Introduction

Most dealers know they're leaving money on the table by paying third-party providers. The harder question is which structure actually solves that problem — and which one creates new ones.

A Dealer Owned Warranty Company (DOWC) and a Producer Owned Reinsurance Company (PORC) both promise to keep F&I profits inside the dealership. The mechanics, risks, and economics, however, differ significantly.

This decision carries lasting consequences. The structure a dealer chooses affects:

- How premiums are taxed

- Which F&I products qualify for inclusion

- How much capital is required upfront

- What regulatory obligations the dealer takes on

- How much operational control the dealer actually retains

Choosing the wrong structure can lock a dealership into a more expensive, less flexible arrangement for years — or create tax exposure that nobody flagged during the sales pitch. This guide breaks down both options so you can make an informed call.

TLDR

- DOWCs act as the obligor on service contracts and defer federal income tax for 7–10 years, but that liability doesn't disappear — it comes due later

- PORCs can qualify for the IRC 831(b) exemption on up to $2.85M in annual premiums, making underwriting profit tax-exempt rather than deferred

- DOWCs cannot include GAP or credit life; PORCs support the full F&I menu — a critical difference for most dealers

- Neither structure is universally superior — the right choice depends on premium volume, product mix, tax timeline, and administrative capacity

DOWC vs PORC: Quick Comparison

| Factor | DOWC | PORC |

|---|---|---|

| Structure type | Domestic C-corporation; service contract obligor | Reinsurance company (onshore or offshore) |

| Tax treatment | Deferral only — taxes due in 5–10 years as reserves unwind | IRC 831(b) exemption; no tax on underwriting profit up to $2.85M |

| Product scope | VSCs and non-insurance ancillary plans only | Full F&I suite: VSCs, GAP, credit life, ancillaries |

| Upfront capital | $50K–$500K+ depending on state; ongoing state filings required | Lower capital; simpler setup; fewer regulatory hurdles |

| Complexity | High — state compliance, lender form filings, financial statements; difficult to wind down | Lower — especially with an experienced administrator; more portable |

| Best for | Large dealer groups with internal compliance resources | Independent, mid-sized, and BHPH dealers seeking tax efficiency |

If your dealership has the infrastructure to manage ongoing state compliance, a DOWC can work — but most independent and mid-sized dealers will find a PORC delivers more flexibility and a stronger tax position from day one.

What is a DOWC?

A Dealer Owned Warranty Company is a C-corporation formed to act as the obligor (the entity legally responsible for paying claims) on vehicle service contracts and certain non-insurance F&I products. While not regulated as an insurance company at the state level, a DOWC is treated as a property and casualty insurer for federal income tax purposes under IRC §§ 831 and 832.

How a DOWC Captures Profit

In a traditional F&I model, the dealer sells a vehicle service contract and the underwriting profit flows to the third-party warranty provider. When a dealer forms a DOWC, that entity becomes the provider. Underwriting profit and investment income stay with the dealer's company instead of leaving the dealership entirely.

Tax Mechanics: Deferral, Not Exemption

A DOWC files as a property and casualty insurance company (Form 1120-PC). Gross premiums are recognized over the contract term, while acquisition costs and administrative expenses are deducted when incurred. The unearned premium reserve is subject to a 20% add-back under IRC § 832(b)(4), which caps the full deferral benefit.

The net result is tax deferral, typically lasting 7–10 years. This is not tax elimination. The deferral unwinds on a predictable schedule:

- Premiums are recognized gradually as contracts mature

- Unearned premium reserves decline over the contract term

- Deferred income becomes taxable as reserves run off

- Pro formas projecting zero taxes for a decade, without disclosing the back-end liability, are incomplete

Dealers must plan for this eventual tax obligation before committing to the structure.

Product Limitations

DOWCs are restricted to non-insurance products. Vehicle service contracts and certain ancillary plans qualify, but coverage categories that most dealers want to include do not:

- GAP and credit life are classified as insurance in most states

- These products must be issued by licensed insurers or reinsurers

- A DOWC cannot include them, forcing dealers to maintain separate structures or rely on third parties

That product gap fragments a dealer's F&I program and is one of the DOWC's most practical limitations.

Controlled-Group Risk

If a dealer owns both a DOWC and a PORC that qualifies for IRC 831(b), and the two entities share majority common ownership, the PORC may lose its ability to make the 831(b) election. This stems from related-party aggregation rules under IRC §§ 267(b) and 707(b). The IRS treats related policyholders as one for diversification purposes, which can disqualify the PORC from 831(b) eligibility, resulting in adverse tax outcomes. Dealers considering both structures should consult a reinsurance advisor before proceeding.

Use Cases of a DOWC

A Dealer-Owned Warranty Company works best when a dealership already has the volume and internal resources to absorb the administrative overhead it requires. The structure offers maximum control — but that control comes with real compliance responsibilities.

Best-fit dealers include:

- Large franchise groups or multi-rooftop dealer groups selling high VSC volume

- Dealers with in-house legal and accounting support capable of handling state filings and licensing

- Operations with established internal infrastructure for claims management and contract administration

Products that align well with a DOWC:

- Vehicle service contracts (VSCs), where the dealer wants direct control over pricing and contract design

- Non-insurance ancillary plans (tire & wheel, door ding, windshield) where the dealer prefers to keep claims processing domestic rather than routing profits through an offshore reinsurance company

For dealers who meet these criteria, a DOWC can deliver strong underwriting profit retention and operational flexibility. Dealers who don't yet have this infrastructure often find a PORC structure easier to manage without sacrificing meaningful upside.

What is a PORC?

A Producer Owned Reinsurance Company (PORC) is a reinsurance entity that assumes insurance risk from a licensed front-line insurer. It goes by several names — ARC, CFC, DORC, or PARC — depending on the administrator and structure.

PORCs can be domiciled offshore (such as Turks and Caicos) or onshore (such as through the Delaware Tribe of Indians). In either case, the entity files as a U.S. taxpayer and holds reserves in U.S. bank accounts.

The 831(b) Tax Advantage

When annual written premiums fall below the IRS threshold — currently $2.85 million for 2025 — a PORC can elect IRC 831(b) status. Under this election, the company pays income tax only on investment income, not on underwriting profit. This is a tax exemption, not a deferral. Dealers at or below this premium cap keep significantly more after-tax profit than they would in a DOWC.

Product Breadth

Unlike DOWCs, PORCs can reinsure both insurance and non-insurance F&I products under the same structure. That includes:

- GAP

- Credit life

- Vehicle service contracts

- Appearance protection

- Tire and wheel

- Other ancillary plans

For dealers who rely on GAP as a significant revenue driver, this product flexibility alone makes the PORC the stronger choice.

Investment Income and Distribution Advantages

Underwriting profit held in trust earns investment income. When the dealer-owner takes a distribution, it's generally taxed as a qualified dividend at the long-term capital gains rate — 0%, 15%, or 20% depending on income level — rather than at ordinary income rates.

Dealers can also defer distributions entirely, giving them direct control over when they recognize that income for tax purposes.

Admin Obligor Structure and DealerRE's Approach

Those PORC advantages — tax efficiency, product breadth, and favorable distribution treatment — are most valuable when the structure itself is sound. DealerRE specializes in admin obligor reinsurance, a PORC model backed by A-rated insurers where the reinsurance company itself is insured.

This reduces dealer exposure while still capturing 100% of underwriting profits. The result is the profit potential of full reinsurance with the security of carrier backing — a structure that works for independent dealers and BHPH operations, not just franchise groups.

Use Cases of a PORC

A PORC works best for dealers who want to capture underwriting profits across their entire F&I product mix without taking on the regulatory complexity or capital requirements of a DOWC.

Dealers who fit this structure well:

- Growth-stage independents building out their F&I program for the first time

- Established franchise dealers looking for tax-advantaged profit retention at scale

- BHPH operators who need flexible product coverage tied to their customer base

- Dealer groups that want a single structure covering multiple rooftops

Products a PORC can cover:

- Vehicle service contracts (VSCs)

- GAP and credit life

- Appearance protection, tire and wheel, and windshield plans

- Ancillary products across the full F&I suite

That product breadth is a real advantage. A DOWC's structure limits which products can run through it — a PORC carries no such restriction, meaning dealers don't have to run parallel structures to capture profit on every product they sell.

DOWC vs PORC: Which Structure Fits Your Dealership?

The right structure depends on five key variables:

- Premium volume relative to the 831(b) threshold

- Product mix (especially whether GAP is a significant revenue item)

- Tax situation and timeline

- Available capital for setup

- Administrative capacity

Each variable carries a different weight depending on your dealership's size and product strategy. The two decision points below tend to be the most determinative.

When 831(b) Eligibility Favors the PORC

If your annual written premiums fall within the 831(b) limit ($2.85M for 2025), a PORC offers a significantly better tax outcome than a DOWC—full exemption versus eventual liability. Dealers at or above that threshold should model both structures before committing to either.

When Your Product Mix Rules Out the DOWC

If your F&I menu includes GAP or credit life as significant revenue drivers, a DOWC is immediately the inferior choice—those products cannot be included. A PORC supports the full product stack.

Choose a DOWC if:

- You are a large dealer group with dedicated internal compliance resources

- You have a strong preference for a domestic entity

- You are comfortable with the long-term tax liability and have modeled the deferral reversal

- You do not rely heavily on GAP or insurance products

- You have explored whether the controlled-group issue with any existing PORC will be triggered

Choose a PORC if:

- You want a simpler, lower-capital path to capturing underwriting profit

- You need to include insurance products in the program

- You are a small, mid-sized, or independent dealer who would benefit from 831(b) tax exemption

- You want a portable, scalable structure that an experienced administrator can manage end-to-end

DealerRE has helped dealers across both structures since 1994—and can model which path makes sense for your specific volume, product mix, and tax situation before you commit.

Common Pitfalls Dealers Should Watch Out For

The "Ownership" Misconception

Many dealers assume a DOWC gives them more control than a PORC. Control over administration, claims decisions, and investment management is determined by the administrator and the agreement terms—not the structure label. Whatever structure you choose, push for the same contractual involvement in each of those areas before signing.

Tax Deferral Is Not Tax Elimination

A DOWC pro forma that shows no taxes for 7–10 years without disclosing the eventual tax bill is incomplete. As unearned premium reserves run off, deferred income becomes taxable. Ask any DOWC provider to show a full lifecycle tax projection, including what happens when deferred liabilities come due.

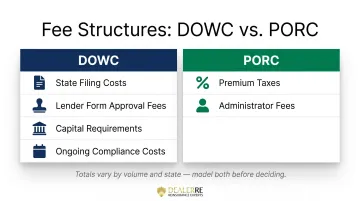

The Hidden Fee Problem

Both DOWCs and PORCs carry fees, but the types differ. Before selecting a structure, request a complete, itemized fee comparison. Common costs to compare include:

- DOWCs: State filing costs, lender form approval fees, capital requirements, and higher ongoing compliance costs

- PORCs: Premium taxes and administrator fees

The totals can vary significantly depending on volume and state, so running the numbers side by side is essential.

Frequently Asked Questions

What are the alternatives to DOWC?

Alternatives include PORC/ARC structures (reinsurance-based), NCFC programs for high-volume dealers, and retrospective (retro) profit-sharing arrangements for dealers not yet ready to form their own company. Each offers different levels of control, tax benefit, and product eligibility.

Do dealerships make money on warranties?

In a traditional model, most warranty profit goes to the third-party provider. When a dealer establishes a DOWC or PORC, they capture the underwriting profit and investment income directly. That's why structure choice determines how much the dealer actually keeps.

What is a reinsurance structure?

A reinsurance structure is an arrangement where a dealer's own company assumes insurance risk from a front-line carrier, retaining underwriting profits instead of surrendering them to a third party. The PORC is the most common dealer reinsurance structure.

What are the 4 functions of reinsurance?

The four standard functions are: (1) risk transfer from the insurer to the reinsurer, (2) stabilization of underwriting results, (3) capacity expansion for the fronting insurer, and (4) profit participation for the dealer-owner. In the dealer context, profit capture is the primary driver.

Which structure is better for a small or mid-sized independent dealer?

For most small to mid-sized dealers, a PORC is the more accessible and tax-efficient choice. Lower upfront capital, broader product eligibility, and 831(b) exemption potential give it an edge. The DOWC is better suited to large dealer groups with the infrastructure to support it.

Can a DOWC and a PORC be owned by the same dealer?

This is possible but carries serious risk: if both entities share majority common ownership, the PORC may lose its ability to qualify for the IRC 831(b) election, resulting in adverse tax outcomes. Dealers considering both structures should consult with a knowledgeable reinsurance advisor before proceeding.