Introduction

More auto dealers are moving away from third-party F&I product providers—and keeping those underwriting profits in-house. Two structures lead that shift: the 831(b) captive insurance company and the Dealer-Owned Warranty Company (DOWC). Both let dealers capture profits from vehicle service contracts, GAP coverage, and other F&I products, but they differ sharply in tax treatment, regulatory requirements, operational demands, and long-term flexibility.

Pick the wrong one and you risk IRS scrutiny, exit complications, or operational burdens your team isn't equipped to handle. Pick the right one and you build a structure that fits your volume, your staff, and your long-term financial goals.

Understanding these differences matters because the stakes are high: with F&I gross profit averaging $2,534 per vehicle retailed in Q3 2025 among publicly traded auto retail groups, dealers leaving profits on the table are funding someone else's bottom line—not their own.

Key Takeaways

- 831(b) captives exclude up to $2.85M in underwriting profits from taxable income annually, with turnkey TPA administration

- DOWCs are dealer-owned C-Corps that act as direct obligors on VSCs — more control, but higher capital and compliance demands

- 831(b) captives fit most dealers — lower startup risk, proven compliance, and broader product eligibility

- DOWCs make sense for high-volume groups already past the 831(b) threshold with dedicated insurance staff in place

- Both structures beat third-party providers, but choosing the wrong one for your volume and experience level can cost more than it saves

What Is an 831(b) Captive Insurance Company for Auto Dealers?

An 831(b) captive insurance company is a small, dealer-owned insurance entity that elects under IRS Section 831(b) to exclude net written premiums from taxable income—up to the annual premium cap. For tax years beginning in 2025, that cap is $2.85 million; for 2026, it rises to $2.9 million, indexed annually in $50,000 increments.

Under this election, the captive is taxed only on investment income, not underwriting profit. Premiums collected, minus claims and expenses, accumulate tax-advantaged inside the company. Shareholders are not taxed until distributions are declared, creating a powerful wealth-building vehicle alongside dealership operations.

How the Admin Obligor Structure Works

In the auto dealer F&I context, the 831(b) captive typically functions as a Controlled Foreign Corporation (CFC)—often domiciled in jurisdictions like Turks and Caicos—that reinsures F&I products backed by A-rated fronting insurers. The dealer's captive acts as the reinsurance entity behind the products, capturing underwriting profits without bearing unlimited risk.

Here's how it works in practice:

- A fronting insurer (A-rated) acts as the primary obligor on the F&I product

- The dealer's CFC reinsures the risk from the fronting insurer via a reinsurance agreement

- A Third-Party Administrator (TPA) manages claims adjudication, fraud protection, and compliance

- The CFC uses first-dollar loss insurance (stop-loss coverage) to limit catastrophic exposure

- Premiums flow into the captive, claims are paid, and underwriting profit stays with the dealer

This structure has been the industry standard since the early 1990s. Professional administrators handle legal filings, tax returns, compliance, claims, and investment oversight — dealers stay focused on selling cars.

Core Tax Advantages

The 831(b) election delivers three compounding tax advantages:

| Advantage | How It Works |

|---|---|

| Permanent income exclusion | Underwriting profit is excluded from taxable income permanently — not deferred — as long as premiums stay below the annual cap |

| Tax-advantaged growth | Investment income grows inside the captive and is taxed at the entity level; distributions can be timed strategically |

| No double taxation | Shareholders owe nothing on underwriting profits until distributions are declared, freeing capital for reinvestment |

Product Flexibility: Insurance and Non-Insurance

The 831(b) captive expands product eligibility beyond what a DOWC allows. The CFC structure can reinsure both insurance and non-insurance F&I products, including:

- Vehicle Service Contracts (VSCs)

- Guaranteed Asset Protection (GAP)

- Credit life insurance

- Collateral Protection Insurance (CPI)

- Ancillary products (tire & wheel, door ding, windshield repair)

This flexibility allows dealers to partner with specialty F&I providers and offer a broader product menu than DOWCs, which are restricted to non-insurance products only.

Capital and Setup Requirements

The CFC structure requires minimal initial capital—far less than the $50,000 to $500,000 typically required for DOWCs. Setup takes weeks, not months, and the structure offers portability: dealers can change administrators without losing ownership rights.

Full-service administration covers:

- Legal filings and entity formation

- Tax preparation and IRS compliance

- Claims adjudication and fraud protection

- Investment management and performance reporting

- Regulatory filings and license renewals

- Bookkeeping and financial statements

This full-service model works for a wide range of dealer sizes — from independent operators to mid-size franchise groups. DealerRE has structured and administered these programs for over 400 dealerships nationwide since 1994, managing all legal, tax, and compliance requirements so dealers can focus on what they do best.

Use Cases for 831(b) Captives

Ideal dealer profiles:

- Independent dealers producing under the $2.85 million premium cap

- Franchise dealers seeking to replace third-party F&I profits

- BHPH operators wanting to capture warranty and CPI underwriting profits

- Dealers new to reinsurance who want professional administration

- Dealers selling more than 30 cars per month (DealerRE's typical client threshold)

The IRS Regulatory Landscape: Recent Court Rulings

For years, 831(b) captives faced heightened IRS scrutiny following Notice 2016-66, which identified certain micro-captive transactions as "transactions of interest" requiring Form 8886 disclosure.

January 2025 brought a significant shift, when the IRS issued Final Regulations (TD 10029) defining two categories:

- Listed transactions: Require BOTH a "financing factor" AND a loss ratio below 30% of earned premiums

- Transactions of interest: Require a financing factor OR a loss ratio between 30% and 60%

In April 2026, Drake Plastics v. IRS pushed the landscape further. A federal court vacated (overturned) the "listed transaction" designation for properly structured 831(b) captives, finding that the IRS exceeded its statutory authority. The "transaction of interest" classification remained, but the most punitive regulatory label was gone.

Auto dealers have a specific advantage worth knowing. The final regulations explicitly exclude "Seller's Captives" from being treated as listed transactions — and "seller" is defined to include automobile dealers. If the captive insures or reinsures at least 95% third-party risk (customer risks unrelated to the dealership), no Form 8886 disclosure is required.

For dealers running properly structured programs, the regulatory picture is now materially clearer than it was even two years ago. That clarity is only useful, however, if the underlying structure holds up — which is where program design and qualified administration become the deciding factor.

What Is a Dealer-Owned Warranty Company (DOWC)?

A DOWC is a domestic C-Corporation established by the dealer to act as the obligor on non-insurance F&I products—primarily vehicle service contracts. Unlike the 831(b) CFC, the DOWC does not require a third-party fronting insurer; it acts as the direct provider of the warranty or service contract.

The DOWC qualifies as an insurance company for federal income tax purposes (filing Form 1120-PC) but is not regulated as one at the state level. This structure has existed since the 1970s and is the only domestic model to accomplish something similar to a CFC.

Tax Structure: Retail-Cost Accounting and NOL Carryforwards

DOWCs use retail-cost accounting, which recognizes the full retail cost of the VSC as premium. Acquisition costs—dealer commissions and administrative fees—are deductible in the year incurred for federal tax purposes, even though premium income is amortized over the policy life for financial reporting.

Under IRC Section 832(b)(4), 20% of the unearned premium reserve must be added back into taxable income. Because commissions and fees are written off upfront, the DOWC typically generates a large Net Operating Loss (NOL) carryforward, resulting in tax deferral for the first 5 to 10 years. This method has been reviewed in IRS audits and allowed with no changes.

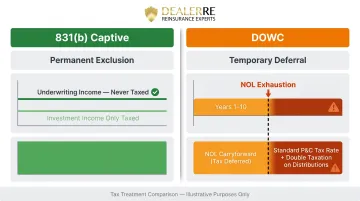

That deferral is the critical difference from the 831(b) captive. The 831(b) offers permanent exclusion of underwriting income; the DOWC offers temporary deferral. Once the NOL is exhausted, DOWC earnings face standard P&C taxation—and eventual double taxation when distributions reach shareholders.

Operational Demands: Hands-On, Labor-Intensive

A DOWC carries the full operational footprint of a standalone insurance company. It requires:

- Separate operating statements and P&Ls

- Reserve management and statutory accounting

- Investment strategy oversight

- IRS audit readiness (capital gains statements, claims reports, retail accounting P&Ls)

- Service contract provider licensing (potentially in multiple states)

Setup typically involves high fees and takes months rather than weeks—considerably longer than CFC formation.

Key Limitations

- Product restrictions: DOWCs cover non-insurance products only — no GAP, credit life, or any product regulated as insurance. This limits product menu flexibility and specialty partner options.

- Higher capital requirements: Initial capitalization ranges from $50,000 to $500,000 depending on domicile; Florida requires the full $500,000.

- Greater regulatory complexity: Retail-cost accounting has survived IRS audits, but the standalone warranty company structure carries more compliance overhead and audit exposure than a CFC.

- Difficult exits: More than 50% of dealers who adopt a DOWC change course within 12 months. Running off existing contracts can take years, and administrator recapture offers often come at a steep discount.

Use Cases for DOWCs

Ideal dealer profile:

- Large dealer groups producing significantly above $2.85 million in annual ceded premiums

- Experienced operators with insurance management expertise on staff

- Dealers willing to operate a standalone warranty company with full audit readiness

- Groups prepared to accept limited product scope and heavier regulatory demands in exchange for direct control over cash flow and investment decisions

For most independent and mid-size franchise dealers, the operational complexity and limited product flexibility outweigh those control advantages — which is where an 831(b) captive structure tends to be the more practical fit.

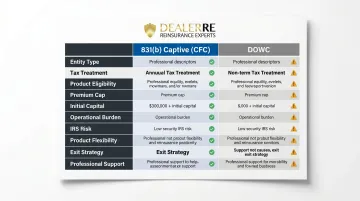

831(b) Captive vs DOWC: Side-by-Side Comparison

| Dimension | 831(b) Captive (CFC) | DOWC |

|---|---|---|

| Entity Type | Controlled Foreign Corporation (often offshore) | Domestic C-Corporation |

| Tax Treatment | Permanent exclusion of underwriting income; only investment income taxed | Temporary NOL deferral (5–10 years), then standard P&C taxation + double taxation on distributions |

| Annual Premium Cap | $2.85M (2025); $2.9M (2026) | No cap |

| Product Eligibility | Insurance AND non-insurance products (VSCs, GAP, credit life, CPI, ancillary) | Non-insurance products only (VSCs, maintenance plans) |

| Initial Capital | Minimal (often under $50K) | $50K–$500K (Florida requires $500K) |

| Operational Burden | TPA handles compliance, claims, filings, investments | Dealer operates standalone warranty company; high staff demands |

| IRS/Regulatory Risk | Clearer path post-Drake Plastics ruling; seller's captive exclusion available | Greater scrutiny; retail-cost accounting requires audit readiness |

| Product Flexibility | Broad; supports all major F&I products | Limited; excludes insurance products |

| Exit Strategy | Portable; no exit strategy issues; clear transition path | Difficult; contract run-off required; often costly or unclear |

| Professional Support | Full-service TPA administration | Dealer self-administers or hires separate support |

Tax Treatment: Long-Term vs. Temporary Advantage

The 831(b) captive provides a permanent tax advantage on underwriting income for the life of the entity, as long as premiums stay below the annual cap. Investment income is taxed, but underwriting profit accumulates tax-free inside the captive until distributions are declared.

The DOWC provides temporary tax deferral through NOL carryforwards for 5–10 years. Once the NOL is exhausted, underwriting income is taxed at standard P&C rates. Distributions to shareholders are taxed again, creating a double-taxation scenario. That distinction — permanent exclusion vs. temporary deferral — is the core reason most dealers find the 831(b) structure more advantageous over a 10-to-20-year horizon.

Operational Complexity: TPA vs. Self-Administration

831(b) captives administered through a professional TPA give dealers turnkey support — the administrator handles claims adjudication, regulatory filings, tax returns, investment management, and performance reporting.

DOWCs place that burden directly on the dealer. Operating one means managing:

- Reserve statements and investment accounts

- IRS audit preparedness and documentation

- Dedicated internal staff with insurance expertise

- Ongoing compliance tracking without administrator support

Exit Strategy and Portability

831(b) CFC structures are generally portable and allow dealers to transition formations without losing ownership rights. Exit strategies are clear, and the captive can even serve as a financing tool in buy-sell transactions.

DOWCs create ownership complications when transitioning mid-program. Running off contracts can take years, and administrators often seek significant discounts on recapture offers. If a DOWC shares majority common ownership with an 831(b) CFC, the CFC will likely lose its 831(b) eligibility, creating adverse tax consequences.

IRS Scrutiny and Compliance Risk

The April 2026 Drake Plastics ruling reduced stigma around 831(b) captives and clarified the seller's captive exclusion path. DOWCs, by contrast, still draw greater IRS scrutiny — particularly around retail-cost accounting methods and the operational standards expected of a standalone warranty company.

Both structures require proper documentation. The difference is consequence: a documentation gap in a DOWC can trigger a full restatement of deferred income, while a well-administered 831(b) captive has a clearer compliance roadmap post-Drake Plastics.

Which Reinsurance Structure Fits Your Dealership?

Choose an 831(b) Captive (CFC Structure) If You:

- Produce under $2.85 million in annual ceded premiums

- Want access to both insurance and non-insurance F&I products

- Prefer professional TPA management of compliance, claims, and investments

- Are new to dealer participation programs

- Want a proven structure with a clear exit strategy and portability

- Sell more than 30 cars per month and want to replace third-party F&I profits

- Value low startup risk and turnkey administration

Consider a DOWC If You:

- Are a high-volume dealer group producing significantly above the 831(b) threshold

- Have experienced insurance management on staff

- Are comfortable operating a standalone warranty company with full audit readiness

- Are willing to accept limited product scope (non-insurance only)

- Prefer direct control of cash flow and investments despite greater regulatory demands

- Have dedicated staff capable of managing reserve statements, compliance, and IRS audit preparedness

DealerRE: Turnkey 831(b) Captive Administration

Once you've identified the right structure, execution matters. For dealers pursuing the 831(b) captive route, DealerRE handles all legal filings, tax returns, compliance, claims adjudication, and investment oversight—so you stay focused on selling cars and building wealth through your reinsurance company.

With 28 years of experience and more than 400 dealers served nationwide, DealerRE offers:

- Fast company setup (weeks, not months)

- Structured onboarding and training programs for your staff

- Expert dealership analysis for maximum profitability

- Ongoing performance reporting and optimization

- Full compliance with IRS Code 831(b) and seller's captive exclusion

- No hidden fees or costs

Schedule a consultation to find out which structure fits your dealership's volume and goals.

Conclusion

Neither structure is universally superior—the right choice depends on several factors:

- Premium volume: Higher volume dealers typically benefit more from the 831(b) captive's tax treatment

- Staff capacity: DOWCs demand more internal administrative involvement

- Risk tolerance: Captives offer stronger liability separation for most dealers

- Long-term goals: If investment growth and profit retention are priorities, the captive structure wins on flexibility

For most independent and franchise dealers, the 831(b) captive offers the right balance of tax efficiency, product flexibility, professional support, and proven compliance history.

The regulatory environment around captive insurance continues to evolve, making it worth exploring these structures now—but only with qualified guidance from an experienced reinsurance partner like DealerRE to avoid costly formation mistakes.

Whether you choose a CFC or a DOWC, both structures beat relying on third-party providers. Getting the structure right from the start is what separates dealers who consistently retain underwriting profits from those who leave money on the table year after year.

Frequently Asked Questions

What is 831(b) captive insurance?

An 831(b) captive is a small, dealer-owned insurance company that elects under IRS Section 831(b) to exclude net written premiums from taxable income up to the annual cap ($2.85 million for 2025). The captive is taxed only on investment income, allowing underwriting profits to accumulate tax-advantaged inside the company.

What is a dealer-owned warranty company (DOWC)?

A DOWC is a domestic C-Corp that serves as the obligor on non-insurance F&I products like vehicle service contracts. It gives the dealer direct control over warranty profits and cash flow, but comes with full administrative, compliance, and operational responsibilities.

What is the 831(b) threshold?

The 831(b) annual premium cap is $2.85 million for 2025 (rising to $2.9 million in 2026), indexed annually for inflation. Premiums written below this cap are excluded from the captive's taxable income entirely.

What is the difference between captive insurance and regular insurance?

Traditional insurance involves paying premiums to a third-party insurer who retains the underwriting profit. Captive insurance allows the business owner (the dealer) to own the insurer—so underwriting profits, investment income, and claims savings stay within the dealer's own company instead of going to an outside provider.

What is the point of a captive insurer?

Captive insurers let dealers keep profits that would otherwise flow to third-party F&I providers. They also give dealers control over claims experience, access to investment income on reserves, and a tax-advantaged structure for building long-term wealth.

What are the two major types of captive insurance companies?

The two primary types are pure captives (owned by a single dealer to insure its own risks) and group captives (owned by multiple businesses sharing risk collectively). In the dealer space, both the 831(b) captive and the DOWC are pure captive structures — but they differ significantly in tax treatment and operational setup.