That sequencing question isn't administrative. It determines how much money moves between parties, who absorbs the bulk of a large loss, and whether your reinsurance program performs as intended when a real claim hits. The mechanism governing all of this is called inuring reinsurance.

Misunderstanding it — or leaving it ambiguously drafted in your contracts — can shift tens of millions of dollars in payment obligations based on a single contractual phrase.

TL;DR

- Inuring reinsurance refers to other contracts applied first to reduce the loss before a particular agreement responds.

- Reinsurance that "inures to the benefit of the reinsurer" absorbs losses first, cutting the reinsurer's exposure.

- Reinsurance that "inures only to the benefit of the reinsured" is ignored by the other contract, protecting the reinsured's full recovery.

- The same $100M loss can cost a reinsurer $30M or $80M depending entirely on how inuring language is drafted.

- Precise contract wording is non-negotiable — courts will not fill in what parties failed to write.

What Does "Inuring" Mean in Reinsurance Contracts?

The Reinsurance Association of America's Glossary defines inuring reinsurance as: "a designation of other reinsurance contracts which are first applied pursuant to the terms of the particular reinsurance agreement to reduce the loss subject to the particular reinsurance agreement."

In plain terms: certain reinsurance contracts go first. They absorb their share of a loss before any other contract is even triggered.

The Legal Meaning of "Inure"

In contract law, "inure" means to take effect or to operate to the benefit of a specific party. In reinsurance, it establishes contractual priority — the order in which recoveries are applied before a subsequent layer calculates its own obligation.

This matters most when a ceding company holds multiple contracts simultaneously. A quota share treaty and an excess of loss treaty covering the same portfolio are a common example — both may have exposure to the same loss event.

Which one responds first changes everything.

Two Opposing Designations

| Designation | What It Means | Who It Protects |

|---|---|---|

| Inures to the benefit of the reinsurer | Applied first, reducing the loss before the main contract responds | The reinsurer (lower exposure) |

| Inures only to the benefit of the reinsured | Disregarded when calculating the other contract's obligation | The cedent (full recovery preserved) |

Both designations are standard in the industry. The critical point is that they must be explicitly stated — the same contract language produces completely different financial outcomes depending on which direction the benefit runs.

Practical implications for any ceding company:

- Priority sequence affects net recovery — the contract that responds first directly shapes what the second layer owes

- Explicit language is non-negotiable — ambiguous wording invites disputes at exactly the wrong moment

- Direction of benefit must match intent — a mismatch between what was negotiated and what was written can leave significant exposure uncovered

The Two Scenarios: Who Does the Inuring Reinsurance Benefit?

Understanding the difference in practice requires walking through both scenarios with the same facts.

Scenario 1 — Inures to the Benefit of the Reinsurer

A quota share treaty inures to the benefit of the catastrophe reinsurer. When a loss occurs, the quota share responds first, absorbing its proportional share of the gross loss. What remains after that recovery is the figure the catastrophe layer uses to calculate its own obligation.

The catastrophe reinsurer's exposure is measured against a reduced (net) loss, not the full gross amount. The quota share has already done part of the work.

Scenario 2 — Inures Only to the Benefit of the Reinsured

The quota share does not inure to the catastrophe reinsurer's benefit. The catastrophe layer is calculated against the gross loss — the full amount before any quota share recovery. The catastrophe reinsurer owes its portion of that larger figure. The quota share recovery then applies separately, improving only the cedent's net retained position.

Result: the catastrophe reinsurer bears significantly more of the loss. Its exposure arrives unreduced.

Why Excess and Catastrophe Reinsurers Negotiate This Language

Excess of loss reinsurers commonly push for quota share coverage to inure to their benefit. Without that protection, their attachment point and limit are applied to gross losses — losses the quota share could have already partially absorbed.

Actuarial pricing guidance from the CAS study note on reinsurance pricing is clear on this point: the correct approach for pricing a catastrophe layer is to apply it against the cedent's net retained exposure, after inuring reinsurance has already been accounted for.

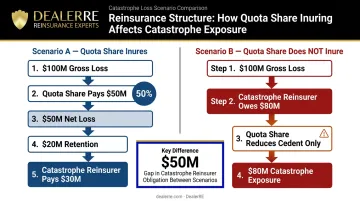

A Worked Example: Seeing Inuring Reinsurance in Action

The numbers below make the contractual stakes concrete. Watch how a single designation shifts $50M of exposure from one party to another — with no change to the underlying loss.

The setup: A ceding insurer holds a 50% quota share reinsurance agreement and a catastrophe excess of loss contract structured as $80M excess of $20M. A single catastrophe loss of $100M occurs.

Scenario A — Quota Share Inures to the Catastrophe Reinsurer

- Gross loss of $100M allocated first to the quota share

- Quota share reinsurer pays $50M (50% of gross)

- Remaining $50M is now subject to the $80M xs $20M catastrophe layer

- Ceding company retains $20M (the attachment point)

- Catastrophe reinsurer pays $30M

Total catastrophe reinsurer payment: $30M

Scenario B — Quota Share Does NOT Inure to the Catastrophe Reinsurer

- Catastrophe layer calculated against the full $100M gross loss

- After the $20M retention, catastrophe reinsurer owes $80M

- Quota share recovery of $50M then reduces only the cedent's net position

- Cedent's net cost drops from $20M to $10M

Total catastrophe reinsurer payment: $80M

What This $50M Gap Means for Your Contract

The same $100M loss costs the catastrophe reinsurer either $30M or $80M — a $50M difference driven entirely by one contractual designation.

That $50M swing isn't a negotiating edge — it's a drafting risk. A contract silent on inuring designation exposes both parties to a dispute at exactly the worst moment: mid-claim. Before any program goes live, the inuring language should be explicit, reviewed by counsel, and confirmed by all parties in writing.

How Inuring Language Appears in Contracts

Inuring reinsurance is not a standalone clause with its own header. It typically appears embedded within other definitions and provisions. Knowing where to look saves time during contract review:

- Ultimate Net Loss (UNL) definitions — The BRMA standard form 54A-L defines UNL as the actual loss paid "after making deductions for all recoveries, salvages, subrogations and all claims on inuring reinsurance, whether collectible or not." A UNL definition that includes inuring reinsurance deductions signals those contracts apply first.

- Net Retained Liability clauses — These define the cedent's retention after inuring contracts are applied, establishing the base on which the treaty responds.

- Treaty cross-references — Some contracts name specific in-force treaties and state explicitly whether those contracts inure to the benefit of the current cover or are disregarded.

Key phrases to identify:

- "Net of inuring reinsurance"

- "Inuring to the benefit of the reinsurer"

- "Gross net written premium income" (GNWPI) calculations — per the RAA Glossary, GNWPI equals gross written premium less premiums paid for reinsurance that inures to the benefit of the cover; those reinsurance costs are already factored into the premium base

- References to which treaties are "disregarded" for purposes of the contract

Courts Will Not Fill the Gap

Ambiguous or silent contract language creates real legal risk. As Larry Schiffer, a reinsurance attorney, has noted, "sloppy contract drafting breeds disputes", and courts are extremely reluctant to imply terms the parties failed to include. The Eleventh Circuit has reinforced this position, refusing to read unstated provisions into reinsurance contracts even when a party argued industry custom supported them.

If the inuring designation is absent or unclear, disputes over loss allocation become drawn-out and expensive. Contracts should name each inuring layer explicitly, confirm whether it applies gross or net of other recoveries, and specify what happens if that coverage becomes uncollectible.

Why This Matters for Dealer-Owned Reinsurance Programs

Dealers who establish their own admin obligor reinsurance companies do not typically hold a single reinsurance contract. Programs covering vehicle service contracts, GAP, collateral protection insurance, and ancillary products can involve multiple layers — each with its own reinsurance structure and each potentially interacting with the others when a significant claim event occurs.

In BHPH programs, where product reserves for mechanical breakdown, debt cancellation, and CPI may all sit within the same reinsurance company, the order in which loss allocation flows across those product layers has a direct effect on:

- How much the dealer's reinsurance company absorbs before external reinsurers respond

- How much is recovered from the fronting carrier or other reinsurers

- How much underwriting profit ultimately flows back to the dealer

Getting this wrong doesn't just create a dispute — it can mean the program pays out in a way the dealer never anticipated, either leaving money on the table or creating unexpected exposure.

DealerRE has helped over 400 dealers structure and manage their own reinsurance programs since 1994. That work includes reviewing the technical contract provisions that determine how losses flow when claims arrive — in coordination with administrators, CPAs, and legal counsel.

Inuring designations that are correctly mapped at program setup prevent misallocation before it happens. Correcting them after a large loss has occurred is far more complicated and costly than addressing them upfront.

Frequently Asked Questions

What does "inure" mean in insurance?

"Inure" means to take effect or operate to the benefit of a specific party. In reinsurance, it describes which party benefits when multiple contracts apply to the same loss — determining the order in which those contracts respond and who bears what share of the claim.

What is the inuring premium?

The inuring premium is the amount paid for reinsurance that inures to the benefit of a particular cover. It is deducted from gross written premium when calculating the subject premium base (GNWPI or GNEPI), since the inuring reinsurance reduces that cover's effective exposure.

What is a cash call in insurance?

A cash call is a reinsurance contract provision — common in proportional treaties like quota shares — that allows a ceding company to request immediate payment from the reinsurer for a large loss, outside the normal periodic settlement cycle. It provides cash flow relief when a significant claim arises.

What is the difference between inuring to the benefit of the reinsurer vs. the ceding company?

When reinsurance inures to the reinsurer's benefit, it reduces the loss before that contract responds, lowering the reinsurer's obligation. When it inures only to the cedent's benefit, it is disregarded entirely in calculating the reinsurer's exposure — leaving the cedent's recovery position intact.

How does inuring reinsurance affect a dealer-owned reinsurance company?

Dealers with layered reinsurance programs need correct inuring designations because contract response order determines how much of a claim the dealer's company absorbs and how much is recovered from external reinsurers. An improperly structured designation can shift significant dollars in an unexpected direction.