Introduction

Every VSC, GAP policy, and F&I product sold at your dealership is already being reinsured by someone—the only question is whether that someone is you or your third-party provider. For too many dealers, the answer is "someone else," which means hundreds of thousands of dollars in underwriting profits are leaving the building with every contract sold. Both retrospective profit-sharing programs (retro programs) and full dealer-owned reinsurance companies are legitimate ways to stop leaving those profits on the table.

The structure you choose determines how much profit you actually capture, how much risk you carry, and how much long-term wealth you can build from your F&I operation. With F&I gross profit per vehicle retailed reaching $2,505 in Q1 2025—near the all-time high—a mid-volume dealer selling 100 units per month could be forfeiting $1M+ annually in underwriting income to a third-party provider.

This article breaks down both structures and gives you a clear framework for deciding which fits your dealership's volume, risk tolerance, tax goals, and wealth strategy.

Key Takeaways

- Retro programs return a portion of unused F&I reserves to the dealer without forming an insurance company

- Full dealer-owned reinsurance means your dealership owns a company that captures 100% of underwriting profits with significant tax advantages

- Retro programs suit lower-volume dealers seeking low-commitment entry; full reinsurance rewards high-volume dealers with long-term wealth goals

- Neither requires changing your current F&I product lineup

- Your best fit comes down to volume, risk tolerance, tax strategy, and how long you're willing to commit

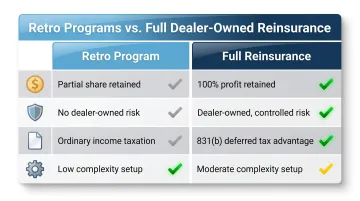

Retro Programs vs. Full Reinsurance: Quick Comparison

Both structures let dealers participate in underwriting profits that would otherwise go to third-party providers. But the mechanics, financial upside, tax treatment, and administrative complexity differ in meaningful ways.

Profit Share

Retro programs return only a portion of unused reserves—typically less than 100%. The administrator keeps a share to cover their risk-bearing, claims management, and administration costs. The exact percentage varies by provider and is not always disclosed transparently.

Full reinsurance gives the dealer access to 100% of underwriting profits after claims are paid. There's no split with an administrator. All profit belongs to the dealer's reinsurance company.

Risk & Downside Exposure

Retro programs carry no financial downside for the dealer if claims exceed expectations. The administrator absorbs the loss. If claims are high, the dealer simply receives no retro check that year. That said, the administrator may adjust future pricing or rates, reducing the dealer's indirect control over program economics.

Full reinsurance makes the dealer's reinsurance company responsible for funding claims. If claims exceed reserves, the reinsurance company's profitability suffers. DealerRE's admin obligor structure is backed by A-rated insurers, which limits the dealer's liability to formation costs and accumulated earnings—not unlimited personal exposure.

Setup, Cost & Control

Retro programs require no new entity formation, no upfront capital investment, and minimal administrative burden. Dealers can sign up quickly with a low learning curve.

Full reinsurance requires establishing a reinsurance company, which involves setup fees, annual maintenance costs (charter renewals, filings, bookkeeping), and disciplined claims management. Working with an experienced partner like DealerRE removes much of this burden—the full-service administration model handles legal forms, filings, tax returns, renewals, and claims adjudication so dealers can stay focused on running their dealership.

Tax Treatment

Retro payouts are taxable income for the dealer in the year received. There are no tax advantages.

Full reinsurance offers notable tax advantages. In properly structured programs—especially admin obligor models—the reinsurance company is typically taxed only on investment income, not underwriting profit. Premium reserves stay inside the company and continue building.

The IRS Section 831(b) election applies to companies with less than $2.9 million in annual premiums and further reduces the tax burden by excluding underwriting income from taxation. For dealers focused on long-term wealth building, that difference compounds quickly.

What is a Retro Program for Auto Dealers?

A retro (retrospective profit-sharing) program is the simplest entry point for dealers who want to participate in underwriting profits without forming their own insurance company. The administrator reinsures F&I products internally, then rebates a pre-agreed percentage of unused reserves back to the selling dealer, on an annual basis.

How the Profit Split Works

The administrator keeps a percentage of reserves to cover program costs, claims management, and their own profit. What's left is the dealer's retro check. The split always falls below 100% of underwriting profits, and many administrators aren't transparent about how that percentage is calculated — so always ask for a full breakdown of deductions before signing.

CNA National Warranty Corp. returned approximately $49 million to dealers in 2018 through its retro and reinsurance participation programs, surpassing $500 million in cumulative distributions. For dealers who qualify and maintain strong loss ratios, those checks add up.

Low-Barrier Entry

Retro programs require:

- No legal entity setup

- No annual charter or filing fees

- No need to understand insurance regulations

- No upfront capital investment

Dealers can usually sign up quickly with minimal learning curve. Retro programs typically require approximately 10 service contracts per month to qualify, making them accessible to smaller-volume stores.

Risk Profile

If claims exceed reserves in a given period, there is no retro payment and the dealer owes nothing. The administrator absorbs the loss. However, the administrator may adjust pricing or rates going forward, which reduces the dealer's indirect control over program economics.

Main Limitation

Because the administrator keeps a cut and the dealer never controls the reserve account, retro participants will always earn less than what a fully reinsured dealer with similar performance would earn. Retro programs also offer no tax advantages — distributions are treated as ordinary income to the dealership.

Use Cases for Retro Programs

Retro programs are best suited for:

- Dealers just entering profit participation—smaller independent or BHPH dealers with monthly F&I contract volumes too low to justify reinsurance company operating costs

- Dealers who want to understand their loss ratios and build a track record before committing to a full reinsurance structure

- Stores looking for a transitional step toward eventual full reinsurance ownership

What is Full Dealer-Owned Reinsurance?

Full dealer-owned reinsurance means the dealer creates and owns their own reinsurance company—often structured as a Controlled Foreign Corporation (CFC), admin obligor company, or Dealer-Owned Warranty Company (DOWC)—that assumes the underwriting risk on F&I products sold at the dealership. Premiums are ceded into the dealer's company, claims are paid from reserves, and remaining profits belong entirely to the dealer.

The Admin Obligor Model

In an admin obligor structure—DealerRE's core offering—the dealer's reinsurance company is the obligor on the contracts but is backed by A-rated insurers. This protects customers and satisfies regulatory requirements while keeping underwriting profits inside the dealer's company.

DealerRE provides full-service administration, including:

- Managing filings, legal forms, tax returns, and renewals

- Claims adjudication

- Compliance monitoring

- Performance reports and financial analysis

- Bookkeeping and financial statements

This allows dealers to focus on running their dealership while DealerRE handles the back-office work.

Financial Upside

The dealer captures:

- 100% of underwriting profits after claims

- Investment income on reserves held inside the company

- Capital flexibility to reinvest in the dealership, real estate, education, or other assets

Successful reinsurance programs are characterized as 10-20+ year strategies. Dealers who exit within 3-4 years rarely capture full benefits, as reserves need time to earn out and compound.

Tax Advantage

Under IRS Section 831(b), qualifying small insurance companies are taxed only on investment income — underwriting profits stay inside the entity, untaxed until distributed. This deferred treatment is one of the most powerful wealth-building levers in a properly structured program.

For 2026, the premium limit is $2.9 million. Dealers exceeding this cap should explore alternative structures such as Super CFC or DOWC models, which offer different tax mechanics but similar wealth-building potential.

Responsibilities and Costs

The financial upside is real — but it comes with overhead that dealers need to plan for. Forming a reinsurance company involves:

- Setup fees

- Annual maintenance costs (charter renewals, filings, bookkeeping)

- Disciplined claims management

Working with an experienced partner like DealerRE removes most of this burden, keeping dealers focused on the dealership rather than the administrative machinery behind it.

Use Cases for Full Dealer-Owned Reinsurance

Full reinsurance is best suited for:

- Franchise dealers, independent dealers, and BHPH operations with consistent monthly F&I production—typically 20-25 contracts per month or more

- Dealers whose long-term goal is building personal and business wealth beyond the dealership floor, using F&I production as the engine

- Stores with clear tax planning goals and a desire to build multi-year wealth inside a company they own

Retro vs. Full Reinsurance: Which Is Right for Your Dealership?

The right choice comes down to four variables: monthly F&I contract volume, risk tolerance, tax planning goals, and how far out you're building. Where your dealership stands on each one points clearly toward one structure or the other.

Volume Threshold Guidance

Retro programs typically require approximately 10 service contracts per month to qualify. Dealers with lower monthly contract volumes may find that the annual costs of running a reinsurance company exceed the profit advantage, making retro the smarter starting point.

Full reinsurance becomes financially viable at approximately 20-25 contracts per month. At higher consistent volume, staying in a retro program means the administrator's profit share compounds against you — and that gap grows fast.

With F&I gross profit per vehicle retailed reaching $2,505 in Q1 2025, the financial stakes are higher than ever. A dealer writing 25 contracts per month at $2,000 each generates $600,000 in annual premium — and the spread between what retro pays out versus what full reinsurance retains in a dealer-owned company can easily exceed $50,000 per year.

Risk and Commitment Consideration

Retro is a no-downside, lower-effort model — good for dealers who want to enter profit participation without operational complexity. If claims exceed reserves, the dealer simply receives no check that year.

Full reinsurance requires accepting that poor claims performance reduces returns. However, it also gives the dealer the ability to control claims experience through better product selection, F&I training, and customer service. Healthy VSC loss ratios range 25-45%, with ancillary product loss ratios often under 20%.

Situational Recommendation Summary

Once volume and risk tolerance are clear, the decision typically resolves itself. Use this as a quick reference:

Choose retro if:

- You're new to profit participation

- Your monthly contract volume is under 20 per month

- You're early in your F&I development

- You want to build a track record before committing to ownership

Choose full reinsurance if:

- Your monthly contract volume exceeds 20-25 contracts

- You have strong F&I production and clear tax planning goals

- You want to build multi-year wealth inside a company you own

- You're committed to a 10+ year strategy

Conclusion

Both retro programs and full dealer-owned reinsurance are legitimate strategies for auto dealers who want to stop giving away underwriting profits to third-party providers. The right choice depends on where you are today — and where you want to be in five years.

Here's a quick way to frame the decision:

- Retro programs — accessible, low-risk entry point for smaller-volume dealers or those new to profit participation

- Full dealer-owned reinsurance — higher-ceiling ownership structure for dealers ready to fully control their profit position and commit to a long-term strategy

The most important first step is knowing your current F&I production numbers and what profit you're leaving on the table. DealerRE offers a dealership analysis that maps your volume, product mix, and goals to the structure that fits — so you're not guessing. Reach out to get started.

Frequently Asked Questions

What is retro reinsurance?

Retro (retrospective) reinsurance in the dealer context is a profit-sharing arrangement where the administrator rebates a portion of unused F&I reserves to the selling dealer after claims are settled, without requiring the dealer to own a reinsurance company. Payments are made annually based on actual loss performance.

What is the difference between retroactive and prospective reinsurance?

Prospective reinsurance—like standard dealer-owned reinsurance programs—covers future risks from newly written contracts. Retroactive reinsurance covers losses from events that have already occurred. Dealer F&I reinsurance programs are prospective, meaning they apply to contracts sold going forward.

What is retrospective rating in insurance?

Retrospective rating adjusts the dealer's premium or profit share based on actual claims experience during a policy period. Dealers with low loss ratios earn more in retro-style arrangements because fewer claims mean more unused reserves available for distribution.

What are the 4 types of reinsurance?

The four main types—facultative, treaty, proportional, and non-proportional—are defined by the Insurance Information Institute. Treaty and facultative describe how reinsurance is placed; proportional and non-proportional describe how risk is shared. Most dealer F&I reinsurance programs use treaty reinsurance with proportional risk-sharing.

What is the difference between reinsurance and retrocession?

Reinsurance is when an insurer transfers risk to another company. Retrocession is when a reinsurer itself purchases reinsurance from another reinsurer (called a retrocessionaire). For dealers, this distinction has no practical effect on how profit participation programs are structured or paid out.

Who insures retrocession?

Retrocession coverage is provided by other reinsurance companies or specialized retrocessionaires. In dealer-owned admin obligor reinsurance programs like DealerRE's, the dealer's company is backed by A-rated insurers, which provides consumer protection and financial stability—dealers don't need to engage with retrocession at any level.