Introduction

Running a dealer-owned reinsurance company means living with a fundamental tension: routine claims are predictable and manageable, but a single bad stretch — a surge of high-severity VSC repairs, a cluster of GAP shortfalls, or a weather event hitting a BHPH portfolio — can wipe out months of underwriting profit in one policy year.

Excess of loss (XoL) reinsurance is designed to prevent that outcome. Rather than sharing every dollar of every claim from day one, XoL steps in only after losses cross a defined threshold — leaving routine profits intact while capping severe loss exposure.

This post covers the essentials:

- How XoL reinsurance works

- The three main structures

- How it compares to quota share

- Key benefits for dealer programs

- How to structure a program correctly

TL;DR

- XoL reinsurance activates only when losses exceed a set threshold — the attachment point — keeping routine underwriting profit with the dealer

- Three structures cover different exposure types: per risk, per occurrence, and aggregate — each targets a distinct loss scenario

- Unlike quota share, XoL doesn't share every premium dollar — it protects only the catastrophic tail

- BHPH dealers face accumulated loss exposure across bad claims years — aggregate XoL is built for exactly that risk

- Accurate historical loss data is essential to fair XoL premium pricing

What Is Excess of Loss (XoL) Reinsurance?

The Core Mechanics

XoL reinsurance is a form of non-proportional reinsurance in which the reinsurer only steps in once losses exceed a predetermined threshold. Below that threshold — called the attachment point or retention — the ceding company absorbs all losses and keeps all underwriting profit. Above it, the reinsurer pays the excess up to an agreed reinsurance limit.

As the Insurance Information Institute describes it: "The primary company retains a certain amount of liability for losses and pays a fee to the reinsurer for coverage above that amount, generally subject to a fixed upper limit."

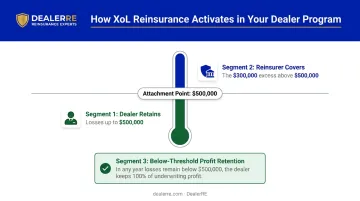

Here's how that plays out in a dealer program:

- Dealer's reinsurance company retains losses up to $500,000 per policy year

- Total claims for the year reach $800,000

- The dealer's company pays the first $500,000

- The reinsurer covers the $300,000 excess

- On any year where claims stay below $500,000, the dealer retains 100% of underwriting profit

Key Terms to Know

| Term | Plain-Language Definition |

|---|---|

| Attachment point / retention | The loss level where reinsurer coverage begins |

| Reinsurance limit | Maximum the reinsurer will pay above the attachment point |

| Ceding company | The dealer's reinsurance company transferring risk |

| Reinsurer | The upstream insurer accepting the excess risk |

Proportional vs. Non-Proportional

The distinction matters for dealer programs. Proportional reinsurance (quota share) involves sharing premiums and losses at a fixed ratio from the first dollar. XoL has no fixed ratio — it's triggered entirely by loss severity or accumulation, not by a percentage split on every policy. As Swiss Re's Essential Guide to Reinsurance confirms, this structure lets the ceding company retain a higher proportion of gross premiums.

In practice, the two structures differ in a few important ways:

- Quota share: Premiums and losses split at a fixed percentage from dollar one — simpler, but the dealer gives up a share of every dollar earned

- XoL: No sharing until losses cross the attachment point — the dealer keeps all profit in good years and gains protection only when it's needed

XoL contracts can be written to activate on individual loss events, a single occurrence that triggers multiple policies at once, or accumulated losses over an entire policy period. How the trigger is defined in the contract directly shapes how much protection a dealer's program actually carries.

The Three Types of XoL Reinsurance

Each structure addresses a different kind of loss exposure. Dealers often use more than one, depending on their product mix and portfolio characteristics.

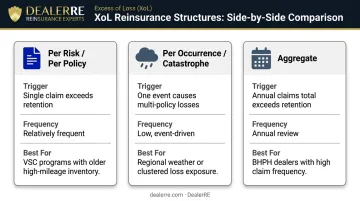

Per Risk (Per Policy) XoL

Per risk XoL covers large individual claims on a single insured asset or policy. For a VSC program, this might mean one vehicle generates an unusually high repair bill — a rebuilt transmission plus engine work on a high-mileage used car, for example. The reinsurer pays the portion of that single claim exceeding the retention.

This structure is sometimes called a "working cover" because it activates relatively frequently compared to catastrophe coverage. It's most relevant for dealers backing VSC programs on older or higher-mileage inventory.

Per Occurrence (Catastrophe) XoL

Per occurrence XoL responds when a single event causes losses across multiple policies at once. A hailstorm damaging twenty vehicles in a BHPH dealer's portfolio in the same week is a clear example — each vehicle generates its own claim, but they all stem from one event.

The contract's definition of "occurrence" determines whether related claims are grouped together. A poorly defined occurrence clause can leave gaps in protection when regional weather events produce clustered losses.

Aggregate XoL

Aggregate XoL protects against a high volume of smaller losses accumulating over a defined period — typically a policy year. If total claims paid during the year exceed the aggregate retention, the reinsurer covers the excess up to the limit. The RAA Glossary defines it as coverage that "indemnifies the ceding company against the amount by which the ceding company's aggregate losses exceed a specified amount."

This structure is particularly well-suited to programs where no single claim is catastrophic, but a run of moderate claims adds up to a damaging year. For BHPH dealers whose claim frequency can be driven by fleet age, economic conditions, or regional weather patterns, aggregate XoL is often the most directly protective structure available.

The right structure depends on where your portfolio risk actually lives. Here's a quick comparison:

| Structure | Trigger | Activation Frequency | Best For |

|---|---|---|---|

| Per Risk (Per Policy) | Single claim exceeds retention | Relatively frequent | VSC programs with older, high-mileage inventory |

| Per Occurrence (Catastrophe) | One event causes multi-policy losses | Low; event-driven | Dealers exposed to regional weather or clustered losses |

| Aggregate | Annual claims total exceeds retention | Annual review | BHPH dealers with high claim frequency from fleet age or economic conditions |

XoL vs. Quota Share Reinsurance

How Quota Share Works

Quota share is a proportional arrangement: every premium dollar and every loss dollar is split at a fixed percentage between the ceding company and the reinsurer, starting with the first dollar of every claim. If the quota share rate is 30%, the dealer's reinsurance company cedes 30% of all premiums and receives 30% reimbursement on all claims.

The Practical Difference

The contrast with XoL is significant for dealer programs:

| Factor | Quota Share | XoL |

|---|---|---|

| Premium sharing | Fixed % of every premium | Lower flat premium cost |

| Loss sharing | Fixed % from dollar one | Only losses above attachment point |

| Routine profit | Shared with reinsurer | Retained 100% by dealer |

| Catastrophe protection | Partial (proportional) | Full above attachment point |

| Best for | Portfolio volatility management | Tail-risk / catastrophe protection |

The table makes the trade-off clear: quota share spreads both risk and profit continuously, while XoL lets dealers keep routine gains and only triggers reinsurer involvement above the attachment point.

Using Both Together

The two structures aren't mutually exclusive. Some programs use quota share to manage overall portfolio volatility while layering XoL on top to cap extreme event exposure. The right combination depends on the dealer's risk appetite, F&I product volume, and factors like average vehicle age, BHPH vs. retail portfolio mix, and historical claim frequency.

Key Benefits of XoL Reinsurance for Dealer Programs

Solvency Protection

A small, concentrated reinsurance company — one backed by a single dealership's customer base rather than a diversified book of business — faces outsized exposure when claims cluster. Swiss Re notes that for "small, local or regional insurers," XoL provides "protection against the biggest and accumulated losses" that could otherwise jeopardize solvency.

The attachment point functions as a financial ceiling on that exposure. No matter how bad a single year gets, the dealer's liability is capped.

Earnings Stability and Capacity

Two additional benefits flow directly from that protection:

- Predictable results — XoL absorbs claims volatility, making year-to-year financial performance more consistent. This matters when dealers are planning reinvestment of underwriting profits into real estate, equipment, or other assets.

- Expanded underwriting capacity — With downside capped, a dealer's reinsurance company can back a larger volume of F&I products or extend into higher-risk coverage categories, such as older vehicles or higher-mileage BHPH inventory, with confidence.

The Insurance Information Institute confirms this directly: "Reinsurance also enables insurers to write larger policies and to cover larger risks."

Cost Efficiency vs. Quota Share

Those capacity and stability gains come at a cost that's typically lower than alternatives. XoL premiums reflect the low frequency of trigger events — the reinsurer is only covering the catastrophic tail, not routine claims. As a result, dealers generally pay substantially less than they would cede under a quota share arrangement. That retained premium stays in the reinsurance company, available for investment, reinvestment into the dealership, or profit distribution.

How XoL Reinsurance Applies to Dealer-Owned Programs

The Concentration Problem

Dealer-owned admin obligor reinsurance companies concentrate risk around a single dealership's customer base. That concentration is the source of both the profit opportunity and the risk — a surge in claims tied to a single region, vehicle model, or economic event can hit the company far harder than it would a diversified insurer with thousands of dealers in its book.

XoL reinsurance addresses this directly by capping what any one bad period can cost the dealer's company.

DealerRE's Program Structure

DealerRE structures dealer programs with A-rated insurer backing, which provides the upstream protection framework within which XoL arrangements operate. If a dealer's reinsurance company faces a severe loss scenario, the A-rated insurer absorbs losses exceeding the dealer company's retention limit — and that relationship ensures the program meets the carrier-quality standards regulators and auditors expect to see.

DealerRE manages the compliance, filings, tax returns, and program administration for dealer clients, so dealers don't navigate these arrangements alone. The full-service model also generates the historical loss data that supports accurate XoL pricing at setup and renewal. That includes:

- Claims adjudication and loss tracking

- Performance reporting and financial bookkeeping

- Compliance management and regulatory filings

The BHPH Application

For buy here pay here dealers, the aggregate XoL structure is especially relevant. BHPH reinsurance programs funded by a dealer's own customer base face claim exposure driven by fleet age, local economic conditions, and regional weather. A single year where customers stretch financially — or where hail moves through a region — can produce an elevated claims count across the entire portfolio without any single claim being catastrophic. Aggregate XoL exists precisely for that scenario — and it's why BHPH dealers benefit from structuring coverage around portfolio-level exposure, not just individual claims.

How to Structure an XoL Program

Getting an XoL program right comes down to three structural choices — and getting any one of them wrong means either overpaying for coverage or being underprotected when a bad loss year arrives.

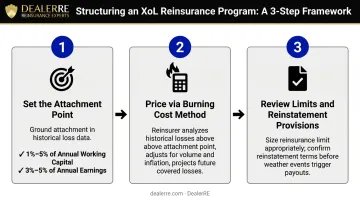

1. Setting the Right Attachment Point

The attachment point calibration matters more than any other structural decision. Set it too low and the dealer pays for coverage that triggers every year — essentially overpaying for routine loss reimbursement. Set it too high and the protection isn't meaningful when a bad year actually arrives.

Actuarial guidance from the Casualty Actuarial Society ties retention levels to risk capital — the amount a dealer is genuinely prepared to absorb under adverse conditions. Common benchmarks include:

- 1%–5% of annual working capital, or

- 3%–5% of annual earnings

In practice, the attachment point should be grounded in the dealer's own historical loss data and adjusted for anticipated volume growth.

2. Pricing via the Burning Cost Method

Once the attachment point is set, that threshold feeds directly into how the premium is calculated. XoL premiums are typically derived using the burning cost method: reinsurers analyze historical losses above the attachment point, adjust for changes in premium volume and inflation, and project the expected future cost of covering excess losses.

This is why accurate loss records matter. A dealer whose program has clean, well-documented claims history can present credible data to a reinsurer and negotiate fair pricing. A dealer with incomplete records faces either inflated premiums or unfavorable terms. DealerRE's performance reporting and claims adjudication services produce exactly the organized loss history a reinsurer needs for a credible burning cost submission.

3. Reviewing Limits and Reinstatement Provisions

Two contract features deserve careful review at placement:

- Reinsurance limit — Caps what the reinsurer pays above the attachment point in a given year. Size this too conservatively and the dealer absorbs the tail of a catastrophic loss out of pocket.

- Reinstatement provisions — After a payout exhausts the limit, most non-marine XoL contracts allow a one-time reinstatement for a pro-rata additional premium. Dealers in storm-prone regions should confirm reinstatement terms at placement — not after a weather event has already triggered a payout.

Frequently Asked Questions

What is XoL reinsurance?

XoL (excess of loss) reinsurance is a non-proportional arrangement where the reinsurer covers losses that exceed a defined threshold, protecting the ceding company from high-severity or catastrophic claims. Unlike quota share, it doesn't share routine losses — it activates only when the retention is breached.

What is the difference between XoL and quota share reinsurance?

Quota share splits all premiums and losses at a fixed percentage from the first dollar of every claim. XoL only activates once losses exceed the retention threshold. This means XoL preserves 100% of routine underwriting profit for the dealer while focusing protection on catastrophic or severe claim events.

How does the attachment point work in excess of loss reinsurance?

The attachment point is the loss level at which the reinsurer's obligation begins. Any losses below it are retained entirely by the dealer's reinsurance company. Losses above it are covered by the reinsurer up to the agreed limit.

What are the main types of excess of loss reinsurance?

Per risk XoL covers large individual claims on a single policy. Per occurrence (catastrophe) XoL responds when one event triggers losses across multiple policies simultaneously. Aggregate XoL protects against total accumulated losses exceeding the annual retention, making it the structure most relevant when a dealer faces a bad claims year.

Can a dealer-owned reinsurance company use XoL protection?

Yes. Dealer-owned admin obligor reinsurance companies can and often should incorporate XoL coverage to cap exposure on VSC, GAP, and mechanical breakdown programs. Proper structuring ensures the dealer retains underwriting profit on routine claims while the reinsurer absorbs excess losses.

How are XoL reinsurance premiums calculated?

Reinsurers typically calculate premiums using the burning cost method, which analyzes the ceding company's historical loss data above the attachment point to estimate expected future covered losses. Accurate, well-documented claims records are essential to getting fair pricing from reinsurers.