Dealer-owned reinsurance isn't a niche strategy reserved for massive dealer groups. It's a proven, decades-old investment structure that auto dealers across the country have used to build substantial personal and business wealth — by keeping the profits that currently flow out of their dealership every month.

With average F&I gross profit approaching $2,505 per vehicle retailed in Q1 2025, the premium volume moving through a typical dealership's finance office is substantial. The question isn't whether that income exists. It's who keeps it.

TL;DR

- Dealer-owned reinsurance lets you capture 100% of underwriting profits currently going to third-party F&I providers

- Reinsurance returns depend on claims performance you control, not stock market swings

- Earned premiums are investable capital; dealers commonly redeploy them into real estate, education accounts, or dealership growth

- DealerRE handles setup, compliance, tax filings, claims, and bookkeeping so you can focus on running your dealership

Why Reinsurance Is One of the Best Investments Auto Dealers Can Make

An Asset Class Unlike Anything Else in Your Portfolio

Most investments — stocks, bonds, mutual funds — rise and fall with economic cycles. Reinsurance doesn't work that way. Returns are driven by insurance underwriting performance: the gap between premiums collected and claims paid. A market downturn doesn't affect whether a VSC claim gets filed.

Research from Schroders on insurance-linked securities describes these instruments as "truly uncorrelated" — their income streams are driven by insurable events, not equity market sentiment. Academic analysis from UC Berkeley confirms that insurance returns have historically shown little to no correlation with broader market cycles.

That matters for dealers. You already have significant operational exposure to economic conditions through vehicle sales. Reinsurance gives you a profit stream that doesn't compound that risk.

The Buffett Principle — Applied to Your Dealership

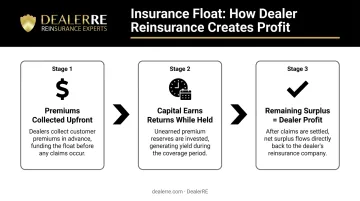

Warren Buffett has credited insurance float as a core engine of Berkshire Hathaway's success for decades. In his 2018 shareholder letter, he described float as "a source of financing that we expect to be cost-free — or maybe even better than that — over time." By year-end 2018, Berkshire's float had reached $122.7 billion.

The principle is straightforward: premiums are collected before claims are paid, creating a pool of investable capital in the interim. Dealer-owned reinsurance applies this same logic at the dealership level — you collect premiums on VSCs and GAP contracts today, claims come later, and the float in between belongs to your reinsurance company and earns returns while it sits.

What Your Idle Capital Is Actually Earning (And What It Could)

According to FDIC national rate data from May 2026, the average savings account earns 0.38% and money market accounts average 0.57%. Dealers parking earned F&I income in bank accounts are, in effect, accepting a fraction of a percent while third-party providers invest that same capital at far higher rates.

The reinsurance industry itself has demonstrated durability over more than 150 years of continuous operation. Consider what that track record looks like in practice:

- Swiss Re reported a record net income of $4.8 billion in 2025

- Its P&C reinsurance segment achieved a combined ratio of 79.4% — a strong underwriting profit indicator

- That performance came during the same environment where savings accounts returned under 0.6%

For dealers selling 30+ units per month, the premium volume flowing through F&I is already substantial. The structure that captures that float — rather than passing it to a third party — is what dealer-owned reinsurance provides.

How Dealer-Owned Reinsurance Captures the Profits You're Currently Giving Away

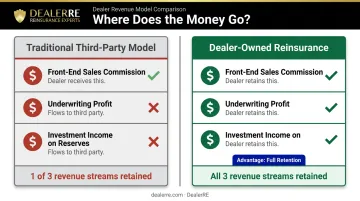

Reinsurance vs. Third-Party F&I Providers

Here's how the traditional model works: you sell a vehicle service contract, the customer pays a premium, and a third-party provider collects it. They pay the claims. Whatever's left over — the underwriting profit — stays with them. You get a flat fee or reserve per contract.

That third party is in business because the math works in their favor. As DealerRE puts it: if your current warranty vendor weren't making a profit from your dealership's volume, why would they keep doing business with you?

Dealer-owned reinsurance flips that equation. Your reinsurance company receives the premiums, pays the claims, and retains whatever remains. Three revenue streams instead of one:

- Front-end sales commission — same as before

- Underwriting profit — the gap between premiums and claims, previously captured by the third party

- Investment income — earned on reserves before claims come due

Admin Obligor vs. Other Structures

The admin obligor (AO) structure is the model DealerRE uses for dealer clients. In this arrangement, the dealer forms a reinsurance company that serves as the product obligor — legally responsible for fulfilling contract obligations — while an A-rated insurer provides backing for regulatory and financial security.

That means the dealer captures the underwriting risk and the underwriting profit, with the financial safety net of a well-capitalized insurer behind it. If claims unexpectedly exceed reserves, the ultimate liability rests with the direct writing insurance company — not solely with the dealer.

Nearly every F&I product your dealership already sells can flow through this structure:

- Vehicle Service Contracts (VSC / extended warranties)

- Guaranteed Asset Protection (GAP)

- Collateral Protection Insurance (CPI)

- Debt Cancellation Coverage (DCC)

- Tire & Wheel, Windshield Repair, Door Ding Protection

- Theft protection products

- Certified Pre-Owned warranty programs

Profit potential scales directly with volume. Consider a dealer writing 150 GAP contracts annually at $499 each: that's $74,850 in reinsurable premium currently leaving the building. Multiply that across VSC and ancillary products, and the retained income adds up fast.

Through DealerRE's administrative partnership with Assured Vehicle Protection (AVP), you get full back-office support: legal filings, tax returns, compliance, claims adjudication, and bookkeeping. You own the company and keep the profits — the infrastructure is already built.

Proven Strategies to Maximize Your Reinsurance Returns

Invest Your Earned Premiums, Not Just Hold Them

Earned premiums held in your reinsurance account aren't meant to sit idle. Initially, trust account regulations require investment in conservative government bonds — appropriate while reserves are building. Once account cash exceeds 125% of unearned premiums, excess funds can be invested in higher-yield vehicles at the ownership's direction.

That's when dealers start directing those earnings toward real assets. Common reinvestment strategies DealerRE clients use include:

- Commercial or investment real estate purchased with reinsurance earnings

- College education accounts for children, funded outside the dealership balance sheet

- Facility upgrades, inventory expansion, or technology back into the dealership

- Watercraft and other appreciating assets for personal wealth-building

Ask your reinsurance administrator about an Investment Policy Statement (IPS) that outlines what investment options are available to your account as it matures.

Focus on Claims Performance to Grow Your Account

Claims performance is the single most controllable variable in your reinsurance returns. When legitimate claims are managed efficiently — appropriate repairs approved, costs kept reasonable — the surplus accumulates faster.

This is also where dealer-owned reinsurance improves customer experience, not just profitability. You're managing your own customers' claims, not an anonymous pool — so the incentive to resolve them fairly and efficiently lands directly with you.

To optimize claims performance:

- Review monthly financial statements from your reinsurance administrator

- Track which products and customer profiles generate the highest claims frequency

- Work with your administrator to analyze whether your F&I product pricing reflects actual loss experience

- Use performance data to refine your F&I menu — more profitable products, better-matched coverage options

DealerRE and AVP provide monthly financial statements and periodic operational reviews to help dealers track claims trends and refine product mix and pricing before losses compound.

Tax Benefits and Building Wealth Beyond Your Dealership

Dealer-owned reinsurance companies are typically domiciled in the Turks and Caicos Islands, which established its captive insurance framework in 1989. The jurisdiction imposes no income tax, capital gains tax, or withholding tax on captive entities. All assets remain in the United States under a trust agreement — the offshore domicile provides the regulatory and tax structure, not asset relocation.

Despite offshore domicile, the reinsurance company is still subject to U.S. federal income taxes. The tax advantage comes through IRS Code Section 831(b), which allows qualifying insurance companies with annual net premiums below a threshold (indexed at $2.65 million for 2024) to elect taxation only on investment income — excluding underwriting income from federal taxation.

DealerRE works with specialized CPAs and legal counsel to keep programs operating within IRS guidelines. Properly structured dealer reinsurance companies are no longer classified as listed transactions — IRS reviews have consistently found them compliant.

Three long-term wealth applications dealers use:

- Estate planning — accumulates wealth in a separate legal entity, shielded from the dealership's operational liabilities

- Retirement funding — underwriting profits compound over time, building a capital pool outside the dealership's balance sheet

- Legacy wealth transfer — transfers accumulated wealth to heirs through a planned, tax-informed ownership structure

The reinsurance company functions as a personal wealth-building vehicle that isn't exposed to the day-to-day liability of running a dealership. If operational issues arise at the dealership level, those assets remain protected and separate.

Understanding Reinsurance Risks and How to Manage Them

No investment is without risk, and dealer-owned reinsurance has specific risk factors worth understanding clearly.

Primary risks in dealer reinsurance:

- Adverse claims experience: If mechanical failures or GAP losses exceed projections, underwriting profit shrinks or turns negative. Disciplined product pricing, conservative underwriting, and actuarially sound premium rates manage this risk directly.

- Poor F&I product pricing: Underpriced products leave insufficient margin between premiums and expected claims. Regular performance reviews and data-driven pricing adjustments address this directly.

- Inadequate claims adjudication: Poorly managed claims inflate losses unnecessarily. Working with an experienced administrator — like DealerRE's partnership with AVP — provides professional claims management expertise.

A Meaningful Difference from Stock Market Investing

With equities, you're a passive participant. Market forces, corporate decisions, and macroeconomic cycles move your portfolio. You have no operational influence.

With dealer-owned reinsurance, the variables are within your control. Your claims experience is shaped by which products you sell, how you price them, and how you manage the adjudication process.

The Schroders ILS analysis notes that during the COVID-19 market crash — when the S&P 500 fell approximately 34% — insurance-linked instruments maintained relative stability precisely because their performance isn't tied to financial markets.

Structural protections in the admin obligor model also limit downside exposure. Each dealer's reinsurance company is entirely independent — no other dealer's claims experience affects yours. And A-rated carrier backing provides a financial safety net if reserves are exhausted.

Frequently Asked Questions

Is reinsurance a good investment?

For auto dealers, dealer-owned reinsurance is an excellent investment structure because it captures profits that already exist within your own operations. You're not seeking external returns — you're retaining income you're currently giving away to third-party providers.

What does Warren Buffett say about insurance?

In his 2002 shareholder letter, Buffett wrote: "Float is money we hold but don't own... During that time, the insurer invests the money." Dealer-owned reinsurance applies the same principle — premiums collected before claims are paid create investable capital that earns returns for the dealer.

What is dealer-owned reinsurance?

Dealer-owned reinsurance is a structure where an auto dealer forms their own reinsurance company to capture underwriting profits from F&I products sold in their dealership — profits that would otherwise flow to a third-party administrator. The result is a wealth-building entity the dealer owns and controls.

What is admin obligor reinsurance?

Admin obligor reinsurance is a specific structure where the dealer's company serves as the product obligor — responsible for fulfilling F&I contract claims — while an A-rated insurer provides backing for regulatory compliance and financial security. The dealer captures full underwriting profits while customers are protected by a financially strong carrier behind the program.

How much profit can auto dealers make through reinsurance?

Profit varies by dealership volume, F&I product mix, and claims performance — and specific figures depend on each dealer's situation. What's consistent is the structure: dealers capturing underwriting profits on their full F&I volume, rather than sharing them with third parties, create a recurring income stream that scales with the business. DealerRE offers a no-obligation business analysis to show dealers what their specific numbers look like.