Introduction

Every F&I product sold in your dealership carries a profit margin — and in traditional third-party arrangements, the majority of that margin goes to warranty companies, administrators, and insurers, not to the dealer who made the sale. Dealers who rely on these providers are leaving substantial underwriting profit on the table.

The right participation structure — whether a PORC (Producer Owned Reinsurance Company), DOWC (Dealer Owned Warranty Company), or Captive Insurance Company — changes that equation by allowing dealers to recapture those profits. All three share a common goal: enabling dealers to participate in underwriting results rather than handing profits to third parties. But they work very differently, and the distinctions matter.

Choosing the wrong structure has real consequences — unexpected tax liabilities, compliance burdens you weren't prepared for, limited product flexibility, or a mismatch with your dealership's volume and goals. Choosing the right one puts underwriting profits back in your pocket and gives you lasting control over your F&I program.

This article provides a plain-language breakdown of each structure, a side-by-side comparison, and situational guidance to help you identify which approach fits your dealership.

Key Takeaways

- A PORC lets dealers retain 100% of underwriting profit and investment income with potential IRC 831(b) tax treatment — lowest barrier to entry.

- A DOWC bypasses the insurance framework entirely, issuing VSCs directly as a service contract obligor and deferring taxes for several years.

- Captives offer the most control and customization but require the highest capital commitment and ongoing regulatory compliance.

- All three capture underwriting results; differences lie in regulatory classification, tax treatment, capital needs, and administrative complexity.

- The right choice depends on annual F&I premium volume, capital availability, risk appetite, and tax strategy.

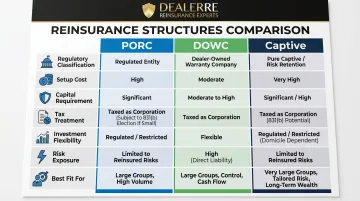

PORC vs DOWC vs Captive: At-a-Glance Comparison

| Factor | PORC | DOWC | Captive |

|---|---|---|---|

| Regulatory Classification | Reinsurance company (insurance entity) | Service contract obligor (not insurance) | Licensed insurance company |

| Setup Cost | Low-to-moderate | Moderate-to-high | Highest |

| Capital Requirement | Lower; varies by structure | $50K–$500K initial; state-dependent | Highest; varies by domicile |

| Tax Treatment | Investment income only taxed if under 831(b) premium cap | Tax deferral only (taxes due later) | Full insurance tax treatment |

| Investment Flexibility | Trust (conservative) + flexible surplus | Claims reserves restricted; surplus flexible | Reserves restricted; surplus flexible |

| Risk Exposure | Full risk of loss assumed | First-dollar claims exposure | Full insurance risk assumed |

| Products Eligible | VSC, GAP, ancillary F&I products | VSC and select ancillary (not GAP) | VSC, GAP, CPI, ancillary |

| Best Fit For | Independent/BHPH dealers seeking tax efficiency | Dealers wanting direct product control | Large groups needing bespoke coverage |

What is a PORC?

A PORC (Producer Owned Reinsurance Company) is a reinsurance entity that assumes insurance risk ceded from a fronting carrier, allowing dealers to capture underwriting profits that would otherwise flow to third-party warranty and insurance providers. PORCs can be domiciled offshore (such as Turks & Caicos) or domestically.

In modern regulatory terminology, these entities are often called PARCs (Producer Affiliated Reinsurance Companies) or ARCs (Affiliated Reinsurance Companies) — the IRS language for Controlled Foreign Corporations (CFCs) under IRC Section 953(d).

In practice, a dealer's F&I products — VSCs, GAP, and ancillary offerings — are backed by a fronting insurer that issues a CLIP (Contractual Liability Insurance Policy), then cedes the risk and corresponding premiums to the dealer's PORC, which retains the underwriting profit. Two CLIP structures exist:

- First-Dollar CLIP: Covers all contract performance obligations from dollar one, transferring full risk to the insurer at a higher premium cost

- Failure-to-Perform CLIP: Covers only obligor default or insolvency — the more common structure in dealer programs due to lower cost

The PORC assumes ceded risks under either arrangement.

Key financial benefits include:

- 100% participation in underwriting results

- Investment income on trust assets and surplus

- Potential tax advantages under the IRC 831(b) election, available to small insurance companies with annual premiums under $2,900,000 for 2026 — only investment income is taxed, not underwriting income

DealerRE specializes in admin obligor PORC programs where an administrator acts as the obligor, providing an additional layer of protection for the dealer's reinsurance company, which is backed by A-rated insurers.

Common misconceptions include:

- PORC does not mean offshore only — domestic PORCs exist

- Funds do not "go offshore"; they remain in U.S. bank accounts even when the entity is domiciled abroad

- A CLIP fee does not eliminate the reinsurer's liability — the PORC still bears full risk of loss

- Premium rates must be actuarially justified, not inflated

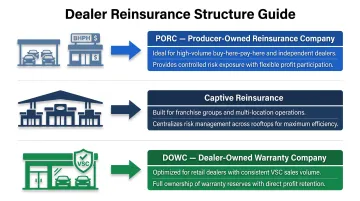

Use Cases for PORC

Best suited for:

- Independent dealers

- BHPH dealers

- Small-to-mid-size franchise dealers with consistent F&I product volume

- Dealers replacing third-party VSC and ancillary providers

- Multi-rooftop groups consolidating risk across locations under one reinsurance entity

What is a DOWC?

A DOWC (Dealer Owned Warranty Company) is a service contract obligor company — not an insurance company — licensed in each state where it issues vehicle service contracts directly to consumers. Unlike a PORC, a DOWC does not assume or transfer insurance risk. It issues contractual service obligations and stands first in line for all VSC claims. A Failure-to-Perform CLIP (FTP CLIP) purchased from a licensed insurer serves as a financial backstop, activating only in the event of the DOWC's insolvency.

That mechanical structure is straightforward — the tax treatment is where dealers routinely get surprised. DOWCs do not eliminate taxes; they defer them. Unearned premium reserves aren't immediately taxable, creating a deferral window of 7–10 years in typical proformas.

The tax liability accumulates the entire time. Many proformas show years of tax-free operation without clearly modeling the eventual bill. Shutting down a DOWC close to when that liability becomes due can draw significant IRS scrutiny.

Setup and ongoing costs:

- Initial capital requirements: approximately $50,000 to $500,000 depending on state

- State VSC provider licensing required in each operating state, with associated form filing costs per product, per lender, per state

- Annual administrative costs (financial statements, tax returns, state filings) typically higher than reinsurance

- DOWCs are difficult to exit — some administrators require exclusivity agreements, term commitments, or run-off fees

What DOWCs cannot do:

- Issue GAP products or limited warranties (insurance products)

- Legally transfer risk in the manner an insurance company does — arrangements with insurance attributes may be deemed insurance by state regulators, triggering penalties, fines, and premium tax exposure

Use Cases for DOWC

Best suited for:

- Dealers wanting direct control over service contract product offerings and terms

- Dealers willing to manage state licensing requirements

- Dealerships with the initial capital to meet obligations

- Larger dealer groups or those wanting access to unearned reserves

Before committing, build a full proforma that models both the deferred tax accumulation and a realistic exit — including what run-off obligations and administrator fees look like in years 8–12.

What is Captive Insurance?

A captive insurance company is a licensed, regulated entity owned and controlled by its insureds — in the dealer context, the dealership or dealer group. Unlike a PORC (which reinsures a fronting carrier) or a DOWC (a service contract company), captives are fully licensed insurance companies with broader authority and higher regulatory accountability.

Dealer captives are domiciled either offshore (Turks & Caicos, tribal nations) for lighter regulation and lower capitalization thresholds, or domestically in captive-friendly states like Vermont, Utah, or Delaware. As of 2024, more than 6,200 captives operate globally.

Primary advantages for dealers:

- Broadest product eligibility, including coverage types unavailable through VSC or PORC structures

- Full customization of coverage terms

- Potential to insure risks beyond F&I (business interruption, cyber, property)

- Full insurance tax treatment

The trade-off is compliance burden — captives carry the highest regulatory load of any dealer structure. They are regulated by a Department of Insurance and subject to annual financial statement requirements, actuarial certifications, and ongoing regulatory oversight.

Relationship to Reinsurance

Dealer captives typically reinsure the risks of a fronting carrier, similar to a PORC arrangement. The key difference: captives operate as fully licensed insurance companies, which means broader underwriting authority, higher capital requirements, and direct regulatory accountability to a Department of Insurance.

Regulatory Exposure

A risk transfer agreement used to shift uninsured dealer obligor risk to an affiliated captive may itself constitute an insurance contract under state law. If not properly structured, that creates regulatory exposure — a risk that requires experienced legal and compliance oversight from the outset.

Capitalization Requirements

Domestic and offshore domiciles differ significantly in their minimum capital thresholds. Domestic states tend to require more upfront capital, while offshore jurisdictions offer lower entry points — though regulators retain discretion to raise requirements based on risk profile.

Capitalization requirements (domestic):

- Vermont: Pure $250,000; Association $500,000

- Utah: Pure $250,000; Association $500,000

- Delaware: Pure $250,000; Association $750,000

Capitalization requirements (offshore):

- Turks & Caicos PORC guideline: Minimum paid-up capital $5,000, with Commission discretion to increase based on risk

- Cayman Islands: Class B(i) general $100,000; B(ii) $150,000; B(iii) $200,000; Class C $500

Which Reinsurance Structure Is Right for Your Dealership?

The decision comes down to four key factors:

- Annual F&I premium volume

- Capital availability and willingness to tie up funds

- Appetite for regulatory compliance and administrative burden

- Tax strategy goals — current tax efficiency (PORC 831(b)), long-term deferral (DOWC), or full insurance tax treatment (Captive)

Volume-Based Guidance

- Dealers with annual premium below the IRC 831(b) threshold ($2,900,000 for 2026) often benefit most from a PORC structure, where the 831(b) election taxes only investment income

- Dealers with high volume who have exhausted 831(b) eligibility or need broader product coverage may find a Captive more appropriate

- DOWCs fit dealers with substantial VSC volume who want direct product control and can manage state licensing across multiple markets

Dealer Type Matching

- BHPH and independent dealers: Typically align best with admin obligor PORC programs given lower capital requirements, simpler setup, and ability to retain VSC and ancillary product profits without state insurance licensing complexity

- Franchise dealers or large multi-rooftop groups: May consider a Captive if their risk portfolio extends beyond standard F&I products or if they seek bespoke coverages

- Retail dealers with established VSC volume: DOWCs are more common among those wanting in-house product control

Risk Tolerance and Exit Strategy

- PORCs carry full risk of loss (underwriting losses reduce the dealer's account)

- DOWCs face first-dollar claims exposure and a deferred tax cliff

- Dealers should model worst-case loss scenarios, understand what happens if they sell the dealership, and confirm their administrator can support a clean transition or run-off

- Captives carry the highest compliance exit cost

Practical Recommendation for Most Independent and BHPH Dealers

Once you've assessed your risk tolerance and exit options, the structure question usually becomes clear for most independent and BHPH dealers.

An admin obligor PORC — where the administrator is the obligor and the dealer's reinsurance company is backed by A-rated insurers — delivers profit capture, tax efficiency, regulatory simplicity, and claims protection without the overhead of a Captive or the licensing complexity of a DOWC. For dealers still weighing the options, DealerRE has guided more than 400 dealers through this decision since 1994. A direct conversation with their team can match the right structure to your volume, tax goals, and exit timeline.

Conclusion

PORC, DOWC, and Captive structures each serve a distinct role in the dealer participation program landscape. No single structure is universally superior — the right choice depends on your dealership's premium volume, capital position, regulatory appetite, and long-term tax strategy.

At a glance:

- PORCs offer profit capture with tax efficiency and a lower setup burden

- DOWCs provide product control with deferred — not eliminated — tax liability

- Captives deliver maximum customization, but come with the highest compliance requirements

The structure you choose has real financial consequences. Get it right and you retain underwriting profit, earn investment income, and build a program that compounds in value. Get it wrong and you face unexpected tax bills, regulatory exposure, or operational complexity that offsets the gains.

DealerRE has helped more than 400 dealers navigate exactly this decision. With over 28 years of experience structuring dealer-owned reinsurance programs, the team helps dealerships match the right structure to their specific volume, capital position, and goals — so the program improves F&I profitability and holds up over the long term.

Frequently Asked Questions

What is a PORC and how does it differ from a DOWC?

A PORC is a reinsurance company that assumes insurance risk ceded from a fronting carrier and earns underwriting profit. A DOWC is a service contract obligor company that issues VSCs directly to consumers and defers (but does not eliminate) taxes. The key distinction: a PORC involves actual risk transfer under a reinsurance agreement, while a DOWC carries contractual service obligations with no insurance risk transfer involved.

What is the difference between captive insurance and traditional insurance?

Traditional insurance involves purchasing coverage from a third-party insurer who retains underwriting profit. Captive insurance involves a company owning its own insurance entity, allowing it to retain underwriting results, customize coverage, and benefit from insurance tax treatment rather than paying premiums to an outside carrier.

What is the point of a captive insurer?

For auto dealers, a captive exists to recapture underwriting profits that would otherwise go to a third-party provider, gain control over coverage terms, and access insurance tax treatment. It can also cover risks that are unavailable or prohibitively expensive in the commercial market.

What are the two major types of captive insurance companies?

The two primary types are single-parent captives (owned by one company, insuring only its own risks) and group or association captives (owned by multiple unrelated companies that pool risks together). For auto dealers, the single-parent structure is most common.

Do captives buy reinsurance?

Yes, dealer-owned captive insurance companies typically operate by reinsuring the risks of a fronting (admitted) insurance carrier that issues the underlying policies or CLIPs. That structure mirrors how a PORC operates — the captive receives premiums in exchange for assuming the risk ceded by the fronting insurer.

Which reinsurance structure is best for independent auto dealers?

Most independent and BHPH dealers are well-suited for an admin obligor PORC structure. It offers lower setup costs, no state VSC licensing burden, favorable IRC 831(b) tax treatment, and the ability to capture 100% of underwriting profit on VSC and ancillary F&I products — without the deferred tax cliff of a DOWC or the compliance weight of a full captive.