Introduction

Every time a dealer sells a vehicle service contract or GAP policy through a third-party provider, they earn a commission — and then watch the rest of the money walk out the door. The underwriting profit, the difference between premiums collected and claims paid, goes straight to the provider. For many dealerships, that represents thousands of dollars per month in profits they never see.

Reinsurance is the structure that changes this. Most people associate it with large insurance conglomerates managing catastrophic risk, but it has a direct and practical application for auto dealerships of every size.

This article breaks down what reinsurance actually is, how the financial mechanics work, and why dealer-owned programs are one of the most direct paths to recovering F&I profits that franchise dealers, independent dealers, and BHPH operators are currently leaving on the table.

TLDR

- Reinsurance transfers risk (and premium income) from one insurer to another — the entity holding the risk keeps the profit when claims are low

- Dealers selling F&I products generate reinsurance-eligible premiums that currently flow entirely to third-party providers

- Dealer-owned reinsurance lets dealerships capture those underwriting profits in a company they own

- Accumulated reserves can be invested in real estate, business reinvestment, education, and more

- Dealers also gain direct control over claims, tax strategy, and how profits compound over time — advantages third-party providers keep for themselves

What Is Reinsurance?

Reinsurance is a contractual arrangement in which one insurance company (the ceding company) transfers a portion of the risk from its issued policies to another insurer (the reinsurer). In exchange, the reinsurer receives a share of the premiums and assumes a corresponding share of the liability for any claims.

The NAIC describes reinsurance as "insurance for insurance companies," and that framing holds up. The primary insurer issues the policy and collects the premium. Under the reinsurance agreement, a portion of that premium passes to the reinsurer. If claims stay low, the reinsurer profits. If losses spike, the reinsurer pays.

Why It Exists

Reinsurance serves several practical functions for insurance companies:

- Capacity expansion — allows insurers to write more policies without overexposing their balance sheet

- Capital relief — frees up reserves that would otherwise sit idle against potential losses

- Claim stability — evens out financial results across good and bad loss years

- Catastrophe protection — limits the impact of large, unexpected loss events

Each of these functions applies directly to how dealerships generate and manage F&I income. When a dealer sells vehicle service contracts or GAP products, premiums flow out to a third-party provider — along with the underwriting profit. Dealer-owned reinsurance changes that equation, letting the dealer capture what the third party was keeping.

How Reinsurance Works: The Financial Mechanics

When a policy is issued, the ceding company collects the full premium from the policyholder. Under a reinsurance agreement, a defined portion of that premium is passed to the reinsurer, who accepts the corresponding liability. The financial outcome depends on what happens next: low claims mean profit stays with the reinsurer; high claims mean the reinsurer pays out.

Treaty vs. Facultative

There are two structural approaches to reinsurance arrangements:

- Treaty reinsurance — a single agreement covers an entire category of policies automatically. Any contract meeting the agreed criteria is ceded without individual review. This is how virtually all dealer F&I reinsurance programs operate.

- Facultative reinsurance — individual risks are negotiated one at a time. The reinsurer can accept or decline each submission. Useful for unusual exposures, but impractical for high-volume F&I programs.

High-volume, standardized programs like dealer F&I product portfolios fit the treaty model naturally, as confirmed by both Swiss Re's essential guide to reinsurance and industry-specific sources covering automotive programs.

Proportional vs. Excess-of-Loss

Within treaty structures, two sharing arrangements are common:

- Proportional — premiums and losses are shared according to a pre-set ratio. If the reinsurer takes 80% of the premium, they pay 80% of claims. Both parties share the same interest in keeping claims controlled.

- Excess-of-loss (non-proportional) — the reinsurer only pays when losses exceed a predetermined threshold. Used primarily for catastrophic protection, not standard F&I programs.

Most dealer reinsurance programs use proportional arrangements. The fixed split works well for F&I portfolios because the product volume is consistent and the risk profile is well-understood — which also sets the stage for something more strategic than pure risk transfer.

Financial Reinsurance

Financial reinsurance (fin re) takes a different approach. Rather than focusing purely on risk transfer, fin re emphasizes capital management and earnings smoothing. The reinsurer holds and invests premiums over a defined period, returning them minus a margin — regardless of whether a major loss event occurs.

This is the model most closely related to dealer-owned reinsurance structures. The primary goal isn't catastrophe protection. It's controlling three things:

- Where premiums sit — inside the dealer's own reinsurance company, not a third-party carrier

- How they're invested — generating additional return on reserve funds

- Who captures the profit — the dealer, when claims run below the premium base

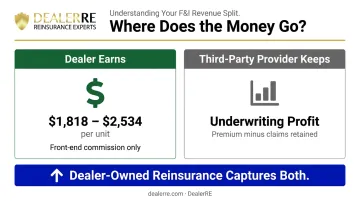

The Financial Impact of Reinsurance on Dealerships

The Profit Leakage Problem

When a dealer sells a VSC or GAP policy through a third-party provider, the transaction looks like a win: front-end gross profit, a satisfied customer, a product sold. What doesn't show up on the deal sheet is the underwriting profit that flows downstream to the provider.

DealerRE frames this with a question worth sitting with: if your warranty company weren't making a profit from your sales, would they continue doing business with you? That question answers itself — and it shows exactly how much value is leaving the dealership on every deal.

F&I remains one of the most profitable departments in the business. Public dealer groups reported average F&I gross profit per vehicle of $2,534 in Q3 2025, while a broader sample of 200+ dealers tracked by VisionAST showed an average of $1,818 per unit across the same general period. The underwriting profit behind those numbers — premium volume not consumed by claims — is where third-party providers build their businesses. That's the margin dealers can recapture by owning the reinsurance structure themselves.

How Reinsurance Restructures Profit Flow

By owning the reinsurance company, the dealer captures the underwriting profit that previously went to the third party. The front-end gross remains intact. What changes is what happens after the sale:

- Premiums are ceded to the dealer's own reinsurance entity

- Reserves are held and invested in that entity's account

- Claims are paid from reserves as they occur

- The difference between premiums collected and claims paid accumulates as profit in the dealer's company

This converts a one-time commission into a recurring, compounding income stream.

Reserve Investment

Once reserves accumulate in the dealer's reinsurance company, they don't sit idle. All investment income belongs to the reinsurance company. Conservative reserve thresholds require initial investment in government bonds, but the dealer directs how excess funds are deployed once balance sheet cash exceeds 125% of unearned premiums — and those funds can move into more aggressive positions.

DealerRE clients have used that capital for real estate purchases, college education funding, dealership reinvestment, and other asset acquisition. The reinsurance company effectively becomes a separate wealth-building vehicle funded entirely by the dealership's existing sales volume.

Tax Planning

Dealer-owned reinsurance companies are typically structured as separate legal entities, often in favorable tax jurisdictions. Property and casualty insurance companies with annual net premiums under $2.2 million may elect under IRC 831(b) to be taxed only on investment income rather than underwriting income — a meaningful deferral opportunity for many dealers.

That opportunity comes with real compliance obligations. The IRS has increased scrutiny of micro-captive arrangements, and 2025 final regulations impose additional requirements around risk transfer and premium diversification. Structures that prioritize tax outcomes over genuine risk management face real exposure. The right approach is to treat reinsurance as a risk management tool first — and work with qualified tax counsel to optimize the structure from there.

Claims Control

When the dealer's reinsurance company bears the claims liability, the financial incentive to manage claims responsibly becomes direct. Lower claims mean more profit retained. This creates natural discipline around:

- Adjudicating claims accurately and consistently

- Driving claims back to the dealer's own service facility

- Monitoring loss ratios and adjusting product pricing when trends shift

Industry sources note that F&I product providers often target loss ratios between 50% and 90%. Parts and labor inflation can push ratios upward, eroding profitability if pricing and terms aren't adjusted. Dealers who own their reinsurance have both the visibility and the incentive to respond before margins compress.

What Is Dealer-Owned Reinsurance?

Dealer-owned reinsurance — also called admin obligor reinsurance — puts the dealer in the position the third-party provider previously held. The dealer establishes their own reinsurance company, which reinsures the F&I products sold at their store. Premiums flow into that entity, claims are paid from it, and underwriting profits accumulate there — not with a third-party provider.

The Admin Obligor Structure

In the admin obligor model, the dealer's reinsurance company is backed by an A-rated insurance carrier. This carrier — rated A or A- (Excellent) by AM Best — provides a layer of financial security ensuring claims can be paid even under adverse scenarios. The dealer's liability covers only formation costs plus accumulated earnings; the A-rated carrier backstops the rest.

That A-rated backing is what makes dealer reinsurance a structured, compliant program — not unprotected self-insurance. Customers receive the same financial security they'd have under any reputable third-party product.

Operational Flow

The process works like this:

- F&I product sold at the dealership — VSC, GAP, ancillary coverage

- Premium collected and ceded to the dealer's reinsurance company

- Reserves invested in the company's trust account

- Claims paid from reserves as contracts are used

- Net underwriting profit accumulates in the dealer's entity as policies expire

What Products Are Included

The product mix determines premium volume — and premium volume determines how much profit accumulates in the dealer's entity. Common inclusions are:

- Vehicle service contracts (VSCs) — highest-volume and typically the most profitable product to reinsure

- GAP insurance — covers the deficiency between insurance settlement and loan balance; DealerRE's GAP product offers 150% or 125% LTV coverage backed by an A-rated carrier

- Collateral protection insurance (CPI) and debt cancellation coverage (DCC) — particularly relevant for BHPH dealers protecting portfolio collateral

- Ancillary products — tire and wheel, door ding protection, windshield repair, theft deterrent

For BHPH dealers, the structure takes on an additional dimension. Customers won't pay on vehicles that don't run. A reinsured VSC creates a customer-funded repair pool — the dealer sells the contract, collects the premium into their own reinsurance entity, and draws from that pool when repairs are needed. Repossessions drop. The dealer owns the reserve. One structure serves two functions: protect the portfolio and build a financial asset the dealer controls.

DealerRE has helped more than 400 auto dealers establish and manage their own admin obligor reinsurance companies since founding in 1994, handling program setup, compliance, claims adjudication, performance reporting, and F&I training.

Key Benefits of Starting Your Own Reinsurance Company

Profit Capture

Instead of earning a front-end commission and walking away, the dealer captures that same commission plus the underwriting profit that previously went to the third-party provider. That profit compounds year over year as the book of business grows and loss ratios are managed effectively.

Wealth Building

The income earned inside the reinsurance entity isn't locked away. DealerRE clients have used accumulated reserves to:

- Purchase real estate

- Fund children's college education

- Reinvest capital into the dealership

- Acquire other personal or business assets

The reinsurance company becomes a wealth-building vehicle funded entirely by activity already happening on the dealership floor, with no new revenue stream required.

Control Over Products and Customer Experience

Dealers who own their reinsurance can structure products more flexibly, approve claims faster, and maintain tighter control over the customer's ownership experience. That translates to stronger CSI, more repeat business, and the ability to offer coverage competitors can't match.

One DealerRE client put it directly: "Our Family Advantage Program has allowed us to offer our customers a warranty that my dealer competitors can't come close to offering."

That kind of competitive separation doesn't happen by accident. DealerRE supports the customer-facing side with F&I training classes (online and in person), menu development, and ongoing staff support, so dealerships can present and sell reinsured products effectively from day one.

Frequently Asked Questions

What is reinsurance in finance?

Reinsurance is a financial arrangement where one insurance company transfers a portion of its risk — and the associated premium — to another company (the reinsurer) in exchange for that company assuming liability for covered losses. It functions as insurance for insurance companies, helping the original insurer stay financially stable and manage exposure across its portfolio.

What is dealer-owned reinsurance?

Dealer-owned reinsurance is a structure where an auto dealer establishes their own reinsurance company to capture the underwriting profits from F&I products sold at their dealership. Rather than those profits flowing to a third-party provider, they accumulate in a company the dealer owns and controls.

How does reinsurance affect dealership profitability?

Reinsurance allows dealers to move beyond one-time F&I commissions and instead accumulate underwriting profits, invest reserves, and build a compounding income stream over time. The result is significantly higher total profitability per deal as their portfolio grows and claims stay well-managed.

What is the difference between treaty and facultative reinsurance?

Treaty reinsurance covers an entire category of policies automatically under a single agreement, while facultative reinsurance covers individual risks negotiated case by case. Most dealer reinsurance programs operate on a treaty basis, as the standardized, high-volume nature of F&I products makes automatic cession the practical choice.

What F&I products can be included in a dealer reinsurance program?

Vehicle service contracts, GAP insurance, collateral protection insurance, debt cancellation coverage, and ancillary products like tire and wheel, door ding, windshield, and theft protection are all commonly included. The specific product mix depends on the dealership type — franchise, independent, or BHPH.

What are the tax advantages of a dealer-owned reinsurance company?

Dealer-owned reinsurance companies structured as separate legal entities may qualify for tax deferral under IRC 831(b), which allows qualifying property and casualty insurers to be taxed only on investment income. Given increased IRS scrutiny, dealers should work with qualified tax counsel and their reinsurance partner to ensure the structure remains fully compliant.