Introduction

Every month, dealers across the country sell dozens of vehicle service contracts, GAP policies, and ancillary F&I products — then watch third-party providers keep the underwriting profits. The dealer earns a flat commission while the administrator retains what's left after claims.

The mechanism behind this profit drain has a name: cession. Specifically, it's the absence of a cession structure designed to work in the dealer's favor.

According to Investopedia, the U.S. property and casualty industry ceded nearly $1 trillion in premiums in 2024 alone. Behind every dollar is a cession decision: who transfers risk, how much, and to whom. Dealers who understand cession stop leaving underwriting profits on the table and start building programs designed to capture them.

This article covers the core concepts dealers need:

- What cession is and how it works mechanically

- The difference between proportional and non-proportional structures

- How cession limits are set and why they matter

- What this means for dealers considering a reinsurance program

TLDR

- Cession transfers insurance risk and a share of premiums from a ceding company to a reinsurer

- Proportional cession splits premiums and losses by a fixed percentage from dollar one

- Non-proportional cession only activates when losses exceed a set threshold — no loss, no payout

- Cession limits cap how much exposure a reinsurer accepts under a given agreement

- Cession ratio = ceded premiums ÷ gross written premiums , which measures how much risk (and profit) flows outward

- For auto dealers, controlling cession is how underwriting profits get redirected from third-party providers into a dealer-owned reinsurance company

What Is Cession in Reinsurance?

Cession carries a dual meaning. The Reinsurance Association of America defines it as both "the portion of insurance ceded by the ceding company to the reinsurer" (the unit of risk transferred) and the formal act of making that transfer. Both definitions apply simultaneously in any reinsurance transaction.

The Three Core Parties

Every cession transaction involves:

- The original insured — a vehicle buyer purchasing a service contract or GAP policy

- The ceding company — the primary insurer or dealer-administered program that underwrote the policy

- The reinsurer — the entity accepting transferred risk in exchange for a share of premiums

One critical point: the ceding company never escapes its obligation to the policyholder. Cession redistributes financial risk between the ceding company and the reinsurer — it doesn't remove the ceding company's liability to the person who bought the policy.

Cession vs. Retention

What a company cedes goes to the reinsurer. What it retains stays on its own books. This isn't just accounting terminology — it's the central strategic decision in any reinsurance program design.

The cession ratio (also called the cession rate) measures how much risk flows outward:

Cession Ratio = Ceded Premiums ÷ Gross Written Premiums

A high cession ratio means more protection but less retained premium income. A lower ratio means the ceding company keeps more of the economics but carries more exposure. The right ratio depends on the dealer's capital reserves, claims history, and how much volatility the program can absorb in a given year.

Why Cession Exists

No insurer or dealer F&I program can absorb unlimited losses from its own capital. Cession solves that constraint. By transferring a defined portion of risk to a reinsurer, the ceding company can write more policies and offer broader coverage terms. Financial stability across a large book of business becomes far more manageable when no single bad year can threaten the entire program.

For dealer-owned reinsurance programs specifically, cession enables:

- Writing higher policy volumes without proportionally increasing capital exposure

- Stabilizing claims costs across years with heavier-than-expected losses

- Maintaining coverage commitments to customers regardless of short-term loss activity

How Cession Works: The Step-by-Step Mechanics

Cession is a proactive structural decision, not a reaction to a claim. Before any loss occurs, the ceding company has already determined its retention level and formalized what gets transferred under a reinsurance contract.

Premium Flow

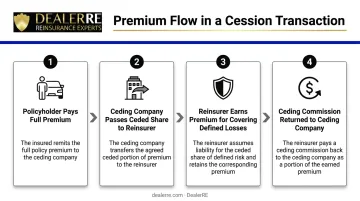

When a policy is written and a cession is made:

- The ceding company collects the full premium from the policyholder

- It passes the agreed ceded share to the reinsurer

- The reinsurer earns that premium in exchange for covering its defined portion of future losses

- The ceding company may receive a ceding commission — a payment from the reinsurer that offsets acquisition costs and administrative overhead

Loss Flow

When a covered claim occurs:

- The ceding company pays the policyholder first

- It then recovers its agreed share from the reinsurer per the reinsurance contract terms

- The contract language specifies exactly when and how the reinsurer's obligation triggers — including trigger conditions, timing of recovery, and loss thresholds

Facultative vs. Treaty Reinsurance

Two contract types govern how cession is structured:

| Type | How It Works | Best Fit |

|---|---|---|

| Facultative | Negotiated policy-by-policy; each cession individually agreed upon | Unusual, high-value, or one-off risks |

| Treaty | Blanket agreement covering an entire class of business; cession is automatic within defined parameters | High-volume, homogeneous programs |

For dealer F&I programs — VSCs, GAP, ancillary coverage — that distinction matters immediately. Treaty reinsurance is the standard because it handles cession automatically across an entire class of business. When a dealer's program produces hundreds of contracts monthly, negotiating each cession individually isn't feasible. The treaty covers them all within its defined parameters without manual intervention.

Retrocession: The Downstream Extension

A reinsurer can itself cede portions of accepted risk to another reinsurer — called a retrocessionaire. This retrocession uses identical mechanics. The same premium-sharing and loss-recovery logic applies, just one layer further down the chain. Cession, in other words, is a layered system — risk can pass through multiple entities before the chain ends.

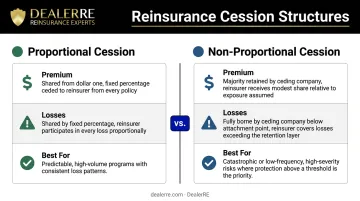

Types of Cession: Proportional vs. Non-Proportional

The structure of a cession determines how premiums and losses are divided. The two main categories — proportional and non-proportional — differ in when the reinsurer gets involved and how much premium they receive in exchange.

Proportional Cession

The reinsurer and ceding company share both premiums and losses at a fixed percentage from the first dollar of loss. Two main forms:

- Quota share — a flat percentage applied to all policies in a class. If a program runs on 60% quota share, 60% of every premium and 60% of every loss goes to the reinsurer.

- Surplus share — the ceded amount is determined by what exceeds the ceding company's retention limit. Larger risks cede more; smaller risks may be retained entirely.

Proportional cession is common in high-volume programs like VSC and GAP coverage, where stable claim frequency makes percentage-sharing practical for both parties.

Non-Proportional Cession

The reinsurer only steps in when losses exceed a defined threshold — the attachment point. Below that threshold, the ceding company absorbs losses entirely. Above it, the reinsurer pays up to a specified limit.

The reinsurer doesn't receive a proportional share of premiums. Instead, it charges a separate reinsurance premium for agreeing to cover losses in that upper band. Excess-of-loss reinsurance is the primary example of this structure.

Non-proportional cession protects against catastrophic or infrequent large losses, not routine claims activity. In dealer-owned warranty programs (DOWCs), excess-of-loss coverage is often layered on top of the primary structure specifically to cap tail-risk exposure.

Profit Implications

| Structure | Premium Retained | Loss Sharing | When to Use |

|---|---|---|---|

| Proportional | Shared with reinsurer | Shared with reinsurer from dollar one | Predictable, high-volume programs |

| Non-proportional | Retained (mostly) | Fully on ceding company below attachment point | Catastrophic or low-frequency risks |

Proportional cession trades premium income for shared loss exposure. Non-proportional keeps more premium in-house but requires the ceding company to absorb every dollar of loss below the attachment point — a meaningful distinction when sizing retention limits.

Cession Limits: How Much Risk Can Be Transferred?

A cession limit is the maximum liability a reinsurer agrees to accept under a specific reinsurance agreement. It functions as a ceiling on the reinsurer's financial exposure — per risk, per occurrence, or in aggregate over a policy period.

How Limits and Retention Interact

The structure works like a defined band of coverage:

- Retention = the floor (what the ceding company keeps)

- Cession limit = the ceiling (how far above the floor the reinsurer will reach)

- Losses above the cession limit fall back on the ceding company or a higher-layer program

Example: A ceding company retains the first $50,000 of any loss. The cession limit is $200,000. Losses between $50,001 and $250,000 are covered by the reinsurer. Losses above $250,000 revert to the ceding company unless a second layer of reinsurance is in place.

Why Limits Matter for Program Design

Setting limits requires balance:

- Too low → the ceding company absorbs large losses the reinsurer won't cover

- Too high → reinsurance premium costs climb unnecessarily

The right cession limit depends on expected loss severity and frequency for the specific product portfolio. In practice, each product line carries its own retention and cession limit schedule — calibrated to that line's claims history and exposure profile — which is why dealers managing multiple F&I products benefit from reviewing limits per product rather than applying a single program-wide figure.

Real-World Cession Examples

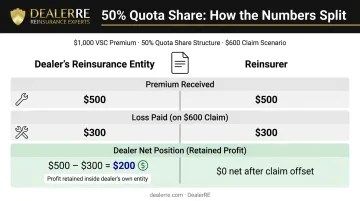

Auto Dealer F&I Example

A dealer sells a vehicle service contract for a $1,000 premium under a 50% quota share arrangement:

- Premium split: Dealer's reinsurance company receives $500; reinsurer receives $500

- Claim occurs: The repair costs $600

- Loss split: Dealer's entity pays $300; reinsurer pays $300

- Net position (dealer's entity): $500 premium collected − $300 loss paid = $200 retained

This is cession working as designed. The dealer's entity accepted half the risk, collected half the premium, and covered half the claim. The underwriting profit — the difference between premium earned and losses paid — stays within the dealer's program rather than flowing to a third-party administrator.

Cession at Scale: Nuclear Insurance Pools

American Nuclear Insurers (ANI) comprises roughly 21–22 member companies that pool capacity to cover nuclear risks no single insurer could absorb alone. Domestically, the pool retains a defined share and cedes portions to approximately 26+ international nuclear insurance pools through reciprocal reinsurance agreements.

The dollar amounts differ dramatically from a dealer F&I program, but the mechanics are identical. In both cases, cession solves the same problem: no single entity can absorb the full range of potential losses from its own capital, so risk is distributed across multiple parties in exchange for a share of the premium.

What the Examples Reveal

Cession is always a trade-off between risk transfer and profit retention:

- Cede more risk → pay more in reinsurance premiums → surrender more underwriting gain

- Retain more risk → keep more premium economics → need capital to absorb losses

- The optimal structure depends on volume, loss history, and the dealer's long-term financial objectives

Why Cession Matters for Auto Dealer Reinsurance Programs

Most franchise and independent dealers selling F&I products are operating at a 100% cession rate — ceding all underwriting risk and all underwriting profit to third-party providers. They earn a flat commission per contract. The administrator keeps the rest.

F&I gross profit per vehicle retailed reached $2,505 in Q1 2025, approaching historic highs according to Haig Partners. That's a significant revenue line — and in a traditional arrangement, the underwriting profit embedded in those numbers stays with the product provider, not the dealer.

How Dealer-Owned Reinsurance Changes the Equation

When a dealer establishes an admin-obligor reinsurance company, the structure flips:

- The dealer's reinsurance company becomes the company accepting ceded risk and premiums from the fronting insurer

- The dealer sets the retention level and cession structure

- Underwriting profit — the premium left after claims — accumulates inside the dealer's entity

- Investment income earned on reserves also belongs to the dealer's company

In DealerRE's admin-obligor programs, dealers' reinsurance companies are backed by A-rated insurers. Funds are held in a U.S. trust account, with conservative investments initially and the flexibility to invest more aggressively once reserves exceed 125% of unearned premiums.

Dealers in these programs have used earned income to purchase real estate, fund education, and reinvest directly into their operations.

DealerRE has been helping dealers build and manage these programs since 1994, covering cession structure, compliance, claims adjudication, and financial reporting — giving dealers the infrastructure to keep underwriting profits inside their own company rather than passing them to third-party providers.

Frequently Asked Questions

What is a cession in reinsurance?

Cession is the transfer of part of an insurance risk — along with a corresponding share of premiums and liability — from a ceding company (the primary insurer) to a reinsurer, under the terms of a reinsurance contract. The word covers both the act of transferring and the specific portion of risk being moved.

What is the cession limit in reinsurance?

A cession limit is the maximum liability a reinsurer agrees to accept under a reinsurance agreement. It caps how much of any loss the reinsurer will cover above the ceding company's retained amount — anything beyond that ceiling falls back on the ceding company or a higher-layer program.

What is the difference between proportional and non-proportional cession?

Proportional cession splits both premiums and losses by a fixed percentage from the first dollar of loss. Non-proportional cession only triggers when losses exceed a set threshold (the attachment point); the reinsurer takes no proportional share of premiums in return.

What is a cession ratio and how is it calculated?

The cession ratio is ceded premiums divided by gross written premiums. It shows what percentage of total premium income is passing to reinsurers — and how much risk and underwriting profit is flowing out rather than being retained.

What is the difference between cession and retrocession?

Cession is when a primary insurer transfers risk to a reinsurer. Retrocession is when that reinsurer further transfers a portion of its accepted risk to another reinsurer (the retrocessionaire) — the same mechanics, one layer deeper in the chain.

How does cession work in a dealer-owned reinsurance program?

In a dealer-owned admin-obligor program, the dealer's reinsurance company accepts ceded risk and premiums from the fronting insurer. Instead of those premiums flowing to a third-party provider, they accumulate inside the dealer's own entity — capturing the underwriting profit and investment income directly.