Introduction

After years of volatile vehicle margins and compressed profitability, dealers across all segments are taking a hard look at F&I programs that have been running on autopilot for far too long. Reinsurance and profit participation structures — once treated as passive revenue — are now front and center.

The question dealers are asking isn't whether to participate in these programs. It's how much underwriting profit has been flowing to third-party providers instead of back into the dealership, and what it takes to stop that.

This article covers what's driving that shift — why experts are urging dealers to revisit their programs now, what active management looks like in 2025, and where reinsurance is headed as repair costs climb and regulatory pressure builds. Whether you run a franchise store, an independent lot, or a BHPH operation, there's real money on the table worth understanding.

TLDR

- Dealers are being warned against "set it and forget it" reinsurance management—annual reviews and quarterly check-ins are now the industry standard

- Target loss ratios sit at 70%, but new IRS thresholds (30% for listed transactions, 60% for transactions of interest) are raising the compliance bar

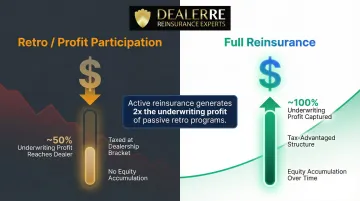

- Active reinsurance structures capture twice the underwriting profit of passive retro programs

- Ancillary F&I products like tire and wheel protection offer stronger retention and lower loss ratios than traditional VSC or GAP products

- Independent and BHPH dealers can build customer-funded reinsurance programs that protect inventory and generate long-term wealth

Profit Participation Programs Are Under a Microscope

Many dealers are running profit participation programs they haven't thoroughly reviewed in years — and some are operating at dangerously high loss ratios without realizing it. According to a Protective Asset Protection survey, more than half of dealer groups currently participate in a Non-Controlled Foreign Corporation (NCFC), yet only 11% of dealer group executives are even aware that new tax law could adversely affect NCFCs.

What a high loss ratio signals:

- Labor rates and claim severity may be out of alignment with pricing

- Reserve positioning may be inadequate to cover future obligations

- Standard operating procedures may need recalibration to match current market conditions

- Someone else is capturing money that should be building dealer wealth

Industry benchmarks and IRS thresholds:

Industry benchmarks often target a loss ratio around 70%, though that figure varies by franchise brand, geographic region, and product mix. However, the IRS's January 2025 final regulations (T.D. 10029) established strict Loss Ratio Factor thresholds for 831(b) micro-captives: 30% for listed transactions and 60% for transactions of interest. The IRS noted that NAIC industry averages ranged between 67.2% and 76.2% per year from 2012 to 2021. Most standard dealer admin-obligor setups are protected under a "Consumer Coverage Exception," but the heightened scrutiny means dealers can no longer afford to ignore their loss performance.

Recommended review cadence:

Industry voices are calling for at minimum one comprehensive annual review, supplemented by quarterly operational check-ins. This mirrors the kind of oversight dealers would apply to a retirement investment portfolio — reinsurance programs represent long-term wealth accumulation, not just transactional income. Dealers who don't actively monitor their programs lose clarity on how funds are actually performing.

Without that visibility, managing budgets, claim severity, and investment returns becomes guesswork.

The opportunity cost of passive participation:

Even dealers who don't own a reinsurance company should participate in profit sharing with their warranty provider at minimum. That said, the review process often reveals just how much passive participation costs over time. Because a retro is taxed at the dealership's tax bracket level and starts with roughly 50% fewer dollars, it's far less advantageous than full reinsurance participation. A retro check represents half of the underwriting profit that could have been generated using reinsurance — meaning dealers are leaving substantial money on the table by staying passive.

Back-End Wealth Building Is Gaining Serious Traction in F&I Conversations

While new and used vehicle profitability has been volatile, F&I profits have continued to climb. In Q4 2024, publicly owned auto dealerships reported an average F&I gross profit of $2,501 per vehicle, the highest level recorded since Q3 2023. This represents a 1.1% increase over Q4 2023 and brings F&I PVR within just 3.9% of the all-time high of $2,603 seen in Q3 2022.

That momentum is prompting a broader strategic shift. Forward-thinking dealers in 2025 are increasingly focused on wealth-building through profit participation programs. Whether through a Dealer Owned Warranty Company (DOWC) or other reinsurance structures, these programs allow dealers to capture a greater share of the underwriting profit and investment income generated by the products they sell. Reinsurance is being repositioned not just as an F&I add-on, but as a foundational wealth-building tool—similar to how a dealer might approach tax strategy or succession planning.

Where Dealers Are Deploying Reinsurance Profits

- Business acquisitions and expansion into new markets

- Facility upgrades and modernization projects

- Employee retention bonuses and staff development programs

- Retirement planning and personal wealth accumulation

- Real estate investment opportunities

- Charitable giving and community investment

The Volume Threshold Most Dealers Can Hit

The common benchmark many advisors reference is 20–25 vehicle service contracts (VSCs) per month. At this volume, dealerships consistently produce enough premium dollars to fund a reinsurance company, cover expected claims, and still generate meaningful profit. That equates to roughly $250,000 in annual premium — putting reinsurance within reach for smaller stores that hit consistent VSC volume.

Unlocking the Investment Tier

Once balance sheet cash exceeds 125% of unearned premiums, excess funds can be invested more aggressively — and at the direction of company ownership. That shifts the return profile from conservative government bonds to strategic investment income that compounds over time. Working with a financial advisor who knows the dealer reinsurance space specifically helps dealers identify when that threshold is reached and how to act on it.

Choosing the Right Program Structure: Retro, Reinsurance, and Hybrid Models

Dealers choosing between program structures must align their volume, risk tolerance, and tax planning goals with the appropriate model:

| Structure Type | How It Works | Key Advantages | Key Limitations |

|---|---|---|---|

| Retro Profit-Sharing | Entry-level option requiring no upfront investment; dealers share in underwriting profits based on performance | Very easy to set up with little administrative overhead; provides quick access to profit sharing | Dealers don't build equity, enjoy no meaningful tax benefits, and are entirely dependent on the administrator's performance |

| Controlled Foreign Corporation (CFC) | Dealers establish their own company with significant control over investments and claims handling | Qualifies for IRS 831(b) election, which excludes up to $2.8M annually in premiums from taxable income | The IRS cap limits scalability; dealers writing higher volumes may eventually outgrow this structure |

| Dealer-Owned Warranty Company (DOWC) | Maximum flexibility and ownership but requires significant compliance and accounting resources | Dealers capture 100% of underwriting and investment income; product design flexibility is particularly valuable for large dealer groups managing diverse product lines | Significant regulatory and administrative complexity; dealers need strong partners or internal infrastructure |

Why the 831(b) Election Matters

CFCs qualify for the IRS 831(b) election, which allows property and casualty insurance companies with less than $2.8M in annual net premiums to be taxed only on investment income rather than all premium income. This creates tax-advantaged wealth accumulation for dealers who are risk-tolerant and actively engaged in program management.

The 2025 IRS regulations also provide a "Consumer Coverage Exception" that exempts "Seller's Captives" from being classified as listed transactions — protecting most standard dealer admin-obligor models from additional scrutiny.

The Real Cost of Staying Put

A common misconception is that switching providers causes major operational disruption. In practice, transitions are straightforward and administrative when handled by an experienced partner. DealerRE manages the full process — training, claims adjudication, compliance, reporting, and financials — with no hidden fees.

Staying in a poorly performing structure out of fear of change is often the more costly decision.

Ancillary F&I Products: The Underutilized Reinsurance Opportunity

Most dealers focus their reinsurance program almost entirely on vehicle service contracts—but ancillary F&I products represent a significant, underutilized profit opportunity within a reinsurance portfolio.

Why Ancillary Products Drive Higher Surplus

Ancillary products like tire and wheel, paint protection, key replacement, and GAP tend to carry very low loss ratios compared to traditional VSCs. Ancillary products like tire and wheel, paint protection, key replacement, and GAP tend to carry very low loss ratios compared to traditional VSCs. A tire and wheel claim may only pay out $500, but claim frequency is far greater than with GAP. Higher frequency also brings customers back to your service department, creating opportunities to find additional customer pay work.

GAP prices are rising because more vehicles are being totaled by insurance companies. The driver isn't more accidents. It's that repair costs have climbed sharply, pushing total-loss thresholds lower across the board.

Structuring Lifetime Warranties Within Reinsurance

Lifetime warranty products can be structured profitably within a reinsurance program, particularly when paired with data tools that track when vehicles are traded, sold, or totaled before coverage is triggered. For transferable service contracts, the contract holder typically pays a nominal fee around $25 and notifies the issuer. Transfers are not permitted when the vehicle is sold to a dealer, which means premiums can move into surplus when a vehicle exits the customer's ownership.

Portfolio Diversification Strategy

Dealers should view their reinsurance portfolio the same way they'd view an investment portfolio. Relying on VSC volume alone leaves money on the table. A balanced product mix creates multiple profit centers while spreading risk across different claim patterns:

- Vehicle Service Contracts (VSC) — high premium, moderate claim frequency

- Tire & Wheel — low payout per claim, high return frequency

- Door Ding Protection — minimal claims, strong surplus contribution

- GAP — rising prices tied to total-loss trends

- Collateral Protection Insurance (CPI) — steady, predictable claim patterns

What These Trends Mean for Independent and BHPH Dealers

Much of the industry conversation around reinsurance tends to focus on franchise dealers—but independent and Buy Here Pay Here dealers have equally compelling—and often more immediate—reasons to establish their own reinsurance programs.

Independent Dealer Scale Creates Real Opportunity

Independent used vehicle dealers sold 9.8 million vehicles in 2025, nearing 2020 total sales. Furthermore, the deep subprime and subprime risk segments accounted for 34% of all independent dealer originations. With this volume and customer base, independent and BHPH dealers have the scale to use admin-obligor reinsurance for significant tax-advantaged wealth creation.

Converting Repair Costs Into Underwriting Profit

Historically, BHPH dealers used a "50/50 method where you and the customer split the repair bill," which often resulted in the dealer "paying all or most of the bill (once again dipping into gross profit) or enduring a tarnished reputation or increased repossessions." Setting up a Dealer Owned Warranty Company gives dealers the same claims management and accounting benefits as a third-party warranty company.

The customer's vehicle service contract payments are held as reserve in a trust account. Any reserve not used to pay claims becomes profit.

How DealerRE's BHPH Program Is Structured

That model is exactly what DealerRE has built for BHPH dealers.

DealerRE offers admin obligor reinsurance programs specifically built for BHPH dealers to protect their vehicle inventory from mechanical breakdown losses while building a funded program from their customer base. The premiums can be financed over the contract term rather than requiring upfront payment, ensuring cash flow and lending pool are not negatively impacted. This structure turns a traditional cost center—vehicle repairs and mechanical breakdowns—into a profit participation vehicle that accumulates wealth over time.

Full-service administration is included with no hidden fees, covering:

- Training and F&I development

- Claims adjudication and compliance management

- Performance reporting and financials

DealerRE also coordinates with A-rated carriers for fronting arrangements, meaning each dealer's reinsurance company is backed by licensed insurers while the dealer captures the underwriting profit.

Frequently Asked Questions

What is dealer reinsurance and how does it work?

Dealer reinsurance (specifically admin obligor reinsurance) allows a dealer to own a company that reinsures the risk behind F&I products like service contracts and GAP. The dealer's company collects premiums, handles claims through professional administrators, and keeps the profits that would otherwise go to third-party providers—all backed by A-rated insurers.

How much volume does a dealer need to start a reinsurance program?

Program minimums vary by provider, but most programs require around $250,000 in annual premium to get started—roughly 20 to 25 monthly contracts. That threshold makes reinsurance accessible for smaller stores that consistently hit this volume.

What is the difference between reinsurance and a retro/profit participation program?

A retro or profit sharing program returns a portion of profits from a third-party provider based on loss performance. Dealer reinsurance means the dealer owns the risk-bearing entity and captures the full upside—with greater control, meaningful tax benefits through 831(b) elections, and typically greater long-term wealth-building potential.

How often should dealers review their reinsurance program?

At minimum, conduct an annual comprehensive review of loss ratios, reserve positioning, and claims trends. More complex programs benefit from quarterly operational check-ins. Treat your reinsurance program like any serious financial asset—with active oversight, not passive neglect.

Can Buy Here Pay Here and independent dealers benefit from reinsurance?

Yes. BHPH and independent dealers are well-suited for admin obligor reinsurance structures that protect against mechanical breakdown losses and fund reserve accounts directly from their own customer base. Independent dealers represent a large and growing segment—making the opportunity for dealer-owned reinsurance programs significant.

What are the tax planning advantages of a dealer-owned reinsurance company?

Under IRC 831(b), a dealer-owned reinsurance company can exclude up to $2.8M in annual premiums from taxable income, with tax applying only to investment income. This allows pre-tax premiums to accumulate and grow inside the reinsurance trust—consult a reinsurance specialist and tax advisor to structure the program correctly.