Understanding the difference between insurance and reinsurance is what changes that equation. These aren't abstract financial concepts. They're the mechanism that determines whether underwriting profits build someone else's balance sheet or yours.

This article explains both terms clearly, maps the key differences, and shows how auto dealers can use the reinsurance layer to stop being a distribution channel and start being a profit center.

TL;DR

- Insurance transfers risk from a policyholder to an insurer in exchange for a premium.

- Reinsurance moves risk between insurers: the primary insurer (cedent) passes exposure to a reinsurer, with no policyholder involvement.

- The two main reinsurance structures are treaty (portfolio-wide, ongoing) and facultative (policy-by-policy, high-risk items).

- Auto dealers can own their own reinsurance companies through an admin obligor structure, capturing F&I underwriting profits instead of sending them to third parties.

- DealerRE has helped more than 400 dealerships do exactly this since 1994.

What Is Insurance?

Insurance is a legal contract between a policyholder — an individual or business — and an insurer. The insurer agrees to cover specific financial losses in exchange for regular premium payments. The Insurance Information Institute describes the core function simply: substituting "payment of a small, known fee — an insurance premium — to a professional insurer in exchange for the assumption of the risk of a large loss."

The policyholder trades uncertainty for predictability. Instead of absorbing a potentially catastrophic loss out of pocket, they pay a manageable, known cost upfront.

F&I Products as Insurance

At the dealership level, this plays out in the F&I office every day. Your customers buy:

- Vehicle Service Contracts (VSCs): Cover mechanical breakdown from defects and wear and tear. Technically not insurance under the NAIC Service Contracts Model Act — but regulated similarly in most states.

- GAP Insurance: Covers the gap between a vehicle's actual cash value and the remaining loan balance after a total loss. Regulated as an insurance product.

- Credit Life Insurance: Pays off a loan balance if the borrower dies. Regulated as insurance.

- Ancillary products: Tire and wheel, windshield, theft protection — often bundled with VSC programs.

The critical detail for dealers: premiums collected on these products flow to the product provider, not back to your store. Publicly owned dealerships averaged $2,505 in F&I gross profit per vehicle retailed in Q1 2025, according to Haig Partners — approaching all-time highs.

That figure reflects front-end gross only. The underwriting profit sitting behind those premiums goes to the product provider — not your store.

What Is Reinsurance?

Reinsurance is a contract between a primary insurer (called the cedent) and a reinsurance company (the reinsurer). The reinsurer assumes a share of the cedent's risk in exchange for a portion of the premium.

The original policyholder has no relationship with the reinsurer at all. As the U.S. Treasury's Federal Insurance Office confirms, "underlying policyholders are not parties to the reinsurance contract and typically hold no rights or obligations under it."

Why Insurers Buy Reinsurance

The NAIC outlines seven reasons primary insurers use reinsurance:

- Capacity — underwrite more policies without overextending the balance sheet

- Stabilization — smooth out volatile claims years

- Financing — support growth without raising external capital

- Catastrophe protection — absorb large, concentrated loss events

- Exiting business lines — transfer risk from discontinued products

- Risk spreading — distribute exposure across a broader pool

- Expertise acquisition — access specialized underwriting knowledge

Treaty vs. Facultative Reinsurance

These are the two primary structural formats:

| Treaty Reinsurance | Facultative Reinsurance | |

|---|---|---|

| Scope | Entire portfolio or class of business | Individual policy or risk |

| Obligation | Both parties must cede/accept all covered risks | Reinsurer can accept or decline each case |

| Underwriting | No policy-by-policy review | Case-by-case analysis |

| Best for | Ongoing, predictable risk classes | High-value or unusual individual risks |

Treaty is a standing blanket arrangement covering an entire book of business. Facultative is negotiated risk by risk, used when a single policy is too large or unusual to fit the treaty terms.

Retrocession: One Layer Deeper

Reinsurers themselves sometimes buy reinsurance — called retrocession. The reinsurer becomes a retrocedent, purchasing coverage from a retrocessionaire. This layering distributes exposure across a global network — which is why a major catastrophe in one region ripples through reinsurance balance sheets worldwide. Global reinsurance dedicated capital reached $769 billion in 2024, up 5.4% year-over-year.

The Dealer Connection

Under a dealer-owned admin obligor reinsurance structure, your dealership's own reinsurance company assumes the risk on the F&I products you sell. Instead of that risk — and the associated underwriting profit — flowing to a third-party provider, it flows into your company. When claims run light, you keep the surplus. You are the reinsurer.

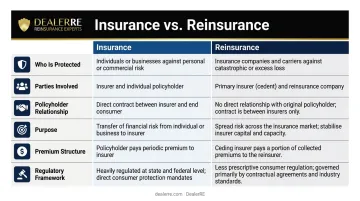

Insurance vs. Reinsurance: Key Differences

These two concepts operate at different levels of the same risk system. Here's how they compare across the dimensions that matter most:

| Insurance | Reinsurance | |

|---|---|---|

| Who is protected | Individual or business policyholder | Primary insurer (cedent) |

| Parties involved | Policyholder + insurer | Cedent + reinsurer |

| Policyholder relationship | Direct — files claims, pays premiums | None — no privity of contract (no direct legal relationship) |

| Purpose | Cover everyday risks (accidents, mechanical failure, theft) | Protect insurer from catastrophic or excess loss |

| Premium structure | Fixed amount set at policy inception | Percentage of cedent's premium base |

| Regulatory framework | Heavy state consumer protection regulation | Contract law; NAIC Credit for Reinsurance Model Law |

On Regulation

Dealers exploring their own reinsurance program operate in a different regulatory environment than standard insurance. Consumer insurance contracts are subject to rate-and-form filing requirements, consumer protection statutes, and state insurance department oversight. Reinsurance contracts — between two sophisticated commercial parties — operate primarily under general contract law.

The NAIC's Credit for Reinsurance Model Law (Model #785) is the governing framework dealers need to understand. Key points:

- Governs how domestic insurers take accounting credit for reinsurance purchased

- 2019 revisions became an NAIC accreditation requirement in September 2022

- Now adopted across all 56 U.S. jurisdictions

Dealer-owned reinsurance programs operate within this framework, backed by A-rated carriers who maintain the ultimate claims liability.

Dealer-Owned Reinsurance: How Dealers Capture F&I Profits

Your third-party warranty and F&I product providers are profitable businesses. They're profitable because the premiums your customers pay exceed the claims your customers file — and they keep the difference. That spread is underwriting profit. Right now, it belongs to them.

A dealer-owned admin obligor reinsurance company changes the equation. You become the reinsurer. When claims run below premiums, the profit stays in your company — not theirs.

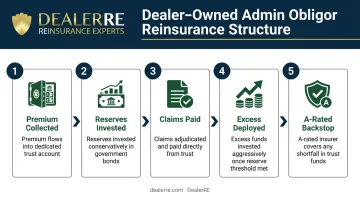

How the Structure Works

When a customer buys a VSC or GAP policy at your F&I desk:

- The premium flows into your reinsurance company's trust account, held at a U.S. trust company.

- Reserve funds are invested conservatively — typically in government bonds — and investment income belongs to your company.

- When a claim is filed, the administrator (DealerRE works with Assured Vehicle Protection) adjudicates and pays from the trust.

- Once reserve requirements are met (typically 125% of unearned premiums), excess funds can be invested more aggressively at your direction.

- If your reinsurance company can't meet obligations, the A-rated direct writing insurer covers the gap — limiting your liability to formation costs plus accumulated earnings.

What Dealers Actually Gain

Beyond retained underwriting profit, the financial benefits include:

- Accumulate underwriting income in a tax-advantaged structure — companies under $2.2M in net premiums may elect IRC Section 831(b) taxation on investment income only

- Deploy earned reserves into real estate, dealership reinvestment, or other assets outside the trust

- Drive repair work back to your service department by staying directly involved in claims adjudication

- Build stronger repeat and referral business through tighter control of the customer ownership experience

DealerRE's Role

Since Tim Byrd founded DealerRE in 1994, the company has helped more than 400 dealerships — franchise, independent, and BHPH — establish and manage their own admin obligor reinsurance programs.

DealerRE handles all legal filings, tax returns, compliance management, and performance reporting. F&I training is available both online through DealerRE Academy and in-person.

As one long-time DealerRE client put it: "Without question, starting our own Reinsurance Company is one of the best decisions I ever made in the used car business."

To understand what's at stake: the VSC market alone was projected to reach $45 billion by 2024, with 93% of VSCs sold at the point of vehicle purchase. That's a substantial premium pool flowing through F&I offices every day — most of it currently going to third-party providers.

If you're selling more than 30 cars a month and currently sending F&I premiums to a third-party provider, it's worth understanding what that program is actually earning — and whether those profits could stay in your operation instead.

Conclusion

Insurance and reinsurance aren't competing options for dealers. They operate at two different levels of the same risk-transfer system. Your customers need insurance; that doesn't change. What changes is whether your dealership passively distributes F&I products for someone else's benefit, or actively participates in the reinsurance layer where the real profits accumulate.

Understanding what reinsurance is — and how it differs from insurance — is the first step. The second step is asking whether the underwriting profits currently leaving your store should be coming back instead. DealerRE helps dealers answer that question — and act on it.

Frequently Asked Questions

What is the difference between insurance and reinsurance?

Insurance protects individuals and businesses from financial loss by transferring risk to an insurer in exchange for premiums. Reinsurance protects insurance companies themselves from large or concentrated losses — it runs between two insurance entities, and policyholders never deal with the reinsurer directly.

What is an example of reinsurance in the auto dealer context?

When a dealership sells a vehicle service contract, the premium goes to the third-party provider. In a dealer-owned reinsurance program, the dealership's own reinsurance company assumes that risk — and keeps the underwriting profit when claims are low rather than sending it to an outside vendor.

Can a business own its own reinsurance company?

Yes. Businesses — including auto dealerships — can own their own reinsurance companies through an admin obligor structure. This lets them retain underwriting profits from F&I products, control their claims experience, and invest premium reserves for additional returns.

What are the two main types of reinsurance?

Treaty reinsurance covers an entire portfolio of policies under a single ongoing agreement. Facultative reinsurance is negotiated policy by policy for specific high-risk or high-value risks, with the reinsurer free to accept or decline each one.

How does reinsurance benefit auto dealers specifically?

Dealer-owned reinsurance lets dealers capture underwriting profits from F&I products like VSCs and GAP instead of sending that income to third-party providers. Beyond profit capture, dealers also gain tax planning advantages under IRC Section 831(b), the ability to invest premium reserves, and direct control over the customer claims experience.

Is reinsurance regulated?

Yes. Reinsurance is regulated at the state level through frameworks including the NAIC's Credit for Reinsurance Model Law, which has been adopted in all 56 U.S. jurisdictions. Dealer-owned programs operate under A-rated insurer backing and comply with applicable state requirements.