Introduction

Most auto dealers interact with reinsurance every single day — every time an F&I manager sells a vehicle service contract or GAP product, a reinsurance transaction is happening in the background. But most dealers are almost never on the profitable side of it.

F&I remains one of the most dependable profit centers in the dealership, with average gross profit reaching $2,565 per vehicle retailed in Q3 2025. Yet most dealers are structured to capture only a fraction of that potential — paying third-party providers and surrendering the underwriting profit by default.

Understanding inward versus outward reinsurance is what changes that. These two terms define which side of the risk transaction you're on. This article breaks down both positions and shows what it looks like to move to the more profitable one.

TL;DR

- Inward reinsurance = accepting risk and receiving premiums (the reinsurer's position)

- Outward reinsurance = paying premiums to transfer risk away (the cedant's position)

- Most dealers default to outward — earning a commission while surrendering all underwriting profit

- Dealers who establish their own reinsurance company move to the inward position, capturing those profits

- The right structure depends on your volume (30+ cars/month is the typical threshold), risk tolerance, and growth goals

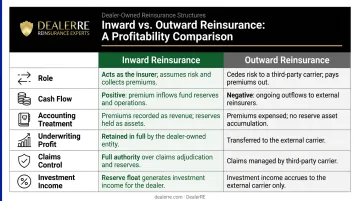

Inward vs. Outward Reinsurance: Quick Comparison

Before going deeper, here's how the two positions compare across every dimension that matters for a dealer:

| Factor | Inward Reinsurance | Outward Reinsurance |

|---|---|---|

| Role | Risk acceptor (reinsurer) | Risk ceder (cedant) |

| Cash flow | Premiums received | Premiums paid out |

| Accounting | Premiums = earned income | Premiums = expense |

| Underwriting profit | Retained by you | Retained by third party |

| Claims control | You manage the experience | Third party manages |

| Investment income | Yours on held reserves | Third party's |

In the standard dealership F&I model, the dealer sits in the outward position. You generate the sale, earn a markup or dealer reserve, and hand the rest — underwriting profit, investment income on reserves — straight to a warranty company or insurer. That's the profit gap the sections below break down.

What Is Inward Reinsurance?

The Core Definition

According to QBE's insurance glossary, inward reinsurance is "reinsurance risk accepted by an insurer from another insurer." The entity accepting that risk is the reinsurer — and it earns premiums in exchange for assuming liability on covered claims.

The mechanics work like this: a primary insurer writes a policy for a customer, then cedes some or all of that risk to a reinsurance entity. The reinsurer receives a share of the premiums and becomes responsible for paying claims up to the agreed contractual limit.

When claims come in below the premiums collected, the reinsurer keeps the difference. That's the underwriting profit.

Two Structural Types Worth Knowing

There are two main categories of reinsurance relevant to dealer programs:

- Proportional (quota share/surplus share): The primary insurer and reinsurer split premiums and losses at a fixed percentage. Simpler to administer and most common in dealer-owned programs.

- Non-proportional (excess of loss): The reinsurer only pays once claims exceed a defined threshold. Offers protection against catastrophic claim events without full risk sharing on every policy.

Most dealer-owned reinsurance programs use a proportional structure because it creates a direct, predictable relationship between premium volume and profit potential.

The Two Profit Streams

Swiss Re's Essential Guide to Reinsurance identifies a critical financial advantage for entities in the inward position: the time lag between when premiums are paid and when claims are made. During that window, reserves sit on the reinsurer's balance sheet and can be invested across asset classes.

That means dealers in the inward position earn from two directions:

- Underwriting profit (premiums minus claims)

- Investment income on held reserves

Entities in the outward position earn neither.

How Dealer-Owned Reinsurance Works

Those two profit streams are exactly what a dealer captures when they move into the inward position themselves.

When a dealer establishes a dealer-owned reinsurance company (DORC), typically through an admin obligor structure, the dealer's own entity steps into that reinsurer role. Premiums from F&I product sales flow into the dealer's reinsurance company rather than to a third-party warranty administrator.

DealerRE structures programs this way. Admin obligor programs are backed by A-rated insurers, so the dealer captures the underwriting profit while maintaining regulatory compliance and a financial safety net. If claims exceed the dealer's reserves, the A-rated carrier covers the overage. The dealer's downside is limited to their formation costs plus accumulated earnings.

The structure also supports multiple F&I product categories: VSCs, GAP, collateral protection insurance, tire and wheel, door ding, windshield protection, and more — all running through the dealer's own company instead of a third party's.

What Is Outward Reinsurance?

Outward reinsurance is the cedant's position. The primary insurer (or any company transferring risk) pays a premium to a reinsurer to reduce its exposure on covered claims. Per QBE's glossary, "the enterprise ceding the risks is the cedant or ceding company and is said to place outward reinsurance." Under accounting standards, that premium is recognized as a reinsurance expense — it flows out of the company's books as a cost.

Why Companies Use It

Outward reinsurance serves legitimate functions for insurers:

- Absorbs exposure on large or catastrophic risks

- Stabilizes earnings during volatile claim periods

- Frees up underwriting capacity to write more policies

- Satisfies regulatory capital requirements

For insurers managing large or unpredictable books of business, outward reinsurance is a sound risk management tool.

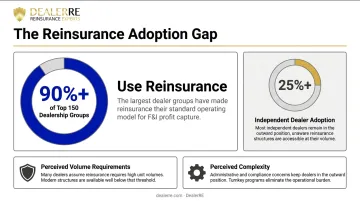

Where Most Dealers Start (and Why They Stay There)

Most dealers land in the outward position by default — and stay there without fully understanding what it costs them.

In the standard F&I arrangement, a dealer sells VSCs and GAP products underwritten by a large warranty or insurance company. The dealer earns a commission — typically 30% to 50% of the retail price, according to Mercer Capital. The underwriting profit — what's left after claims are paid — stays entirely with the third-party administrator.

DealerRE has worked with dealers since 1994 and consistently sees two reasons they stay in the outward position:

- Perceived volume requirements — Many dealers believe reinsurance is only viable for large groups. That's a misconception. Dealers selling more than 30 cars per month often qualify.

- Perceived complexity — Setting up a reinsurance company requires compliance support, legal filings, tax structure, and ongoing administration. Without a partner who manages all of that, the barrier feels insurmountable.

The result: more than 90% of the top 150 dealership groups use reinsurance, while smaller dealers continue paying third-party providers and wondering why their F&I profits feel capped.

Inward vs. Outward Reinsurance: What It Means for Auto Dealers

The Core Financial Question

Every dealer running a standard third-party F&I program should ask one question: who is keeping the underwriting profit on the products I'm selling?

In most cases, the answer is the administrator. AM Best data on Dealers Assurance Company shows a 10-year average combined ratio of 36.2% — meaning roughly 64 cents of every premium dollar remained as profit after claims and expenses over that period. In the outward position, that profit flows entirely to the third-party provider. Dealers in the inward position recapture it.

What Dealers Capture in the Inward Position

Transitioning from outward to inward through a DORC changes the economics significantly. Based on DealerRE's client experience, dealers who make the shift begin capturing:

- Underwriting profit — The surplus after claims are paid, previously retained entirely by third-party providers

- Investment income — Returns on premiums held in trust during the contract term

- Service revenue — VSC claims directed back to the dealer's own service department keep repair dollars in-house

- Tax planning flexibility — Under IRC Section 831(b), qualifying reinsurance companies are taxed only on investment income, not underwriting income, up to approximately $1.2 million in annual premiums

DealerRE clients have described this as realizing "hundreds of thousands of dollars of underwriting profit that they did not know was available previously." One dealer called it "one of the best decisions I ever made in the used car business."

Who Should Consider Moving Inward

Not every dealer is ready for a DORC. The inward position works best for:

- Dealers selling 30+ cars per month consistently

- Operations with a stable, predictable F&I product mix

- Dealers willing to commit to proper reserve management and ongoing administration

- Groups looking for long-term wealth-building tools, not just short-term income

The admin obligor structure DealerRE uses reduces the risk of self-insuring. The A-rated carrier backstop protects dealers from catastrophic loss years — auto repair costs have risen more than 20% in recent years, pushing loss ratios upward across the industry. That protection is real.

What DealerRE Manages on the Dealer's Behalf

The administrative burden that historically made DORCs feel inaccessible is one DealerRE handles entirely:

- All legal forms, filings, tax returns, and renewals

- Claims adjudication (handled through Assured Vehicle Protection)

- Monthly financial statements and performance reporting

- F&I training and staff onboarding

- Compliance coordination with CPAs and legal counsel

The dealer's role is to run their business. DealerRE manages the infrastructure that makes the inward position sustainable.

Conclusion

Outward reinsurance isn't a mistake — it's where most dealers start, and it provides a functional structure for selling F&I products without the complexity of self-administration. But it comes with a real cost: the underwriting profit on every policy sold flows to a third party, not back to the dealership.

Inward reinsurance, through a properly structured dealer-owned program, reverses that flow. Instead of funding a vendor's bottom line, the dealer captures:

- Underwriting profits on every policy sold

- Investment income earned on reserves

- Direct control over the claims experience

- A tax-advantaged financial asset that grows alongside the dealership

The first step is knowing which side of the transaction you're currently on — and what it's costing you to stay there. DealerRE has helped over 400 dealers across the country make that evaluation and, for those who qualify, build programs that work for them rather than for their product vendors.

To explore whether a dealer-owned reinsurance program fits your business, call (804) 824-9533 or request a free dealership analysis at DealerRE.com.

Frequently Asked Questions

What does inward reinsurance mean?

Inward reinsurance refers to the position of the entity that accepts transferred risk from a primary insurer. That entity — the reinsurer — receives premiums in exchange for assuming liability on covered claims, and retains any underwriting profit when claims come in below premiums collected.

What is outward reinsurance?

Outward reinsurance is when an insurer or cedant transfers risk to a reinsurer by paying a premium. That premium is recognized as a reinsurance expense on the cedant's books, reducing claims exposure but surrendering the underwriting profit to the reinsurer.

What are the two main types of reinsurance?

Proportional reinsurance (quota share or surplus share) splits premiums and losses between the primary insurer and reinsurer at a fixed ratio. Non-proportional reinsurance (excess of loss) only triggers the reinsurer's liability once claims exceed a defined threshold — the primary insurer absorbs everything below that level.

Can an auto dealer own their own reinsurance company?

Dealers can establish dealer-owned reinsurance companies (DORCs), typically structured as admin obligor programs backed by A-rated insurers. This places the dealer in the inward reinsurance position, allowing them to retain underwriting profits from F&I product sales rather than surrendering those profits to third-party providers.

How does outward reinsurance affect a dealership's F&I profits?

Third-party F&I providers keep the underwriting profit — what remains after claims are paid. The dealer earns only a commission or dealer reserve, typically 30–50% of the retail price, with no share of the surplus when claims fall below premium collections.