in annual F&I income.

Customer Retention and Service Loyalty

Ancillary products create long-term relationships that extend far beyond the initial sale. Customers who purchase VSCs or prepaid maintenance plans return to the selling dealer for service and repairs at significantly higher rates than those who don't.

Dealerships using retention plans enjoy an 85% first-year retention rate and 65% in years two and three. This loyalty matters: car owners who get their vehicle serviced at the dealership are 74% more likely to buy their next car from the same place.

Customer Satisfaction and CSI Performance

When ancillary products perform well—a claim gets paid quickly, a tire gets replaced under warranty, GAP covers a total loss—customer satisfaction scores improve dramatically. When overall satisfaction reaches 950 or higher on a 1,000-point scale, 86% of mass market customers and 88% of premium customers say they will "definitely" return for paid service.

For franchise dealers, that CSI performance is directly tied to manufacturer incentives and vehicle allocations—making every smooth claim or fulfilled warranty a measurable business asset.

The Problem with Third-Party Ancillary Product Providers

Most dealers partner with third-party administrators or manufacturer-affiliated providers to offer ancillary products. While this model is easy to set up, it comes with a hidden cost: the dealer earns only a portion of the profit from each sale, typically a fixed reserve or flat fee.

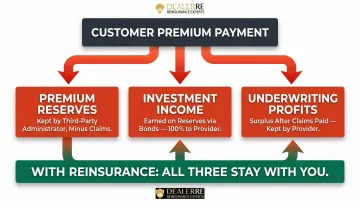

Where Your Money Goes

In a traditional third-party model, premiums are deposited into custodial accounts that hold reserve funds used to cover warranty and service claims. The provider or insurer controls these funds and earns profits from unused reserves after claims are paid out.

Here's what happens to your money:

- Premium reserves – The third-party administrator keeps the bulk of premium dollars collected, minus claims paid and administrative costs

- Investment income – Reserves are invested in conservative government bonds, generating annual income that goes entirely to the third-party provider

- Underwriting profits – Any difference between premiums collected and claims paid represents pure profit that the provider keeps

Your warranty company stays in business because selling products through your dealership is highly profitable for them. That profit comes directly from the spread between premiums collected and claims paid — money that could be building your dealership's balance sheet instead.

The Reinsurance Alternative

Through an admin obligor reinsurance model, dealers replace third-party F&I products with their own reinsurance company — capturing 100% of the profits that external providers were keeping. DealerRE has helped over 400 dealers make this transition across franchise, independent, and BHPH operations.

The real value goes beyond the product sale. Dealers gain investment income on reserves, direct control over the claims process, and a structure that builds long-term personal and business wealth. For BHPH dealers specifically, reinsurance converts problem areas like collateral protection and vehicle warranties into substantial profit centers.

Controlling the claims experience also shapes how customers feel about your dealership long after the sale. When claims are handled quickly and fairly under your roof, customers come back — and they refer others. A third-party provider has no stake in that relationship.

How to Build a More Profitable Auto Ancillary Product Program

Three operational levers consistently separate high-performing F&I departments from average ones: staff training, menu presentation, and metric tracking. Getting all three right compounds quickly.

Train Your F&I Staff Consistently

The presentation matters as much as the product itself. F&I managers who clearly communicate the value and real-world benefits of each product convert at significantly higher rates than those who simply list options.

Structured F&I training—both online and in-person—sharpens presentation skills, improves penetration rates, and ensures compliance with regulations like the FTC's CARS Rule, which requires express informed consent for all add-ons. Dealers who treat training as a recurring investment—not a one-time onboarding step—see measurably stronger penetration rates and fewer compliance gaps over time.

Use a Structured F&I Menu

Present ancillary products through a transparent, organized menu that lets customers see and compare their options. A well-designed menu increases the average number of products purchased per deal and reduces compliance risk by ensuring customers understand what they're buying.

Dealerships using digital F&I menu platforms report an average 33% increase in service contract penetration and over $500 higher PVR. When customers can see their options side-by-side with clear pricing, the conversation shifts from persuasion to selection—which is a far easier position for your F&I manager to be in.

Track Key Performance Metrics

You can't improve what you don't measure. Monitor these critical metrics:

- Penetration rate per product – Percentage of customers purchasing each product

- PVR (Profit Per Vehicle Retailed) – Average F&I gross profit per transaction

- Product-specific claim ratios – Claims paid versus premiums collected for each product

Reviewing these numbers monthly tells you which products are underperforming—and whether the fix is a pricing adjustment, a retraining effort, or removing a product that simply doesn't fit your customer base.

Frequently Asked Questions

What are auto ancillary products?

Auto ancillary products are optional add-on protections and financial products offered alongside the vehicle sale through the dealership's F&I office. Common examples include extended warranties, GAP insurance, and tire protection. They protect the customer's investment while generating additional revenue for the dealer.

What are ancillary products in car sales?

In car sales, ancillary products are presented during the F&I process after the vehicle price is agreed upon. The F&I manager introduces these protections — vehicle service contracts, GAP coverage, appearance packages, credit life insurance — as a menu of options the buyer can add to their deal.

What are ancillary products on a car loan?

Ancillary products on a car loan are add-on protections financed into the loan amount at purchase. GAP insurance covers the shortfall between the loan balance and the vehicle's actual cash value after a total loss. Credit life and disability insurance cover the borrower's loan payments if they die or become disabled.

What are some examples of ancillary products?

The most common examples include Vehicle Service Contracts (extended warranties), GAP insurance, tire and wheel protection, appearance protection packages, credit life and disability insurance, roadside assistance, key replacement programs, and paintless dent repair coverage.

How do auto dealers make money on ancillary products?

Dealers earn profit through the markup between the product cost and the price sold to the customer, plus backend participation structures. Dealers with their own reinsurance companies capture the full premium reserves and investment income that third-party providers would otherwise keep.

What is the difference between a vehicle service contract and other ancillary products?

A VSC specifically covers mechanical breakdown and repair costs. Other ancillary products address different risks: GAP covers the financial shortfall after a total loss, tire and wheel covers road hazard damage, and credit life/disability covers loan payments if the borrower faces hardship. Together, they address the full range of risks a buyer may encounter.