Introduction

Every time a customer signs a vehicle service contract or GAP agreement at your dealership, an insurance company somewhere is collecting premiums and booking profit on the claims that never happen. Most dealers understand the front-end mechanics of F&I sales. Far fewer understand the financial layer sitting behind those products: reinsurance.

This post covers the fundamentals: what a primary insurer is, how reinsurance works, why insurance companies buy it, and what the key structures look like.

More practically, it explains why these concepts matter for dealers evaluating whether to stop sending underwriting profits to third-party providers and start capturing them through a dealer-owned reinsurance program.

If you sell more than 30 cars a month and you've never asked who profits when your warranty claims don't exhaust the reserve fund, this article is for you.

TLDR

- The primary insurer sells policies directly to customers and bears initial claim responsibility

- Reinsurance transfers part of that risk to a second company in exchange for a premium share

- Primary insurers buy reinsurance to manage catastrophic losses, expand capacity, and stabilize earnings

- Dealers who own their reinsurance company capture underwriting profits instead of paying them to third-party providers

- DealerRE has helped over 400 dealers nationwide build these structures

What Is a Primary Insurer?

The primary insurer — also called the ceding company or cedent — is the entity that issues policies directly to individuals or businesses. When a customer buys a vehicle service contract or GAP product, they're entering a contract with the primary insurer. That company collects the premium and accepts financial responsibility for covered losses.

That obligation isn't optional or casual. By law, an insurer must have sufficient capital to ensure it can pay all potential future claims, which is why the NAIC's Risk-Based Capital framework sets statutory minimum capital requirements tied directly to each company's risk exposure.

How This Maps to Auto F&I

In the dealership context, the "primary insurer" is the company standing behind F&I products like vehicle service contracts, GAP, and collateral protection insurance. When a dealer uses a third-party provider, that provider plays the primary insurer role — handling all three of the core financial functions:

- Collecting premiums from each contract sold

- Managing reserves to cover future claims

- Retaining underwriting profit when claims don't exhaust the fund

That profit dynamic is exactly what dealer-owned reinsurance addresses. DealerRE puts it directly to dealers: if your warranty company weren't making a profit from your F&I sales, would they continue doing business with you? The answer is straightforward — your premium dollars are funding their profit, not yours.

Dealers who establish their own reinsurance companies are stepping into a comparable risk-sharing position — capturing a portion of the economics that currently flows entirely to third-party providers.

What Is Reinsurance? Understanding the Core Concept

Reinsurance is, in the simplest terms, insurance for insurance companies. The NAIC describes it as a contract in which a reinsurer indemnifies an insurer for part of the loss it may sustain under its policies.

The Reinsurance Association of America defines the ceding company as "the issuer of an insurance contract that contractually obtains an indemnification for all or a designated portion of the risk from one or more reinsurers."

Three terms define the core structure:

- Cedent / ceding company — the primary insurer transferring risk

- Assuming insurer / reinsurer — the company accepting that risk in exchange for a premium share

- Cession — the act of transferring the risk and corresponding premium

What Policyholders See (and Don't See)

Policyholders never interact with the reinsurer. The customer's contract is with the primary insurer, and the primary insurer remains legally obligated to pay claims even if the reinsurer defaults. The reinsurance relationship exists entirely between the two insurance entities — invisible to the customer but consequential to how both parties manage risk and capital.

The Layered Chain: Retrocession

Reinsurers can themselves purchase reinsurance — called retrocession — from other companies known as retrocessionaires. This creates a layered chain of risk distribution, with each layer absorbing a defined share of potential losses.

That chain has deep roots. Reinsurance dates to at least 1370, when the first recorded contract covered a marine voyage originating in Genoa. From there it expanded to fire insurance, and today it underpins virtually every modern insurance product — including vehicle service contracts and auto-related F&I coverage.

Why Do Primary Insurers Buy Reinsurance?

The RAA identifies four core purposes: limit liability, stabilize loss experience, protect against catastrophes, and increase capacity. Those four purposes translate into five concrete business reasons:

1. Risk Concentration Management

Primary insurers often concentrate heavily in one geography or product line. When claims spike — a hurricane, a flood, a regional catastrophe — reinsurance prevents any single event from wiping out the insurer's capital.

The 2005 hurricane season (Katrina, Rita, Wilma) put that protection to the test. Reinsurers paid approximately 61% of all insured losses, shielding primary carriers from insolvency during one of the most destructive years on record.

2. Underwriting Capacity Expansion

Reinsurance lets insurers write larger policies by passing excess risk to reinsurers, multiplying the volume of business a primary insurer can accept without raising additional capital.

3. Capital Relief and Reserve Reduction

By transferring risk, the primary insurer reduces its required reserves. Reserves are funds set aside to pay future claims — holding fewer of them frees capital for other uses. This reserve relief is recognized explicitly under NAIC Credit for Reinsurance Model Law 785, which states: "Credit for reinsurance shall be allowed a domestic ceding insurer as either an asset or a reduction from liability" when the assuming insurer meets specified conditions.

4. Earnings Stabilization

A bad loss year creates dramatic earnings swings when there's no reinsurance protection in place. Losses above a defined threshold get absorbed by the reinsurer instead, making financial performance more predictable year over year.

5. Market and Product Expansion

Reinsurance lets primary insurers enter new markets or product lines without bearing all the early-stage risk. The reinsurer shares the downside while the insurer builds a track record — a practical path to growth without overexposure.

How Reinsurance Works: Key Structures and Mechanisms

Reinsurance arrangements fall into a few well-defined categories. Understanding them helps clarify how risk is allocated at each layer.

Proportional Reinsurance

In a proportional (or "pro rata") arrangement, the primary insurer and reinsurer share premiums, losses, and expenses at a pre-agreed ratio. If the primary insurer cedes (transfers) 30% of a block of premiums, the reinsurer receives 30% of those premiums and covers 30% of any resulting losses. Dealers favor it for its simplicity and lower administrative overhead.

Non-Proportional Reinsurance

Non-proportional — typically called excess of loss — works differently. The primary insurer retains all losses up to a predetermined threshold, and the reinsurer only pays losses that exceed that amount, up to a defined limit.

A simple example: if the retention is $1 million and the reinsurer covers up to $10 million, any single loss between $1M and $10M falls to the reinsurer. Losses below $1M stay with the primary insurer entirely.

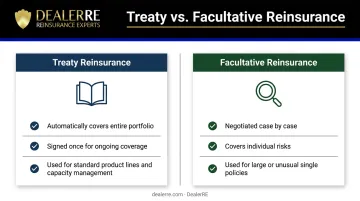

Treaty vs. Facultative Reinsurance

Beyond how losses are shared, reinsurance is also categorized by how the agreement itself is structured — whether it covers an entire book of business automatically or is negotiated policy by policy:

| Type | How It Works | Common Use |

|---|---|---|

| Treaty | Automatically covers an entire portfolio once the agreement is signed | Standard product lines, ongoing capacity management |

| Facultative | Negotiated case by case for individual risks | Large, unusual, or high-value single risks |

For most auto dealers, treaty reinsurance is the relevant structure — it covers their F&I product portfolio automatically, without renegotiating each individual contract.

From Theory to Practice: What This Means for Auto Dealers

Every time your dealership sells a vehicle service contract, GAP product, or ancillary coverage plan, these reinsurance mechanics are already at work — whether your dealership benefits from them or not.

When a dealer routes F&I products through a third-party provider, that provider is functioning as the primary insurer — collecting premiums, managing reserves, and retaining the underwriting profit when claims don't exhaust the fund. The dealer earns the front-end gross. The third-party provider earns everything that's left in the reserve after claims are paid.

The Dealer-Owned Reinsurance Opportunity

Dealers who establish their own reinsurance company step into the risk-sharing role, capturing the underwriting profits that would otherwise flow entirely to the third-party provider. In DealerRE's admin obligor structure, the dealer's reinsurance company is backed by an A-rated carrier, meaning the risk is properly supported by a licensed insurer while the dealer captures the economics of the program.

Premiums flow into a custodial trust account held in the United States. Those funds are invested conservatively, with investment income belonging to the dealer's reinsurance company. After claims are paid, remaining reserves represent underwriting profit.

Once accumulated reserves exceed 125% of unearned premiums, excess funds can be deployed more aggressively: into real estate, back into the dealership, or wherever the dealer chooses.

DealerRE has helped over 400 dealers nationwide build this kind of structure, managing all legal forms, filings, tax returns, and renewals so dealers stay focused on running their business.

The products covered under these programs include:

- Vehicle service contracts

- GAP and debt cancellation coverage

- Collateral protection insurance (CPI)

- Tire & wheel, windshield repair, door ding, and theft protection

- Reinsured certified pre-owned warranty programs

Understanding how primary insurers use reinsurance to manage risk, reduce reserves, and build capital is the foundation for understanding why dealer-owned reinsurance programs work — and whether one makes sense for your dealership.

Frequently Asked Questions

What is the difference between a primary insurer and a reinsurer?

The primary insurer sells policies directly to customers and bears initial claim responsibility. The reinsurer is a second-level insurer that absorbs all or part of the primary insurer's risk in exchange for a premium share. Policyholders only ever interact with the primary insurer.

Why do primary insurers buy reinsurance?

Primary insurers buy reinsurance to protect their financial stability and grow their business without taking on unmanageable exposure. Common reasons include:

- Managing concentrated or catastrophic risk

- Expanding underwriting capacity

- Reducing required capital reserves

- Stabilizing earnings across volatile loss years

- Supporting entry into new markets

What does it mean for an insurer to "cede" risk?

Ceding is the act of transferring part of an insurance liability from the primary insurer to the reinsurer, along with a corresponding share of the premium. It's the mechanism by which risk is legally and financially shifted between the two companies.

What is the difference between proportional and non-proportional reinsurance?

Proportional reinsurance splits both premiums and losses at a fixed ratio. Non-proportional (excess of loss) reinsurance only requires the reinsurer to pay losses that exceed a pre-set threshold retained by the primary insurer.

What is an admin obligor reinsurance structure for auto dealers?

An admin obligor structure is a dealer-owned reinsurance arrangement where the dealer's company acts as the obligor on F&I product contracts, backed by an A-rated carrier. It allows the dealer to capture underwriting profits while the risk remains supported by a licensed insurer.

Can an auto dealer own their own reinsurance company?

Yes. Dealers selling more than 30 cars per month can establish their own reinsurance company to participate in the profits generated by F&I products sold at their dealership. A program administrator handles company setup, compliance filings, and ongoing management — DealerRE has been doing exactly that for dealers nationwide since 1994.