Introduction

Most auto dealers who sell F&I products leave significant underwriting profits with third-party insurers — profits that a dealer-owned reinsurance company can recapture. The decision to start one often comes down to a single foundational choice: domestic or offshore.

That choice affects startup costs, tax treatment, regulatory burden, investment flexibility, and how quickly a dealer starts building real wealth through reinsurance. The right structure depends entirely on your dealership's volume, tax situation, and long-term goals — there's no universal answer.

This article covers how each structure works, the key differences between them, and a practical framework for choosing the right fit based on dealership size, volume, and financial goals.

Key Takeaways

- Offshore reinsurance structures (CFC, NCFC) are the most widely used by auto dealers due to lower startup capital and reduced regulatory overhead

- Domestic structures (DOWC, tribal domicile) are U.S.-based, offer potential decades of tax-advantaged operation, and are increasingly accessible to more dealers

- Both structure types typically require an IRC Section 953(d) election or equivalent — offshore programs still file and pay U.S. federal taxes

- The right structure depends on sales volume, tax situation, risk tolerance, and time horizon

- An experienced reinsurance partner managing administration, compliance, and reporting is critical regardless of which structure you choose

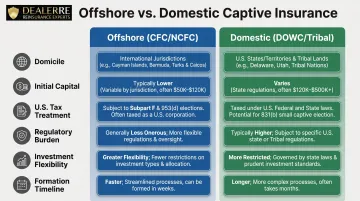

Domestic vs. Offshore Reinsurance: Quick Comparison

The table below breaks down the six factors that most directly affect which structure fits your dealership's goals, capital position, and risk tolerance.

| Factor | Offshore (CFC/NCFC) | Domestic (DOWC/Tribal) |

|---|---|---|

| Domicile | Turks & Caicos Islands, Nevis, Seychelles, or other offshore jurisdictions | U.S. state-licensed entity or tribal jurisdiction (e.g., Delaware Tribe of Indians in Kansas) |

| Initial Capital | $2,500–$25,000 (historically low barriers to entry) | $50,000–$500,000+ depending on state (Florida requires $500,000; tribal domiciles offer lower thresholds) |

| U.S. Tax Treatment | With 953(d) election, files U.S. federal returns as domestic insurance company | Treated as U.S. insurance company; claims paid can generate negative taxable income |

| Regulatory Burden | Lighter oversight, fewer annual filings, no state examination cycle | Subject to state insurance department oversight, annual filings, periodic examinations |

| Investment Flexibility | Assets held in U.S. institutions with flexibility to borrow against reserves and reinvest | Comparable flexibility with stricter reserve requirements |

| Formation Timeline | Days to weeks | Six months to over a year for state-domiciled entities |

What Is Offshore Reinsurance?

Offshore dealer reinsurance refers to a structure where the dealer forms a captive reinsurance company domiciled in a foreign jurisdiction — most commonly the Turks and Caicos Islands. Contrary to popular misconception, offshore structures are not primarily about tax evasion. They exist to provide lower capital requirements, reduced regulatory burden, and the ability to combine credit insurance and property/casualty products (like VSCs) in one entity — something historically difficult in U.S. domiciles.

Historical Background

Dealer-owned reinsurance originated in Texas in the 1950s with credit insurance reinsurers. The industry migrated to Arizona, which originally required just $25,000 in capital. By the late 1970s, dealers began moving offshore to Bermuda and the Cayman Islands because these jurisdictions allowed reinsurance of casualty products (service contracts) alongside credit life and disability — product combinations not permitted under Arizona law at the time.

From the 1980s through the 1990s, the industry continued shifting jurisdictions — each move driven by lower capital requirements and broader product scope, not tax motivations:

- Texas → Arizona: Early credit insurance roots; $25,000 capital threshold

- Bermuda / Cayman Islands: First offshore move; enabled casualty product reinsurance

- Turks and Caicos → BVI → Nevis/TCI: Settled where product flexibility and lighter regulation converged

TCI now hosts over 6,000 active producer-owned reinsurance companies, regulated under a framework designed specifically for dealer-focused programs.

IRC Section 953(d) Election: Dispelling the Tax-Free Myth

Nearly all offshore dealer reinsurance programs elect under IRC Section 953(d) to be taxed as U.S. domestic insurance companies for federal income tax purposes. This means:

- The offshore entity files annual federal returns (Form 1120-PC for property and casualty)

- It is subject to tax on worldwide income

- The election eliminates the federal excise tax (FET) of 1% or 4% on U.S.-source premiums

- The entity is not tax-exempt simply because it is domiciled offshore

This election is widely used because post-1986 tax law changes made it economically rational — CFC shareholders are taxed regardless, so the 953(d) election removes additional excise tax burdens.

Two Main Offshore Structures

Controlled Foreign Corporation (CFC):

- Wholly dealer-owned

- Allows tax-deferred premium growth

- Investment borrowing and flexible reinvestment permitted

- Can elect IRC 831(b) treatment (taxed only on investment income up to approximately $2.35M–$2.8M in premiums)

Non-Controlled Foreign Corporation (NCFC):

- Used by larger dealer groups

- Removes individual premium caps

- Expands the investment pool

- Offers less direct control than a CFC

Use Cases for Offshore Reinsurance

Offshore CFCs are well-suited for small-to-mid-sized dealers entering reinsurance for the first time. The lower startup capital and simpler formation process make them accessible without requiring high initial investment.

BHPH dealers are another strong fit. Offshore structures work particularly well here because admin obligor reinsurance programs can be built to protect vehicles from mechanical breakdown and insurance losses funded directly by the customer base.

DealerRE helps BHPH dealers establish these programs, covering products like Debt Cancellation Coverage (DCC), Collateral Protection Insurance (CPI), VSCs, and GAP waivers — all structured around the monthly payment cycle typical of BHPH operations.

What Is Domestic Reinsurance?

Domestic reinsurance structures are dealer-owned entities formed within the United States — either as state-licensed insurance companies or through tribal domiciles (such as the Delaware Tribe of Indians in Kansas). The most common domestic structure is the Dealer Owned Warranty Company (DOWC), where the dealer acts as the obligor on F&I contracts rather than relying on a third-party carrier.

Tax Mechanics That Make DOWCs Compelling

The DOWC's tax advantage comes from a specific timing difference:

- Gross premium is amortized into income over the life of the policy

- All acquisition costs, commissions, and administrative fees are deductible in the year incurred

- Under IRC Section 832(b)(4), 20% of unearned premium reserves must be added back to taxable income

This creates net operating losses (NOLs) that can offset other dealership income. The average deferral period is 7–10 years, meaning a well-managed DOWC can operate on a tax-advantaged basis for decades. That's a different mechanism than the 831(b) premium exclusion used in offshore CFC structures — and for many high-volume dealers, a more powerful one.

Key Benefits of Domestic Structures

- Maximum tax efficiency: NOL generation can offset dealership income for years

- Full branding and product control: The dealer acts as the obligor and controls claims handling

- No offshore jurisdictional risk: All assets and operations remain in the U.S.

- Estate and succession planning alignment: Ideal for multi-generational dealership families

Hybrid Structures: The Super CFC (CFC+)

The Super CFC combines an offshore CFC's ease of formation and investment flexibility with retail accounting that mimics DOWC-level tax deferment. This represents a middle path for dealers who want tax efficiency without the full complexity of a standalone domestic entity.

Drawbacks of Domestic Structures

Domestic structures generally require:

- Higher initial capitalization ($50,000–$500,000 depending on state)

- Longer formation timelines (six months to over a year)

- More intensive regulatory compliance (state insurance department oversight, annual filings, periodic examinations)

These factors make DOWCs a better fit for higher-volume dealers with the administrative bandwidth to manage them.

Tribal Domicile Option

The Delaware Tribe of Indians operates a Tribal Domicile in Caney, Kansas, offering an alternative domestic domicile for dealer-owned reinsurance. Allied Reinsurance Companies (ARCs) domiciled there are considered domestic insurance companies but offer an "affordable domestic alternative to traditional offshore domiciles" with simplified regulatory requirements under tribal sovereignty.

Use Cases for Domestic Reinsurance

DOWCs are best suited for higher-volume franchise and retail dealers with established F&I programs. Common use cases include:

- Long-term wealth accumulation and after-tax profitability optimization

- Multi-generational succession planning for dealership families

- Full product customization, including tying service contract terms to the dealer's own service drive

Which Structure Is Right for Your Dealership?

Volume and Premium Thresholds

According to industry research:

- Retro/profit-share programs: Generally require $50,000+ annual premium

- Offshore CFCs: Accessible to smaller dealers; no strict volume minimums in many cases

- Domestic reinsurers: Historically best suited for dealerships producing $250,000+ in annual premium

Smaller stores often find offshore CFCs justify the investment more quickly, while DOWCs need higher premium volume to offset formation and compliance costs.

Tax Situation

A dealer's current personal and business tax picture significantly affects which structure delivers the most after-tax value:

- Dealers in high tax brackets with long time horizons often benefit most from DOWC or hybrid structures

- Dealers seeking near-term cash access may prefer the borrowing flexibility of a CFC

- Post-2017 Tax Cuts and Jobs Act, many dealers have reconsidered NCFC structures due to uncertain future tax implications and new disclosure requirements

Risk Tolerance and Product Mix

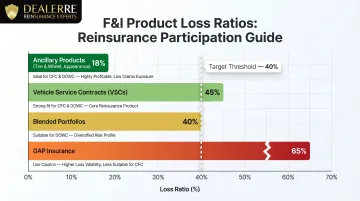

Not all F&I products are ideal for reinsurance participation. Research shows loss ratios vary significantly by product:

- VSCs: 25%–45% loss ratios; generally favorable for CFC/DOWC participation

- Ancillary products (tire and wheel, appearance): Often under 20%; most favorable for participation

- Blended portfolios: Target 30%–40% loss ratios

- GAP insurance: Higher and more volatile loss ratios driven by vehicle depreciation, interest rates, and total-loss frequency

Dealers with diverse, lower-loss-ratio product mixes (VSCs, tire and wheel, appearance) have more to gain from either a CFC or DOWC than those relying heavily on GAP or other high-volatility products.

Time Horizon

Offshore CFCs:

- Formation in days to weeks

- Can begin generating returns sooner

- Ideal for dealers seeking accessible entry points

Domestic DOWCs:

- Formation in six months to over a year

- Structured for long-term wealth building

- Dealers with 10+ year horizons and succession planning goals often find domestic structures deliver more total value over time

Administrative Capacity and Partner Selection

Once you've weighed volume, tax position, product mix, and timeline, execution comes down to one factor: your administrator. The right partner handles legal formation, tax filings, compliance, claims adjudication, and performance reporting — so you focus on selling cars.

DealerRE manages the full administrative lifecycle for dealer clients, regardless of which structure they choose. That includes:

- Legal formation and licensing

- Tax return preparation and renewals

- Claims adjudication (through partnership with Assured Vehicle Protection)

- Monthly financial statements and performance reporting

- Ongoing compliance monitoring

- Training and onboarding for dealership staff

Example Scenario:

Two similar-sized independent dealers each sell 80 units per month with $150,000 in annual F&I premium:

Dealer A chooses an offshore CFC due to lower startup capital ($25,000 vs. $150,000), faster formation (three weeks vs. nine months), and simpler compliance. They begin retaining underwriting profits within the first quarter and use investment flexibility to borrow against reserves for dealership expansion.

Dealer B opts for a DOWC because they're part of a multi-generational family dealership focused on long-term tax efficiency and succession planning. The higher upfront cost and longer timeline are offset by NOL generation that shelters other dealership income for the next decade, creating more total after-tax value over 15 years.

The scenarios above show the same revenue base producing two very different optimal outcomes. Choosing the right structure starts with an honest look at where your dealership is today — and where you want it in 10 years.

Conclusion

Neither offshore nor domestic structures are universally superior. Offshore CFCs offer accessibility, flexibility, and lower startup costs, while domestic DOWCs deliver maximum tax efficiency and control for dealers with larger programs and longer-term planning goals.

Choosing the right structure is only half the equation. Execution determines results — and that depends on the administrator managing compliance, claims, and performance reporting behind the scenes. DealerRE has helped over 400 auto dealers nationwide establish and manage reinsurance programs, handling everything from tax filings and compliance to claims adjudication and financial reporting, regardless of whether a dealer selects an offshore or domestic structure.

Frequently Asked Questions

What are the 4 types of reinsurance?

The four common dealer reinsurance structures are walkaway (no participation), retro/profit-share, CFC/offshore captive, and DOWC/domestic captive. Each represents a different level of risk participation and profit retention — from zero participation in walkaway programs to full underwriting profit retention in CFCs and DOWCs.

What is the difference between inward and outward reinsurance?

Outward (ceded) reinsurance is when a primary insurer transfers risk to a reinsurer, while inward (assumed) reinsurance is when the reinsurance company accepts that risk. In a dealer-owned structure, the dealer's captive is the assuming (inward) reinsurer receiving ceded premiums from the primary carrier.

Do offshore dealer reinsurance companies pay U.S. federal taxes?

Virtually all offshore dealer reinsurance companies elect under IRC Section 953(d) to be taxed as U.S. domestic insurance companies. They file annual federal returns and are not tax-exempt simply because they are domiciled offshore.

What are the key compliance differences between domestic and offshore dealer reinsurance structures?

Domestic DOWCs are subject to state insurance department oversight and must meet capitalization, reserve, and filing requirements in their domicile state. Offshore CFCs operate under a foreign domicile's regulatory framework but still require 953(d) tax elections and annual U.S. federal filings to remain compliant.

What is the minimum sales volume needed to benefit from a dealer reinsurance program?

Volume thresholds vary by structure. Offshore CFCs can be viable for smaller stores, while domestic DOWCs typically require higher annual premium volume (often $250,000+) to justify setup and compliance costs, according to industry research.

Can BHPH dealers participate in dealer reinsurance programs?

BHPH dealers can participate in reinsurance, particularly through admin obligor structures that protect vehicles from mechanical breakdown and insurance losses funded by the customer base. These programs commonly cover products like DCC, CPI, VSCs, and GAP waivers.