Introduction

Most auto dealers think carefully about floor plan limits, inventory mix, and F&I product selection. Few think about the financial infrastructure those F&I products actually depend on — reinsurance capacity.

Every vehicle service contract, GAP policy, and ancillary protection product sold in your finance office is backed by a chain of risk transfer that runs from your customer through a primary insurer to a reinsurer. The reinsurer's ability to absorb that risk — its capacity — determines the pricing, availability, and terms of every product in that chain.

Global dedicated reinsurance capital is projected to hit a record $649 billion in 2025, according to AM Best and Guy Carpenter. That number looks comfortable — until the market tightens. Capacity is cyclical, and dealers who don't understand it find out the hard way when pricing shifts, terms change, or product availability narrows.

What follows breaks down what reinsurance capacity actually means, what moves it, and why dealers who own their own reinsurance company have a structural advantage when it contracts.

TL;DR

- Reinsurance capacity is the maximum risk a reinsurer can financially absorb — it directly affects F&I product pricing and availability

- Capacity is driven by capital levels, regulatory requirements, and catastrophe loss cycles

- Hard markets shrink capacity, raise costs, and tighten coverage terms across all insurance lines

- Dealers relying on third-party F&I providers absorb capacity-driven cost increases with no control or protection

- Dealer-owned reinsurance programs shift underwriting profits away from third-party providers and into the dealer's own company

What Is Reinsurance Capacity?

The Basic Definition

Reinsurance capacity is the maximum amount of risk a reinsurer is financially able and willing to absorb. It represents a ceiling — the point beyond which a reinsurer cannot take on additional liability without jeopardizing its ability to pay claims and remain solvent.

A primary insurer issues policies to customers — or, in the F&I context, backs vehicle service contracts and other protection products. That insurer then "cedes" a portion of its risk to a reinsurer in exchange for a share of the premiums. The reinsurer accepts that transferred risk only up to the limits of its available capacity.

Two Types of Capacity — and Why Both Matter

Two related concepts define how much risk the system can carry at any given time:

- Underwriting capacity — the maximum risk a primary insurer can accept based on its own capital and reserves

- Reinsurance capacity — the additional ceiling created when primary insurers transfer excess risk to reinsurers

When a primary insurer cedes risk to a reinsurer, those transferred liabilities no longer count against the primary insurer's own underwriting capacity. This frees the primary insurer to write more policies. But the reinsurer can only accept that transferred risk up to its own capacity limits — so both ceilings matter.

The Floor Plan Analogy

Your dealership can only finance so many vehicles based on your floor plan limit. Exceed that limit and you can't acquire more inventory, regardless of demand. Reinsurance capacity works on the same principle: it's the reinsurer's hard ceiling for risk. When that limit is reached, no more risk gets absorbed — and the effects ripple down to every product backed by that reinsurer.

For dealers, that means a constrained reinsurer can restrict which products get offered, compress coverage terms, or push pricing higher — all without any change to your dealership's own operations.

What Determines Reinsurance Capacity?

Capital Is the Foundation

The most fundamental driver of reinsurance capacity is the reinsurer's capital base — its total financial resources including equity, free reserves, and liquid assets. More capital means more risk can be absorbed. When capital erodes (typically through large catastrophe losses), capacity contracts.

This is why industry analysts track dedicated reinsurance capital as the primary indicator of market health. The current $649 billion figure reflects strong underwriting returns over recent years attracting new capital to the sector.

Regulatory Requirements Set the Floor

Regulators don't allow insurers and reinsurers to underwrite unlimited risk. The NAIC's Risk-Based Capital framework requires every insurer to maintain minimum capital levels based on company size and the riskiness of its operations. Fall below certain thresholds and regulators can intervene — including mandatory management takeover if capital ratios drop below 70% of the authorized control level.

These requirements exist to protect policyholders, but they also mean capacity has hard limits baked in by law.

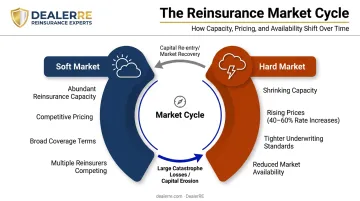

Hard vs. Soft Market Cycles

Reinsurance capacity doesn't stay constant. It moves through cycles:

- Soft market — abundant capacity, competitive pricing, broader coverage terms, more reinsurers competing for business

- Hard market — shrinking capacity, rising prices, tighter underwriting, reduced coverage availability

What triggers a hard market? Large-scale losses that erode reinsurer capital. After Hurricane Ian in 2022 — with damage estimates of $47–$60 billion — rate increases of 40%–60% were the starting point for 2023 treaty renewals, according to CRC Group. The market was already facing a capacity shortfall of $25–$50 billion before Ian hit.

That ripple extends well beyond property catastrophe lines. When reinsurers take large losses and tighten capacity broadly, specialty lines — including the mechanical breakdown and warranty-related coverage backing F&I products — feel the effects too.

Risk Concentration and Portfolio Quality

A reinsurer's willingness to extend capacity also depends on what's already on its books. A reinsurer heavily concentrated in mechanical breakdown or warranty claims may tighten capacity or raise pricing for exactly those lines — directly affecting dealer F&I programs that rely on that reinsurer.

Diversification across risk types helps reinsurers manage aggregate exposure. When one line becomes overloaded, the strain spreads across the entire portfolio.

Retention Balance

Retention is the portion of risk a primary insurer keeps on its own books rather than ceding to a reinsurer. Getting this balance wrong in either direction creates problems:

- Too high — the primary insurer absorbs more risk than it can handle

- Too low — the reinsurer carries everything, straining capacity unnecessarily

What's retained versus what's ceded is a key lever in how efficiently any reinsurance program operates.

How Reinsurance Capacity Works in Practice

Treaty vs. Facultative Structures

Reinsurance agreements come in two main forms:

| Feature | Treaty Reinsurance | Facultative Reinsurance |

|---|---|---|

| Scope | Broad groups of policies | Individual, specific risks |

| Negotiation | One standing agreement | Negotiated per risk |

| Acceptance | Automatic for qualifying risks | Reinsurer can accept or reject |

| Typical use | Ongoing portfolio coverage | High-value or unusual risks |

Most dealer F&I reinsurance programs operate under treaty-style arrangements — a standing agreement that automatically covers qualifying F&I products written through the dealership. Facultative reinsurance comes into play for complex or unusual individual risks that fall outside a treaty's scope.

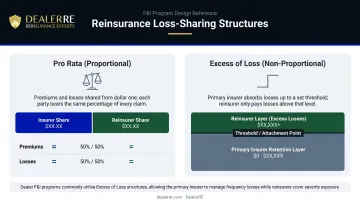

How Losses Are Shared

Under any reinsurance agreement, there are two fundamental ways losses get allocated:

- Pro rata (proportional): Both the reinsurer and primary insurer share premiums and losses in an agreed proportion, starting from the first dollar of loss

- Excess of loss (non-proportional): The primary insurer absorbs all losses up to a set threshold; the reinsurer only pays above that point

Dealer-oriented reinsurance programs commonly use excess-of-loss structures. This protects against high-severity claim events without requiring the reinsurer to share every routine, lower-cost service contract repair — keeping the program efficient and allowing underwriting profit to accumulate when routine claims stay within the retention layer.

Alignment between the reinsurance agreement and primary policy terms is essential. Gaps between the two create uncovered claim exposure — a risk that's particularly relevant for dealer-owned programs where claims handling falls directly on the dealer.

Why Reinsurance Capacity Matters for Auto Dealers

You're Already Operating Inside This System

F&I departments at publicly owned dealerships averaged $2,505 in gross profit per vehicle retailed in Q1 2025, approaching historic highs according to Haig Partners. Every dollar of that F&I gross profit flows through products backed by the reinsurance capacity system.

When you sell a vehicle service contract through a third-party provider, you're operating inside a chain of risk transfer. The third-party provider is backed by a primary insurer, which is backed by a reinsurer. That reinsurer's capacity controls what the third-party provider can offer, at what price, and under what conditions.

How Capacity Pressure Flows Downhill to Dealers

When reinsurers face capacity constraints, the pressure doesn't stay at the top of the chain:

- Third-party F&I product providers face higher reinsurance costs

- Those costs get passed through as reduced dealer margins or increased product pricing

- Coverage terms may tighten, meaning more claims fall outside policy coverage

- In extreme cases, products become unavailable in certain segments

Dealers relying entirely on third-party providers have no visibility into any of this. They don't know which reinsurer backs their products, what that reinsurer's financial condition is, or how capacity pressure is being managed. When the terms change, the dealer finds out after the fact.

The Alternative Position

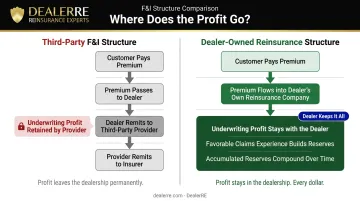

A dealer who owns their own reinsurance company sits in a fundamentally different position. Rather than absorbing the downstream effects of capacity pressure, they're capturing the economics that third-party providers currently keep:

- Premiums flow into the dealer's own reinsurance company rather than a third-party provider

- Underwriting profit (the margin between premiums collected and claims paid) accumulates in the dealer's own account

- Favorable claims experience directly benefits the dealer, not a third-party provider's bottom line

A combined ratio below 100% represents underwriting profit. In a third-party structure, that profit stays with the provider's insurer. In a dealer-owned structure, it stays with the dealer.

Zurich noted in 2025 that "the vast majority of dealers today are in some kind of profit participation program." Dealers outside any participation program are effectively subsidizing a third-party provider's bottom line.

How Dealer-Owned Reinsurance Programs Leverage Capacity

The Admin Obligor Structure

DealerRE structures dealer-owned programs using an admin obligor model. In this structure, the dealer establishes their own reinsurance company — but that company is backed by A-rated primary insurers who carry the ultimate capacity risk.

If the dealer's reinsurance company cannot meet its financial obligations, the direct writing insurance company bears the ultimate liability for claim payments. The dealer's exposure is limited to formation costs plus accumulated earnings. The capacity risk sits with an A-rated, regulated insurer, not the dealer alone.

All funds ceded to the dealer's reinsurance company are held in a U.S.-based trust account, with reserves managed to the backing insurer's requirements. The Trust Agreement requires regulatory guidelines to be followed until balance sheet cash exceeds 125% of unearned premiums. Once that threshold is met, excess funds can be directed toward other investments.

What Dealers Can Reinsure

DealerRE's programs cover the full range of F&I products, including:

- Vehicle Service Contracts (VSCs) for all inventory types

- Guaranteed Asset Protection (GAP) with A-rated carrier backing

- Collateral Protection Insurance (CPI) and Debt Cancellation Coverage (DCC) for BHPH dealers

- Ancillary products: Tire & Wheel, Windshield Repair, Door Ding, Theft Protection

- Certified Pre-Owned (CPO) warranty programs

Programs are available for dealers selling more than 30 cars per month, across franchise, independent, retail, and BHPH operations nationwide.

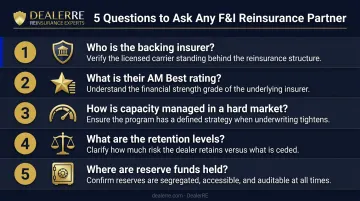

Questions Dealers Should Ask Before Choosing Any F&I Partner

Understanding reinsurance capacity equips dealers to ask better questions. Before committing to any F&I product provider or reinsurance structure, get clear answers to these:

- Who is the backing insurer? Name the carrier, not just the program administrator.

- What is their AM Best financial strength rating? An "A" (Excellent) rating means excellent ability to meet ongoing obligations — anything lower warrants scrutiny.

- How is capacity managed during a hard market? What happens to your product terms and pricing if the reinsurer tightens?

- What are the retention levels? How much risk stays with the primary insurer versus the reinsurer?

- Where are reserve funds held? U.S.-based trust accounts offer more transparency and regulatory protection than offshore arrangements.

Dealers who understand these questions are harder to mislead and better equipped to build programs that hold up when market conditions tighten.

DealerRE has been structuring admin obligor programs since 1994. That three-decade track record spans multiple hard and soft market cycles — the kind of direct experience that shapes how programs are built to perform, not just in favorable conditions, but through the difficult ones too.

Frequently Asked Questions

What does capacity mean in reinsurance?

Reinsurance capacity is the maximum amount of risk a reinsurer is financially able and willing to absorb, determined by its capital base, reserves, and regulatory requirements. Higher capacity means reinsurers can cover more risk and offer more competitive pricing and terms.

What is reinsurance in simple terms?

Reinsurance is insurance for insurance companies. It allows primary insurers to transfer a portion of the risk they've underwritten to a reinsurer in exchange for a share of the premiums, helping insurers manage large losses and remain solvent.

What is the difference between treaty and facultative reinsurance?

Treaty reinsurance covers a broad category of risks under a standing agreement, automatically including all qualifying policies. Facultative reinsurance is negotiated individually for specific, complex, or high-value risks. Dealer F&I reinsurance programs typically use treaty-style structures for this reason.

How does reinsurance capacity affect auto dealers?

When reinsurers tighten capacity, third-party F&I product providers face higher costs and stricter coverage terms, which reduces dealer margins and can limit product availability. Dealers with their own reinsurance programs have direct insulation from these pressures and retain underwriting profits rather than passing them upstream.

What happens when a reinsurer runs out of capacity?

A reinsurer that hits its capacity limit stops accepting new risk or raises pricing sharply. Primary insurers must then absorb more risk themselves, find alternative reinsurers, or reduce the volume of coverage they offer. Each outcome can affect product availability and pricing for dealers downstream.

What is an admin obligor reinsurance program for auto dealers?

An admin obligor program lets a dealer own their own reinsurance company, backed by a financially rated primary insurer that handles regulatory and claims obligations. This structure allows dealers to capture underwriting profits while the backing insurer manages the ultimate capacity risk.