A cedant is the party in any reinsurance arrangement that transfers risk and premium to a reinsurer. Understanding this role isn't just useful for traditional insurers—it's the foundation of one of the most underused profit strategies in automotive F&I. For dealers selling vehicle service contracts and GAP through third-party providers, the cedant structure represents back-end profits they're currently giving away.

This article breaks down what a cedant is, how the ceding process works, which reinsurance types are available, and why the structure matters specifically for auto dealers looking to retain underwriting profits.

TL;DR

- A cedant (also spelled "cedent") transfers a portion of insurance risk and premium to a reinsurer in exchange for loss coverage

- Ceding risk protects solvency, expands underwriting capacity, and stabilizes financial results

- Cedants choose from several structures: facultative, treaty, proportional, non-proportional, and excess-of-loss

- Dealers who set up their own reinsurance company receive those ceded premiums directly, keeping the underwriting profits third-party F&I providers would otherwise pocket

What Is a Reinsurance Cedant?

The cedant is the insurance company or risk-bearing entity that transfers a portion of its insurance risk—and the associated premium—to a reinsurer. This transfer, called "ceding," obligates the reinsurer to cover a defined share of any resulting losses.

The NAIC defines reinsurance as a contract in which "the insurance company—the cedent—transfers risk to the reinsurance company, and the latter assumes all or part of one or more insurance policies issued by the cedent." The RAA Glossary describes the cedent as "the issuer of an insurance contract that contractually obtains an indemnification for all or a designated portion of the risk from one or more reinsurers."

Cedant vs. Cedent: Which Is Correct?

Both are. The table below shows how usage splits across institutions:

| Source | Spelling Used |

|---|---|

| Swiss Re, Artemis.bm | Cedant |

| NAIC, Lloyd's, AM Best, RAA | Cedent |

Continental European usage favors "cedant"; U.S. and London market documents lean toward "cedent." Neither is wrong, and both appear throughout industry literature.

Understanding the terminology is only half the picture. The more pressing question is what drives an insurer to become a cedant in the first place.

Why Insurers Cede Risk

The primary regulatory driver is the NAIC's Risk-Based Capital (RBC) framework, which sets statutory minimum capital levels based on an insurer's size and risk profile. When capital falls below RBC thresholds, regulators can issue corrective orders or take control of the company.

Reinsurance addresses this directly by moving risk off the cedant's books. The NAIC identifies several regulatory purposes for ceding:

- Expanding underwriting capacity without raising new equity

- Stabilizing results against unpredictable loss years

- Providing catastrophe protection

- Withdrawing from a line of business

- Spreading concentrated risk across the market

How the Ceding Process Works

From Policy to Ceded Risk

The flow from policy issuance to ceded risk follows a consistent pattern:

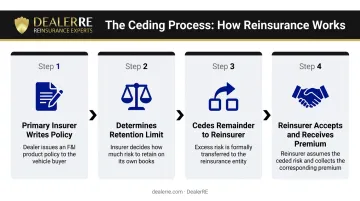

- Primary insurer writes a policy and collects the policyholder's premium

- Determines its retention limit—the maximum loss it will absorb on that policy

- Cedes the remainder to a reinsurer under a pre-agreed contract

- Reinsurer accepts the ceded portion and receives a corresponding share of the premium

Ceding Commissions

Because the cedant incurs acquisition, underwriting, and administrative costs before ceding the risk, the reinsurer typically pays back a ceding commission. The RAA defines this as "an amount deducted from the reinsurance premium to compensate a ceding company for its acquisition and other overhead costs."

The Society of Actuaries documents two common structures:

- Flat commission: A fixed percentage (a property quota share example uses 30%)

- Sliding-scale commission: Adjusts with loss experience—for example, ranging from 25% at a 65% loss ratio to 45% at a 35% loss ratio

These are illustrative examples, not market standards. Actual rates vary by line of business and treaty terms.

Funds Held and Loss Settlements

When a claim occurs, the cedant typically pays the policyholder first, then seeks reimbursement from the reinsurer for the ceded share. Under a funds held arrangement (common in quota share treaties), the cedant retains the ceded premium in a trust account rather than transferring it immediately. Losses are netted against that balance periodically, reducing cash transfer volume.

This structure also allows the cedant to earn investment income on funds held, which is particularly relevant for dealer-owned reinsurance programs where reserve management directly affects profitability.

Ongoing Reporting Obligations

Beyond managing funds, cedants carry ongoing reporting obligations throughout the contract. On a recurring basis, the cedant submits:

- Premium volume and loss activity via periodic bordereaux and premium/loss summaries

- Exposure data to keep the reinsurer current on covered risk

- Claims files and books, which reinsurance contracts typically make accessible under an access-to-records clause

Accurate reporting is non-negotiable. When it lapses, claims reimbursement stalls and the reinsurance relationship deteriorates.

Types of Reinsurance Available to Cedants

Proportional vs. Non-Proportional Reinsurance

The broadest distinction in reinsurance structure is whether the reinsurer shares in both premiums and losses from the start, or only steps in when losses exceed a threshold.

Proportional reinsurance splits premiums and losses at a fixed ratio:

- Quota share cedes the same fixed percentage of every policy — premiums and losses both transfer at that ratio. According to Swiss Re's Essential Guide to Reinsurance, this structure is "ideal for homogenous portfolios" like motor insurance and works well for growing insurers seeking capital relief.

- Surplus share lets the cedant retain risks up to a defined limit and cede only the excess. This gives more precise calibration than quota share when policy sizes vary significantly.

Non-proportional reinsurance has no fixed premium split. The reinsurer only pays when the cedant's losses exceed a specified threshold:

- Protects against severe or catastrophic loss events, not routine claims activity

- The cedant absorbs all losses below the retention point

- The reinsurer covers everything above that threshold

- Premium is paid directly to the reinsurer rather than split proportionally

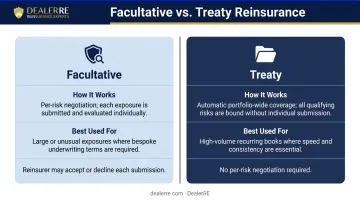

Facultative vs. Treaty Reinsurance

The second key distinction is whether coverage is negotiated per risk or applies automatically to a portfolio:

| Structure | How It Works | Best Used For |

|---|---|---|

| Facultative | Each risk submitted individually; reinsurer can accept or decline | Large, unusual, or high-value exposures outside treaty limits |

| Treaty | Standing agreement covers an entire class or portfolio automatically | High-volume, recurring books of similar business |

Of the non-proportional structures covered by treaty or facultative arrangements, Excess-of-Loss is the one cedants encounter most frequently.

Excess-of-Loss (XOL)

XOL reinsurance covers losses above the cedant's retention on a per-occurrence or aggregate basis. The cedant pays a standalone reinsurance premium directly — no ceding commission applies.

XOL is typically used to:

- Cap exposure from a single catastrophic event

- Limit cumulative annual losses that could exceed the cedant's tolerance

- Provide a clean, defined ceiling on the cedant's worst-case liability

Key Benefits of the Cedant Role

Solvency Protection

The most direct benefit: ceding risk limits the cedant's financial exposure to any single loss or series of losses. This protects the solvency margin and ensures the insurer can meet policyholder obligations even in adverse years.

Swiss Re confirms that reinsurance "stabilises insurance company results" by "absorbing some of their losses"—and the NAIC lists solvency stability as a core regulatory purpose of the cedant relationship.

The global reinsurance market currently offers favorable conditions for cedants. S&P Global reported that global reinsurance capital hit a record $760 billion as of September 30, 2025, with 10%-20% rate declines at January 2026 renewals—a buyer-favorable environment for those seeking protection.

Expanded Underwriting Capacity

Because reinsured risks no longer count against the cedant's RBC requirements, the cedant can write more business and offer higher policy limits than its balance sheet alone would support. Swiss Re describes this as "capital relief"—the cedant effectively uses the reinsurer's capital to grow without raising additional equity.

For dealers operating their own reinsurance structure, this matters directly: capacity that would otherwise sit idle on the balance sheet can instead back additional vehicle service contracts, GAP, or ancillary products—turning reserved capital into active revenue.

Financial Predictability

Reinsurance smooths out the peaks and valleys in financial results. Dealers writing vehicle service contracts or mechanical breakdown coverage know how sharply claims can spike in any given period—this stabilization directly addresses that exposure.

Predictable financials make planning easier, support better financing terms, and present a stronger picture to outside investors or buyers.

How Auto Dealers Can Leverage the Cedant Structure

The Status Quo Problem

When a dealer sells F&I products through a third-party provider, here's what actually happens financially:

- The dealer earns a front-end markup or commission at point of sale

- The fronting insurer collects all premiums and holds them in reserve

- Claims are paid from those reserves

- Whatever remains—the underwriting profit—stays with the third-party provider

The dealer's loss experience directly determines how profitable that relationship is for the provider. As DealerRE puts it plainly: if your third-party warranty provider weren't making a profit off you, why would they continue doing business with you?

The Dealer-Owned Reinsurance Opportunity

Through an admin obligor reinsurance structure, a dealer establishes their own reinsurance company that receives premiums ceded from the fronting insurer. The dealer's company sits in the risk-assuming position: it captures ceded premiums, holds reserves in a U.S.-based trust, and retains underwriting profits after claims are paid.

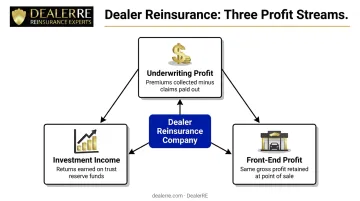

The profit streams this creates:

- Underwriting profit: Premiums collected minus claims paid

- Investment income: Returns earned on reserves held in trust (initially in conservative government bonds; dealers can invest excess reserves above 125% of unearned premiums more aggressively, at their direction)

- Same front-end profit: Dealers still earn the same gross profit at point of sale they earned before

This structure works across the full F&I product portfolio—vehicle service contracts, GAP, collateral protection insurance, debt cancellation coverage, tire and wheel, and ancillary products.

DealerRE's Role

DealerRE has helped over 400 dealers nationwide build these programs since 1994, managing everything from company formation to ongoing administration. Services include:

- Legal forms, compliance filings, and annual renewals

- Tax returns and monthly financial statements

- Claims adjudication through their partner administrator

Dealers get complete visibility into their reinsurance company's performance without having to manage the operational complexity themselves. For BHPH dealers specifically, the structure accommodates monthly premium billing tied to customer payment cycles—preserving cash flow while still capturing full underwriting profit at contract earn-out.

The scale of what's at stake makes the math compelling. Assurant's Global Automotive segment alone generated $3.11 billion in vehicle service contract revenue in just the first nine months of 2024. Dealer-owned reinsurance puts a share of that pool back where it belongs—on the dealer's balance sheet.

Frequently Asked Questions

What is ceding and cedant?

Ceding is the act of transferring a portion of insurance risk and the associated premium to a reinsurer. A cedant is the insurance company or risk-bearing entity that performs this transfer—it "gives away" a share of risk in exchange for financial protection against large or unexpected losses.

What is the difference between cedant and cedent?

Both terms describe the same role: the party that transfers risk in a reinsurance agreement. "Cedant" is the preferred international term; "cedent" appears more often in U.S. documents. Either is acceptable and both are used interchangeably throughout industry literature.

What is the difference between a cedant and a reinsurer?

The cedant is the primary insurer transferring risk; the reinsurer is the entity accepting that risk in exchange for a premium. The cedant maintains the policyholder relationship, while the reinsurer operates behind the scenes, stepping in to cover its agreed share when losses occur.

How does a cedant benefit financially from reinsurance?

The core financial benefits include solvency protection, expanded capacity to write more business without raising equity, and stabilized results across reporting periods. Cedants also receive a ceding commission that partially offsets acquisition and administrative costs.

What types of reinsurance can a cedant choose from?

The main options are:

- Facultative — per-risk negotiation for individual policies

- Treaty — portfolio-wide automatic coverage

- Proportional — shared premiums and losses via quota share or surplus share

- Non-proportional — coverage triggered above a defined loss threshold

- Excess-of-loss — coverage above a set retention limit

Can auto dealers participate in reinsurance as a cedant?

Through a dealer-owned admin obligor reinsurance structure, dealers position their own reinsurance company to receive premiums ceded by the fronting insurer. This puts the dealer in the profit-capturing role, retaining underwriting income and investment returns from F&I programs instead of sending those profits to a third-party provider.