The distinction matters more than you might think. Reinsurance is something dealers can actively participate in through dealer-owned programs, capturing F&I profits that currently flow to third-party providers. Retrocession operates at a completely different level of the insurance chain — one that has nothing to do with dealer operations. Mixing up the two can mean missing a real profit opportunity.

This article breaks down both concepts clearly, explains the risk chain from policyholder to retrocessionaire, and clarifies exactly where dealer-owned reinsurance fits.

TL;DR

- Reinsurance transfers risk from a primary insurer to a reinsurer — one level up from the policyholder

- Auto dealers can own and operate a reinsurance company to capture F&I underwriting profits directly

- Retrocession is when a reinsurer transfers risk to another reinsurer (a retrocessionaire) — one level above reinsurance

- The risk chain runs: Policyholder → Primary Insurer → Reinsurer → Retrocessionaire

- For auto dealers, the actionable opportunity is at the reinsurance layer — not retrocession

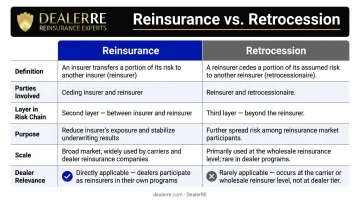

Reinsurance vs. Retrocession: Quick Comparison

Here's how reinsurance and retrocession compare directly:

| Factor | Reinsurance | Retrocession |

|---|---|---|

| Definition | Insurer transfers risk to a reinsurer | Reinsurer transfers risk to a retrocessionaire |

| Parties involved | Primary insurer (cedent) + reinsurer | Reinsurer (acting as cedent) + retrocessionaire |

| Layer in risk chain | First layer above primary insurance | Second layer — above reinsurance |

| Primary purpose | Expand capacity, stabilize underwriting results | Manage reinsurer's own accumulated exposure |

| Scale | Broad — used across all insurance lines | Concentrated in catastrophe and specialty lines |

| Dealer relevance | Direct — dealers can own a reinsurance company | None — wholesale institutional tool only |

The chain works like this: Primary Insurer → Reinsurer (reinsurance) → Retrocessionaire (retrocession). Dealers operate at the reinsurance layer — owning and controlling their own reinsurance company, and capturing the underwriting profits that would otherwise go to a third-party provider.

What Is Reinsurance?

The NAIC defines reinsurance as a contract in which a reinsurer agrees to indemnify a ceding company against all or part of the loss it may sustain under its insurance policies. Plain language version: it's insurance for insurance companies.

The primary insurer — called the cedent — transfers a portion of its risk to a reinsurance company in exchange for a premium. The reinsurer doesn't deal directly with policyholders. It reimburses the insurer for claims paid, rather than paying those claims itself.

Why Reinsurance Exists

Reinsurers serve four core functions for primary insurers:

- Capacity expansion — allows insurers to underwrite more policies than their capital alone would support

- Result stabilization — smooths out the volatility of unpredictable loss years

- Catastrophic loss protection — limits exposure when a single event generates massive claims

- Financial stability — supports an insurer's target risk profile without overexposing its balance sheet

Two Structural Types Worth Knowing

Proportional reinsurance splits premiums and losses at a fixed ratio. Quota share is the most common form: a 40% quota share means the reinsurer receives 40% of premiums and covers 40% of losses.

Non-proportional (excess-of-loss) reinsurance only triggers when losses exceed a defined threshold. It's the standard structure for catastrophe protection, where the reinsurer absorbs the worst of a bad year without sharing routine losses.

How Dealers Fit In

Those same structural principles apply directly to automotive F&I. Auto dealers can own their own reinsurance company through what's called an admin obligor reinsurance structure — meaning the dealer's company acts as the administrator and obligor of the products sold, not just a passive risk participant. Here's how it works in practice:

- The dealer's F&I office sells products like VSCs, GAP, and ancillary coverage

- A direct-writing insurance company (the primary insurer) underwrites those products

- The dealer's reinsurance company reinsures that business, capturing the underwriting profits

- All funds are held in a U.S. trust account — none sent offshore

Those underwriting profits exist in every deal — the question is who captures them. DealerRE has helped dealers across franchise, independent, and BHPH operations recapture that income since 1994 using this same admin obligor model.

What Is Retrocession?

Retrocession is reinsurance for reinsurers. When a reinsurance company has accumulated too much exposure on its own books, it cedes a portion of that risk to another reinsurer — called a retrocessionaire.

The Insurance Information Institute defines it simply: retrocession is "the type of reinsurance bought by reinsurers." The original primary insurer plays no role in this transaction. Retrocession is entirely a back-end arrangement between large institutional reinsurers.

Types of Retrocession

| Type | Category | Description |

|---|---|---|

| Quota Share | Proportional | Retrocessionaire takes a fixed percentage of premiums and losses |

| Surplus Share | Proportional | Covers exposures exceeding the reinsurer's retention limit |

| Excess-of-Loss | Non-proportional | Pays when losses exceed a defined threshold |

| Stop-Loss | Non-proportional | Covers aggregate losses above a set ratio |

| Treaty | Placement | Automatic coverage for entire portfolios |

| Facultative | Placement | Individual risk, negotiated case by case |

Treaty retrocession is the most common form for standard portfolios; facultative is reserved for complex, individually negotiated risks. Both operate well above the level of any single product line.

A Real-World Example

Swiss Re's retrocession program is managed centrally by its Alternative Capital Partners team in Zurich and London. The program focuses on "peak exposures" — primarily natural catastrophes like California earthquakes and Atlantic hurricanes — where Swiss Re needs to transfer accumulated risk off its own balance sheet.

That context makes the scale clear: retrocession exists to manage exposure to billion-dollar hurricane seasons, not the kind of product risk pools dealers encounter in F&I.

Where Retrocession Is and Isn't Used

Retrocession is concentrated in:

- Property catastrophe (nat-cat) lines

- Large commercial reinsurance books

- Specialty and man-made risk portfolios

It plays no role in dealer F&I reinsurance. No authoritative source connects retrocession to VSCs, GAP, or any F&I product risk pool.

Key Differences Between Reinsurance and Retrocession

Parties Involved

This is the single most important structural distinction. Reinsurance connects a primary insurer with a reinsurer. Retrocession connects a reinsurer (now acting as cedent) with a retrocessionaire. The mechanism is identical — the structure simply moves one level higher in the risk chain.

Position in the Risk Chain

Visualize it as four links:

Policyholder → Primary Insurer → Reinsurer → Retrocessionaire

- Reinsurance covers the second link

- Retrocession covers the third

Purpose and Scale

Reinsurance is used broadly across all insurance markets to manage underwriting risk. Retrocession is specifically used by institutional reinsurers to manage their own overconcentration — almost always in catastrophe or specialty lines at a scale far beyond typical F&I products.

Who Retains Obligation

One principle runs through every layer of this chain: the entity transferring risk never escapes its original obligation.

- The primary insurer remains fully responsible to the policyholder regardless of reinsurance

- The reinsurer remains liable to the insurer regardless of retrocession

For dealer-owned programs, this means the A-rated carrier backing the admin obligor structure retains its obligation to the consumer. The dealer's reinsurance company participates in the economics — underwriting profit and investment income — without bearing the consumer-facing regulatory obligation.

Dealer Accessibility

That distinction matters practically. Here's how each layer maps to dealer opportunity:

| Reinsurance | Retrocession | |

|---|---|---|

| Dealer can participate | ✅ Yes — through admin obligor structure | ❌ No — institutional tool only |

| Profit opportunity | ✅ Underwriting profit + investment income | ❌ Not applicable |

| Complexity | Structured with administrator support | Wholesale market requiring regulatory scale |

What Auto Dealers Need to Know

The relevant concept for dealers is reinsurance. Retrocession is useful context, but it's not an opportunity dealers can or should pursue.

When you set up a dealer-owned reinsurance company, you participate at the reinsurance layer: your company reinsures the F&I products written by the primary insurer at your dealership, capturing underwriting profits that third-party providers were keeping. Dealers who move through DealerRE's admin obligor model continue making the same gross profit on each F&I sale — and now also capture what the warranty provider was keeping.

What Backs the Structure

Understanding retrocession clarifies one practical point: your reinsurance program doesn't operate in isolation. The A-rated insurer backing your admin obligor structure provides the financial foundation, layered into the broader insurance market above it.

You don't need to engage at the retrocession level — but knowing that institutional-grade risk architecture sits behind your program matters when evaluating a provider.

DealerRE's admin obligor model is backed by A-rated insurers, which means if your reinsurance company can't meet its obligations, the direct-writing insurance company carries ultimate liability. Your exposure is limited to formation costs and accumulated earnings.

Questions to Ask Any Program Manager

Before committing to a reinsurance program, get clear answers on:

- Who is the backing insurer, and what is their AM Best rating?

- How is risk structured between the primary insurer and the dealer's reinsurance company?

- What is the trust structure for premium reserves?

- How are claims adjudicated, and can you direct service back to your own facility?

Any program worth joining answers these questions without hesitation. Vague or deflected responses are a signal to keep looking.

Frequently Asked Questions

What is the difference between retrocession and reinsurance?

Reinsurance involves a primary insurer transferring risk to a reinsurer. Retrocession involves that reinsurer transferring some of the risk again to another reinsurer, called a retrocessionaire. Both are successive layers in the same risk chain.

What is an example of retrocession in insurance?

A major global reinsurer like Swiss Re purchases catastrophe excess-of-loss retrocession coverage to protect itself when hurricane losses exceed a defined threshold — shielding its balance sheet from outsized natural disaster exposure.

How does retroactive reinsurance work?

Retroactive reinsurance covers losses from events that have already occurred but whose full cost is still unknown — such as long-tail liability claims. It's distinct from prospective reinsurance, which covers future risks, and it's an entirely separate concept from retrocession.

What is a retrocessionaire?

A retrocessionaire is the reinsurance company that accepts risk ceded by another reinsurer in a retrocession agreement. They sit at the far end of the cession chain, receiving risk passed down from both the primary insurer and the first-tier reinsurer.

Can auto dealers own their own reinsurance company?

Yes. Dealers can establish an admin obligor reinsurance company to capture underwriting profits from F&I products including VSCs, GAP, and ancillary coverage. DealerRE specializes in setting up and managing these programs for franchise, independent, and BHPH dealers nationwide.

What are the main types of retrocession?

The four types are proportional (quota share and surplus share), non-proportional (excess-of-loss and stop-loss), facultative (individual risk basis), and treaty (portfolio-wide, automatic coverage). Treaty retrocession is the most commonly used form for standard reinsurance portfolios.