Introduction

When a dealer sets up a reinsurance company, they typically receive a stack of legal documents to review. The purchase agreement gets scrutinized. The trust agreement gets explained. But the I&L agreement? It often gets handed over with little more than "sign here."

That's a problem — because the I&L agreement is the document that formally defines what risk the dealer's reinsurance company has accepted, at what percentage, and under what legal terms.

I&L stands for "Interests and Liabilities." In a quota share reinsurance program, this is the agreement each reinsurer signs to record its specific participation percentage and bind itself to the underlying contract terms. For dealers establishing their own reinsurance company, understanding this document is foundational.

This article covers what an I&L agreement is, what it must contain, how it functions in multi-reinsurer programs, and the specific terms dealers should review before signing.

TL;DR

- I&L = Interests and Liabilities — the agreement formally recording a reinsurer's percentage share in a quota share arrangement

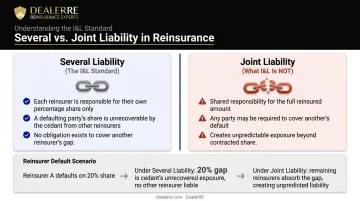

- Each reinsurer signs a separate I&L, creating individual (several) liability — not shared responsibility

- Signing incorporates the quota share contract by reference, binding the reinsurer to all its terms

- In dealer-owned programs, the dealer's reinsurance company acts as the assuming reinsurer and signs the I&L directly

- Several liability: a defaulting reinsurer's unpaid share cannot be recovered from other participants

What Is an I&L Agreement in Reinsurance?

The Reinsurance Association of America defines an Interest and Liabilities Agreement as "a reinsurance contract between the ceding insurer and one or multiple reinsurers in which the percentage of participation of each reinsurer is specified."

That definition captures the structure, but the document's real function is in how it locks each reinsurer to a specific share of both the income and the risk.

The Two Components

- "Interests" — the reinsurer's right to receive a proportional share of ceded premiums

- "Liabilities" — the reinsurer's obligation to pay the same proportional share of covered losses

These two sides are inseparable. A reinsurer that holds a 40% I&L receives 40% of the ceded premium and owes 40% of every covered loss.

How It Binds the Reinsurer

When multiple reinsurers participate in the same reinsurance contract, rather than all signing one document, each signs an individual I&L that ties them to the same underlying contract.

According to Law Insider, the I&L agreement is one "into which the Quota Share Contract is incorporated upon the signing by the (a) Reinsurer of the I&L Agreement, and (b) Insurer of both the Quota Share Contract and the I&L Agreement."

The moment both parties execute, the reinsurer is bound — not just to the I&L itself, but to every term, condition, and exhibit in the underlying contract.

When I&L Agreements Are Used

I&L agreements are most common in quota share arrangements with multiple reinsurers. They're the standard approach when several participants each hold a defined slice of 100% of ceded risk.

The Brokers & Reinsurance Markets Association publishes standardized I&L wording — BRMA 21A-C (Spring 2005) — making this the de facto standard form across the market.

Key Components of an I&L Agreement

Every I&L agreement follows a recognizable structure — regardless of program size, carrier, or ceded percentage. Knowing what to look for in each section helps dealers evaluate whether their reinsurance arrangement is documented correctly and protects their interests if a dispute arises.

Party Identification

Ambiguity in party identification has derailed reinsurance claims. The agreement must clearly name:

- The reinsurer (legal name, domicile, entity type)

- The ceding insurer

- The specific underlying contract being referenced — typically by name, contract number, and effective date

An SEC-filed I&L agreement from Amerisafe demonstrates the standard format: the opening section identifies the reinsurer name, jurisdiction, contract title, effective period, and participation percentage — leaving no room for dispute about who is bound to what.

Quota Share Percentage

The quota share percentage defines exactly how much ceded risk each reinsurer is taking on. In the Amerisafe filing, three separate reinsurers held 5.00%, 7.50%, and 10.00% respectively across the same underlying contract. In other programs — like the Bristol West arrangement — a single reinsurer held 100% of the ceded risk.

Each reinsurer's percentage must be stated explicitly in its own I&L. When reviewing a multi-reinsurer program, dealers should confirm that all participation percentages across issued I&Ls account for the full ceded amount — gaps or overlaps signal a documentation problem.

Incorporation Clause

Most I&L agreements contain language stating that the underlying quota share contract and its attachments "form part of and are expressly incorporated into" the I&L. This is the mechanism that binds the reinsurer to the full contract — not just a summary of terms, but every provision, endorsement, and exhibit.

The incorporation clause matters because it prevents a reinsurer from later claiming it was only bound to a subset of the agreement's terms.

Several Liability Language

The incorporation clause establishes what the reinsurer is bound to — but several liability language determines what happens when one of them can't pay. This clause is the one dealers most often overlook. An SEC-filed I&L agreement (Amerisafe/Alterra Bermuda, 2012) states it exactly:

"The share of the Subscribing Reinsurer in the interests and liabilities of the 'Reinsurer' shall be several and not joint with the share of any other subscribing reinsurer. In no event shall the Subscribing Reinsurer participate in the interests and liabilities of the other subscribing reinsurers."

Several liability means each reinsurer is responsible only for its own stated percentage. If one reinsurer defaults, the others are not obligated to cover the gap. This has direct financial consequences in claims scenarios — which is why the financial strength rating of each participating reinsurer deserves scrutiny before a program is finalized.

Attachments and Exhibits

The I&L itself is rarely a standalone document. The Bristol West I&L, for example, attached Exhibit A (an endorsement) and Exhibit B (a trust agreement) — both carrying the same legal weight as the I&L itself. Trust agreements are particularly important in dealer-owned programs, where the trust account structure governs how ceded funds are held, invested, and accessed for claims.

How I&L Agreements Work in Quota Share Programs

The Quota Share Foundation

In a quota share arrangement, the ceding insurer transfers a fixed percentage of every policy's premiums and losses to the reinsurer. The reinsurer receives its share of premium income and, in return, pays the same percentage of every covered loss from the first dollar. Swiss Re notes that quota share is "ideal for homogenous portfolios like motor" — which maps directly to dealer F&I product reinsurance.

Each I&L represents one reinsurer's slice of that arrangement. Together, all participating reinsurers cover 100% of what was ceded.

The Execution Process

- The ceding insurer executes the main quota share contract

- Each participating reinsurer signs its own I&L Agreement separately

- Upon signing, each reinsurer becomes bound to the contract terms

- The result is a series of bilateral agreements — not one multilateral contract

This bilateral structure is deliberate. As IRMI confirms, "each reinsurer has a separate contractual relationship with the ceding insurer and generally no real contractual relationship with the other reinsurers."

Several Liability in Practice

Several liability means each reinsurer is responsible only for its own percentage — no more. If one reinsurer fails to pay, the others have no obligation to cover that shortfall. A straightforward example:

| Reinsurer | I&L Percentage | Share of $100,000 Loss |

|---|---|---|

| Reinsurer A | 30% | $30,000 |

| Reinsurer B | 70% | $70,000 |

If Reinsurer A defaults, the ceding insurer can only recover $70,000 from Reinsurer B. Neither party owes the other's share. This is why the financial strength of every reinsurer in the program matters — a weak link creates a real exposure gap that no other participant is required to fill.

Dispute Handling in Multi-Reinsurer Programs

When disputes arise, each I&L creates a separate contractual relationship, meaning disputes could technically require separate handling with each reinsurer. BRMA-standardized arbitration language (BRMA 6A series) addresses this through an "act-as-one" provision.

Under that provision, when multiple reinsurers are involved in the same dispute under the same contract, they must participate in arbitration together as a single party. This protects the ceding insurer from relitigating the same facts repeatedly. Key points to understand:

- The "act-as-one" rule applies only to arbitration procedures, not to liability

- Each reinsurer retains its own individual defenses

- Several liability remains intact — acting together doesn't create joint liability

I&L Agreements and Dealer-Owned Reinsurance Programs

When a dealer establishes their own reinsurance company, that company becomes the assuming reinsurer in a quota share arrangement with the fronting or primary carrier. The fronting carrier is the ceding insurer. The dealer's company is the party executing the I&L.

The I&L agreement is the document through which the dealer's company formally accepts its financial obligations — not a background formality, but the binding instrument of participation.

What Dealers Should Verify Before Signing

Before any authorized signatory executes an I&L, these elements deserve close attention:

- Participation percentage — Does it match what was negotiated and agreed upon?

- Incorporated contract terms — Are the underlying quota share contract provisions favorable? The I&L pulls in the entire contract, not just a summary.

- Several liability confirmation — Is the liability explicitly stated as several, not joint?

- Attached exhibits — Are any trust agreements, endorsements, or security arrangements clearly identified and understood?

- Effective date and term — Does the period align with the program structure?

The "several liability" point above is where program structure matters most. DealerRE's admin obligor model backs dealer reinsurance companies with A-rated insurers, directly addressing default risk. If the dealer's company cannot meet its financial obligations, the direct writing insurance company retains ultimate liability for claim payments — limiting the dealer's exposure to formation costs plus accumulated earnings.

The Administrative Reality

Managing the legal forms, filings, and ongoing compliance associated with I&L agreements is one of the most underestimated aspects of running a dealer-owned reinsurance company. DealerRE handles all documentation, tax returns, and renewals as part of its full-service administration model — working alongside legal counsel, CPAs, and program administrators to keep dealer programs compliant and current.

Frequently Asked Questions

What does I&L mean in reinsurance?

I&L stands for "Interests and Liabilities." An I&L agreement is the document through which a reinsurer formally records its percentage share of participation in a quota share reinsurance contract, binding it to both the proportional premiums earned and losses owed under that arrangement.

What is the difference between a sidecar and ILS?

A reinsurance sidecar is a special purpose vehicle that lets investors assume risk on a specific book of business, usually structured as a quota share. ILS (Insurance-Linked Securities) is a broader category of capital market instruments — including catastrophe bonds and collateralized reinsurance — that transfer insurance risk to investors. Sidecars are one specific type of ILS vehicle.

What is the difference between an I&L agreement and a reinsurance treaty?

The reinsurance treaty is the master document setting out all terms and conditions of the arrangement. The I&L agreement is what each individual reinsurer signs to formally adopt those terms and record its specific participation percentage. The I&L incorporates the treaty by reference — making both documents part of the same legal obligation.

Is an I&L agreement legally binding on its own?

Yes. Upon authorized signing, the reinsurer is fully bound to the terms of both the I&L and the underlying quota share contract incorporated into it. The I&L is a standalone, enforceable agreement.

Can a dealer-owned reinsurance company be a party to an I&L agreement?

Yes. A dealer-owned reinsurance company acts as the assuming reinsurer in these arrangements and would execute an I&L to formalize its participation in the ceded risk. This is the core structural mechanism through which the dealer's company receives premiums and assumes loss obligations.

What happens if a reinsurer fails to meet its obligations under an I&L agreement?

Because I&L liability is several — not joint — the ceding insurer can only recover each reinsurer's proportional share. A defaulting reinsurer's portion cannot be collected from the other participants. For dealer-owned programs, this makes vetting your fronting carrier's financial strength a critical step before executing any I&L.