Introduction

Most people picture insurance as a straightforward two-party deal — a customer buys a policy, the insurer covers the risk. But behind that relationship sits a deeper financial structure that keeps insurers solvent when large losses hit all at once.

That deeper structure is reinsurance.

Often called "insurance for insurance companies," reinsurance lets primary insurers transfer a portion of their risk to a reinsurer in exchange for a premium. The mechanics are straightforward. The financial impact on dealers is not.

For auto dealers selling F&I products like vehicle service contracts, GAP, and CPI, the structure of reinsurance determines where the underwriting profits go — and whether they flow to a third-party provider or back to your dealership.

This article covers the core definition of reinsurance, its key characteristics, the two main types, essential vocabulary, and why it matters directly to your dealership's bottom line.

TLDR

- Reinsurance transfers risk from a primary insurer (the ceding company) to a reinsurer in exchange for a premium

- Core characteristics: risk transfer, two-insurer contracts, capacity enhancement, and financial stability

- Two primary types: proportional (shared premiums and losses) and non-proportional (reinsurer pays only above a loss threshold)

- The original insured has no direct relationship with the reinsurer — all obligations run through the primary insurer

- Dealers can capture underwriting profits directly — instead of handing them to third-party F&I providers

What Is Reinsurance? A Simple Definition

The NAIC defines reinsurance as "a contract between a reinsurer and an insurer" in which "the insurance company — the cedent — transfers risk to the reinsurance company, and the latter assumes all or part of one or more insurance policies issued by the cedent."

Simpler version: it's insurance for insurance companies.

The Two-Contract Structure

Reinsurance operates through two separate contracts:

- Primary Policy — between the original insured (your customer) and the primary insurer

- Reinsurance Agreement — between the primary insurer and the reinsurer

The original policyholder has no direct relationship with the reinsurer. If a claim arises, the customer deals only with the primary insurer. The reinsurer's obligation exists solely in relation to the primary insurer, and only to the extent defined in the reinsurance agreement.

Retrocession: When Reinsurers Buy Their Own Protection

When a reinsurer purchases its own reinsurance from another party, that's called retrocession. The Reinsurance Association of America describes it as "a reinsurance transaction whereby a reinsurer, known as a retrocedent, cedes all or part of the reinsurance risk it has assumed to another reinsurer." For dealers, understanding retrocession matters because it illustrates how deeply layered risk distribution can extend across the reinsurance market.

A Concept With Decades of History

The first dealer-owned reinsurance companies appeared in the 1950s, initially covering credit life and disability insurance through Texas-domiciled entities. Over the following decades, these structures migrated through Arizona and eventually offshore, evolving alongside regulatory changes and dealer sophistication. That history shaped the framework dealers use today, and it's the same framework DealerRE has been operating within since 1994, helping over 400 dealers build and manage their own programs.

Key Characteristics of Reinsurance

Understanding reinsurance means looking past the premium transfer. Several structural and legal characteristics define how these contracts work — and why regulators, courts, and dealers treat them differently from ordinary business agreements.

Risk Transfer

The defining feature of any reinsurance contract is genuine risk transfer — the primary insurer's financial exposure on a policy or portfolio moves, at least partially, to the reinsurer. Without actual risk transfer, the arrangement isn't reinsurance; it's something else entirely (and regulators treat it accordingly).

Contractual Relationship Between Two Insurers

Reinsurance exists strictly between two insurance entities. The original insured cannot file a claim directly against the reinsurer. All obligations flow through the primary insurer, who remains solely responsible to the policyholder regardless of what the reinsurance agreement says.

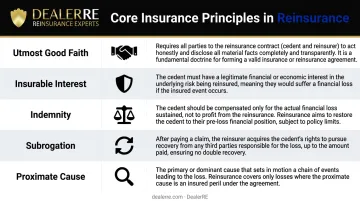

Insurance Principles Apply

The same foundational principles that govern primary insurance apply equally to reinsurance contracts:

| Principle | What It Requires |

|---|---|

| Utmost Good Faith | Full disclosure of all material facts by both parties |

| Insurable Interest | The cedent must have a legitimate financial interest in the risk |

| Indemnity | Reinsurance compensates actual loss — no profit from a claim |

| Subrogation | Reinsurers may pursue third-party recovery through the cedent |

| Proximate Cause | The dominant cause of loss determines coverage applicability |

Misrepresentation on either side can void coverage — the utmost good faith standard leaves no room for selective disclosure.

Capacity Enhancement

One of the most practical reasons insurers use reinsurance: it allows them to accept risks larger than their own capital would otherwise support. By ceding the portion of a risk above their retention limit to a reinsurer, a primary insurer frees up capital — and that freed capital can back additional policies.

For a dealer-owned reinsurance company, this translates directly to scalability. As the Insurance Information Institute notes, freed capital can "support more or larger insurance policies" — meaning a dealer's program can grow alongside F&I volume without hitting a capital ceiling.

Stability in Underwriting Results

Reinsurance smooths out financial volatility. In a year with unusually high claims — a bad winter, a spike in mechanical failures across a portfolio — the reinsurer absorbs losses that exceed the cedent's retention. This protects the primary insurer's financial stability and keeps underwriting results predictable across business cycles.

Customization

That predictability pairs well with another structural advantage: reinsurance arrangements are negotiated, not standardized. Retention levels, premium structures, coverage layers, and contract terms can all be tailored to fit the ceding company's risk profile and business objectives. For dealers, this means a program built around their actual F&I volume, product mix, and reserve strategy — not a generic template designed for someone else's book of business.

The Two Main Types of Reinsurance Explained

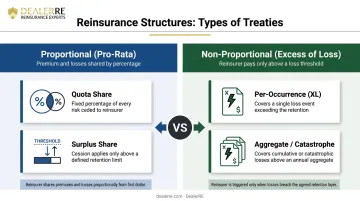

Proportional Reinsurance

In proportional (pro-rata) reinsurance, both premiums and losses are shared between the cedent and reinsurer according to a pre-agreed percentage. There are two primary forms:

- Quota Share — The reinsurer takes a fixed percentage of every policy in a defined portfolio. Premiums and losses split at the same ratio on every contract.

- Surplus Share — The reinsurer covers only the portion of liability that exceeds the cedent's retention limit. Each risk is shared in proportion to how much the reinsurer is actually covering above that threshold.

Proportional arrangements work well when a ceding company wants predictable cash flow, shared administrative costs, and consistent exposure management across a whole book of business.

Non-Proportional Reinsurance

In non-proportional (excess of loss) reinsurance, the reinsurer only pays once the insurer's losses cross a predetermined threshold. Premiums are not shared proportionally; the reinsurer's obligation is triggered by loss size, not policy count.

Two common structures:

- Per-Occurrence — Applies to a single claim event; the reinsurer covers the portion of that loss exceeding the cedent's retention

- Aggregate/Catastrophe — Activates when total losses across a policy period surpass a pre-set threshold, protecting against sustained claim volume

Non-proportional structures are less common in standard dealer F&I programs, where portfolios of VSC and GAP products tend to favor proportional arrangements. That said, understanding the distinction matters when evaluating how any reinsurance program responds under stress.

Facultative vs. Treaty Reinsurance

These two structures represent a separate way of categorizing reinsurance — not by how losses are shared, but by how coverage is applied to individual risks or entire portfolios.

| Feature | Facultative | Treaty |

|---|---|---|

| Scope | Individual risk or policy | Entire class or portfolio |

| Negotiation | Case-by-case | Pre-agreed, automatic coverage |

| Common Use | Unusual or oversized individual risks | Portfolio-wide programs |

| Dealer Relevance | Less common in F&I context | More relevant — dealer programs typically operate here |

Treaty reinsurance is the structure most relevant to dealer F&I programs. It covers an entire portfolio of products under pre-set terms, automatically — which aligns with how dealer-owned reinsurance companies operate across high volumes of vehicle service contracts, GAP, and ancillary products.

Key Reinsurance Terms Auto Dealers Should Know

These terms appear in every reinsurance contract and determine how risk and profit actually flow. Knowing them before evaluating any program puts dealers in a stronger position to ask the right questions.

| Term | Definition |

|---|---|

| Ceding Company | The primary insurer transferring risk to a reinsurer |

| Reinsurer | The insurer accepting the transferred risk |

| Retention / Retention Limit | The maximum risk the cedent keeps for its own account |

| Cession | The portion of risk (and associated premium) transferred to the reinsurer |

| Ceded Premium | The premium paid to the reinsurer in exchange for assuming ceded risk |

| Surplus | In reinsurance, the liability above the cedent's retention that is ceded |

| Ceding Commission | A fee the reinsurer pays back to the cedent to offset acquisition and administrative costs |

| Fronting | An arrangement where a licensed insurer issues policies but passes risk to a reinsurer, used when the reinsurer lacks a license in the required jurisdiction |

Understanding "Lines" in Reinsurance Treaties

A line equals the amount the ceding company retains. A multi-line treaty allows the cedent to cede multiples of that retention to the reinsurer. A 10-line treaty, for example, means the ceding company can cede up to 10 times its own retention amount on any given risk.

For dealers evaluating programs, retention limits and cession amounts have direct practical implications:

- Risk placement: They determine how much exposure sits inside the dealer's own reinsurance company versus what is backed by an A-rated carrier

- Backstop protection: In DealerRE's admin obligor structure, the A-rated insurer assumes ultimate liability if the dealer-owned reinsurance company cannot meet its obligations

- Limited dealer exposure: The dealer's financial risk is capped at formation costs plus accumulated earnings

Why Reinsurance Matters for Auto Dealers

According to Haig Partners' Q1 2025 analysis, publicly owned dealerships averaged $2,505 in F&I gross profit per vehicle retailed , near historic highs. The global vehicle service contract market sits at $34.52 billion, projected to reach $49.85 billion by 2032.

That's a substantial pool of premium dollars. Most dealers never see the underwriting profit from those premiums. Here's why.

The Third-Party Problem

When a dealer sells F&I products through a third-party provider, the dealer earns a commission or markup on each sale. The third-party provider collects the premium, manages claims, and keeps what remains after claims are paid — the underwriting profit.

As DealerRE puts it directly: if your third-party warranty company weren't making a profit off your products, why would they continue doing business with you?

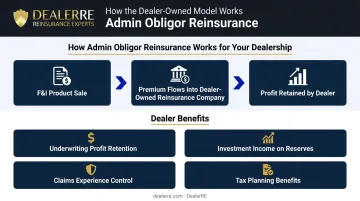

How the Admin Obligor Model Changes the Equation

In an admin obligor reinsurance structure, the dealer establishes their own reinsurance company. Premiums from F&I products flow into that dealer-owned entity instead of to a third party. The dealer:

- Retains underwriting profit when claims are less than premiums collected

- Earns investment income on reserves held in a U.S. trust account

- Maintains control over the claims experience for their own customers

- Accesses tax planning benefits available to qualifying insurance entities

The A-rated carrier backing the program ensures that customer claims get paid even if the dealer's reinsurance company faces financial stress, preserving contractual integrity and the regulatory compliance that define a well-structured program.

Zurich Insurance notes that "the vast majority of dealers participate in some form" of profit participation program. The more useful question is whether your current structure is actually returning that profit to you.

Since 1994, DealerRE has helped more than 400 auto dealers set up and manage their own admin obligor reinsurance companies. Full-service support covers:

- Program structure and reinsurance company setup

- Compliance management, legal filings, and tax returns

- Claims adjudication through administration partners

- F&I training and ongoing financial reporting

Frequently Asked Questions

What are the characteristics of reinsurance?

Reinsurance is a contract between two insurance entities, not involving the original insured directly. Its core characteristics are risk transfer, contractual integrity, application of standard insurance principles (good faith, indemnity, subrogation), and the ability to limit the primary insurer's liability to amounts within its financial capacity.

What is the difference between insurance and reinsurance?

Insurance covers an individual's or business's personal risk through a contract with an insurer. Reinsurance operates between two insurers: the primary insurer transfers part of its risk portfolio to a reinsurer to protect its own financial stability. The original policyholder has no direct involvement in that arrangement.

What are the two main types of reinsurance?

Proportional reinsurance shares premiums and losses on a percentage basis. Non-proportional reinsurance only obligates the reinsurer once losses exceed a set retention threshold. Each type can be structured as facultative (single risk) or treaty (portfolio-wide) arrangements.

What is a ceding company in reinsurance?

The ceding company is the primary insurer that transfers (cedes) a portion of its risk to a reinsurer. It retains part of the risk up to its retention limit and remains solely responsible to the original policyholder for all claims, regardless of what the reinsurance agreement covers.

What is retrocession in reinsurance?

Retrocession is reinsurance of reinsurance. When a reinsurer purchases its own protection from another party to reduce its exposure on risks it has already assumed, that transaction is called retrocession. This layering allows risk to be distributed broadly across multiple market participants.

What is dealer-owned reinsurance?

Dealer-owned reinsurance is a structure where an auto dealer establishes their own reinsurance company to insure the F&I products they sell. Rather than paying underwriting profits to a third-party provider, the dealer captures those profits directly, with an A-rated carrier providing the underlying financial security.