That gap matters. Understanding the difference between proportional and non-proportional reinsurance helps dealers evaluate what kind of program they have, ask sharper questions of their administrators, and recognize whether their risk architecture actually fits their claims exposure and growth stage.

This article breaks down non-proportional reinsurance in plain language, explains how it differs from the proportional structures most dealers already use, and clarifies when — and for whom — non-proportional elements become relevant.

TL;DR

- Non-proportional reinsurance only pays out when losses exceed a set retention threshold — below that, the primary insurer absorbs everything

- Also called "excess of loss" reinsurance, it differs from proportional arrangements where premiums and losses are shared from dollar one

- Most dealer-owned programs (admin obligor / quota share) are proportional; non-proportional layers show up as supplemental protection in larger programs

- Understanding the difference helps dealers assess their program structure and how claims exposure is managed at each layer

What Is Non-Proportional Reinsurance?

Non-proportional reinsurance is an arrangement where the reinsurer's obligation to pay only begins once a loss — or accumulation of losses — crosses a defined threshold. Below that threshold, the primary insurer absorbs the entire loss. Above it, the reinsurer steps in up to an agreed maximum.

Munich Re describes it this way: the reinsured pays all losses up to a pre-agreed amount (the priority or deductible), and the reinsurer pays the balance above that amount up to a pre-agreed limit. In this structure, the reinsurer and the primary insurer do not share risk proportionally — they share the loss on an excess-of-loss basis only, triggered by the attachment point.

How It Differs from Proportional Reinsurance

The contrast with proportional reinsurance is straightforward:

- Proportional: Premiums and losses are divided at an agreed ratio from the first dollar of loss. The reinsurer participates in routine claims and routine profits.

- Non-proportional: The reinsurer collects a separately negotiated premium and pays nothing on routine claims. Their obligation is triggered solely by losses above the attachment point.

That distinction matters for dealer programs: proportional structures share every dollar of claim activity, while non-proportional structures exist specifically to limit catastrophic or cumulative loss exposure.

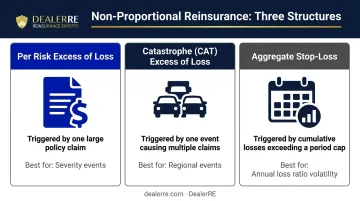

Three Types Relevant to Dealer Programs

| Type | What Triggers It | Best For |

|---|---|---|

| Per Risk Excess of Loss | A single large claim on one policy | Severity events on individual contracts |

| Catastrophe (CAT) Excess of Loss | One event causing multiple claims simultaneously | Multi-vehicle incidents or regional events |

| Aggregate (Stop-Loss) Excess of Loss | Total claims over a period exceed a cumulative cap | Annual loss ratio volatility |

Each type addresses a different form of exposure. For most dealer-owned programs, aggregate stop-loss is the most operationally relevant: it caps total annual losses rather than individual claim severity, giving dealers a predictable ceiling on what a bad claims year can actually cost them.

How Non-Proportional Reinsurance Works

The mechanics rest on two numbers: the retention (the maximum loss the primary insurer absorbs before the reinsurer engages) and the limit (the maximum the reinsurer will pay above the retention). Everything below the retention is the dealer's responsibility. Everything above it, up to the limit, transfers to the reinsurer.

A Dealer-Relevant Example

Say a dealer's reinsurance company has a retention of $50,000 on a VSC program and a single claim reaches $80,000. The dealer's company pays the first $50,000. The reinsurer covers the remaining $30,000 — assuming it falls within the agreed limit layer.

Below $50,000, the reinsurer is uninvolved. No recovery, no participation, no notification required. The dealer absorbs routine losses entirely.

Layering: How Larger Programs Stack Coverage

Bigger programs often divide total protection across consecutive loss layers, each with its own pricing and reinsurer:

- $50,000–$200,000 (Layer 1)

- $200,000–$500,000 (Layer 2)

Different reinsurers may price each layer based on their own risk appetite. Layers that are less likely to be reached (higher attachment points) typically cost less to purchase. This layering structure is more common in sizable insurance programs, but it explains why complex programs involve multiple reinsurance counterparties.

Premium Pricing

Non-proportional premiums are not a share of the original premium collected. They're independently calculated based on the probability that losses will reach the attachment point. The Casualty Actuarial Society notes that each contract must be individually priced based on the specific needs and risk level of the reinsured.

Factors that influence pricing include:

- Historical claims frequency and severity

- Total premium volume (exposure size)

- Where the attachment point is set relative to expected losses

- The agreed limit above the retention

That pricing complexity directly shapes who handles claims once a program is running — and how much operational control the dealer retains.

Who Manages Claims Day-to-Day

Under a non-proportional structure, claims management below the retention stays entirely with the primary insurer. In the dealer context, that's typically handled by the program administrator on behalf of the dealer's reinsurance company. The reinsurer may have consultation rights on large claims approaching the retention, but they have no involvement in routine claims.

This creates operational independence — but it comes with a trade-off. Dealers must carry sufficient reserves to handle normal claims volume without any reinsurer support.

Proportional vs. Non-Proportional: What Auto Dealers Need to Know

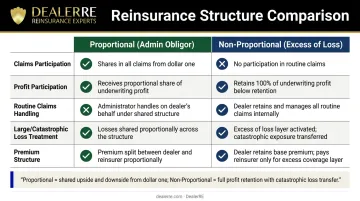

The reason this distinction matters practically: the most common dealer-owned reinsurance structure is proportional. The admin obligor (or quota share) program that DealerRE helps dealers build and manage is proportional in nature — premiums are ceded to the dealer's reinsurance company at an agreed rate, and the dealer participates in underwriting profits when claims are lower than reserves.

The Core Operational Difference

| Proportional (Admin Obligor) | Non-Proportional (Excess of Loss) | |

|---|---|---|

| Claims participation | Shared from the first dollar | Only above the retention threshold |

| Profit participation | Yes — dealer captures underwriting profit on every policy | No — reinsurer only covers tail losses |

| Routine claims | Shared per cession ratio | Fully absorbed by the dealer's company |

| Large/catastrophic losses | Shared per ratio | Transferred above retention |

| Premium structure | Proportional share of original premium | Independently negotiated rate |

In a proportional program, the dealer captures a portion of profits on every policy sold — sharing both upside and downside proportionally. Non-proportional flips this: the dealer absorbs all routine losses but transfers the financial risk of large or catastrophic events. That trade-off — full profit participation versus catastrophic loss protection — is what determines where each structure fits within a dealer's overall program design.

Where Non-Proportional Fits Within a Dealer Program

Some dealer reinsurance programs incorporate non-proportional layers as secondary protection above their proportional core — a safety net that activates if annual claims accumulation exceeds a defined level. This is a supplemental layer, not a replacement for the proportional foundation.

Evaluating whether a program has the right combination of proportional and non-proportional protections requires analyzing claims history, reserve levels, and premium volume. DealerRE works with dealers to structure admin obligor programs with the right risk structure for their volume and claims history, helping them determine whether their current program design matches their actual exposure and growth trajectory.

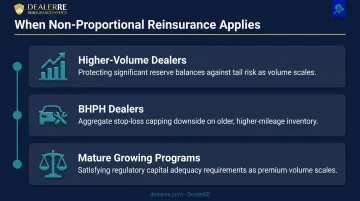

When Non-Proportional Reinsurance Applies to Auto Dealer Programs

Non-proportional elements are not appropriate for every dealer. Three scenarios where they become relevant:

- Higher-volume dealers with substantial reserves may add excess of loss layers to protect against an unusually bad claims year. Once reserve balances are significant, protecting against tail risk can be justified by the capital at stake.

- BHPH dealers face higher mechanical claims frequency due to older, higher-mileage inventory. Aggregate stop-loss structures can cap downside exposure in years with elevated claim activity — useful when the vehicle profile makes loss volatility harder to predict.

- Mature programs with growing premium volume may layer reinsurance protection to satisfy domicile regulatory requirements or meet capital adequacy standards as the program scales.

When Non-Proportional Is Not the Right Answer

Smaller, single-point stores or newer programs with limited premium volume typically don't have the exposure to justify standalone non-proportional arrangements. The added complexity and cost of negotiating a standalone excess of loss layer rarely pencils out at lower volumes.

For these dealers, a well-structured proportional program remains the more practical and profitable choice. Non-proportional is a tool for specific risk management situations, not a universal upgrade.

That said, dealers may still encounter non-proportional structures indirectly. When an administrator or fronting carrier carries its own excess of loss protection, it affects the overall program's stability. Knowing the concept helps dealers ask sharper questions about what protection exists at each level of the program structure.

Common Misconceptions About Non-Proportional Reinsurance

Misconception: "Reinsurance" always means shared profits from the first dollar.

The reinsurer negotiates a separate premium specifically for absorbing tail risk above the attachment point — no interest in routine underwriting profits below the retention. Proportional treaties include profit commission mechanisms tied to actual underwriting outcomes. Non-proportional treaties do not. Conflating the two leads to incorrect expectations about when and how recoveries actually work.

Misconception: Excess of loss coverage means the dealer won't have big losses.

Non-proportional reinsurance caps losses at a defined level. It doesn't eliminate them. The dealer still pays up to the full retention on every qualifying event, and losses below that threshold are entirely the dealer's responsibility.

Sound reserve management remains essential regardless of reinsurance structure above it. Aon's guidance on captive reserves confirms that adequacy certification obligations persist for the retained layer no matter what sits above it.

Misconception: Non-proportional is inherently superior to proportional.

The right structure depends on the dealer's claims profile, volume, and risk tolerance. A proportional program with a healthy loss ratio often outperforms a non-proportional structure where routine losses never trigger reinsurer involvement but the standalone premium is still a real cost.

The fit depends on where the dealer is in their program:

- Proportional works well when claims volume is predictable and the dealer wants to capture underwriting profit consistently

- Non-proportional fits better when the dealer has strong retention capacity but needs protection against infrequent, high-severity events

- Neither is a default — program stage, book size, and loss history should drive the decision

Conclusion

Non-proportional reinsurance is a threshold-based protection structure: the reinsurer only participates above a set retention, absorbing large or accumulating losses rather than sharing routine risk from the first dollar. For auto dealers, this concept matters most as a reference point when evaluating program design — not something most dealers need to implement right away.

For most dealers, a well-structured proportional admin obligor program remains the foundation. As programs mature and premium volume grows, non-proportional layers may become a valuable addition. Understanding where each structure fits helps you ask better questions and make more deliberate decisions as your program scales. If you're evaluating your current F&I structure or considering a dealer-owned reinsurance program, DealerRE can walk you through which approach fits your volume, risk profile, and long-term goals.

Frequently Asked Questions

What is non-proportional reinsurance in simple words?

It's coverage that only activates when a loss exceeds a predetermined amount (the retention). The reinsurer pays nothing on smaller claims but steps in for large or catastrophic losses up to an agreed limit, functioning like a high-threshold backstop rather than a shared risk arrangement.

What is the difference between proportional and non-proportional facultative reinsurance?

Proportional facultative reinsurance shares both premiums and losses at an agreed ratio from the first dollar on individual risks. Non-proportional facultative only triggers when a specific loss exceeds the retention. Both apply to individual placements rather than treaty portfolios, but operate on entirely different payout mechanics.

What are the advantages of non-proportional reinsurance?

Key advantages include:

- Protects against large unexpected losses without disrupting routine operations

- Allows the primary insurer to retain underwriting profits on normal claims

- Provides a predictable ceiling on maximum loss exposure

- Reduces administrative burden since the reinsurer isn't involved in every claim

Do auto dealers typically use proportional or non-proportional reinsurance?

Most dealer-owned reinsurance programs are built on proportional (quota share / admin obligor) structures, where the dealer captures underwriting profit on every policy. Non-proportional layers may be added as supplemental protection in larger or more mature programs, but they're not the default structure.

What does "retention" mean in a non-proportional reinsurance contract?

The retention (also called the attachment point or priority) is the maximum loss the primary insurer absorbs before the reinsurer's obligation begins. Think of it as a deductible in the insurer-to-reinsurer relationship — the reinsurer has no payment obligation until losses cross that line.

Can a dealer-owned reinsurance company use non-proportional coverage?

Yes. Dealer captives can incorporate non-proportional protections — typically aggregate stop-loss or excess of loss layers — but the structure must fit the dealer's premium volume, claims history, and program objectives. It's not standard for smaller programs, but it's a practical and often valuable tool for larger ones.