Introduction

Auto dealers who sell F&I products — vehicle service contracts, GAP, appearance protection — are generating underwriting profit on every deal. The problem? Most of it flows straight to third-party providers. Dealer-owned reinsurance changes that equation, but the structural choice between a CFC (Controlled Foreign Corporation) and NCFC (Non-Controlled Foreign Corporation) determines how much you keep, how it's taxed, and how far it can scale.

That structural choice carries real financial weight. Premium capacity, tax treatment, ownership control, and long-term wealth-building all hinge on which entity you operate.

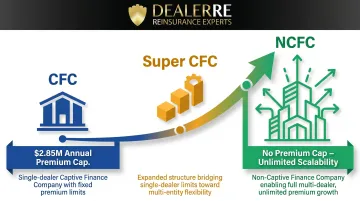

A CFC offers powerful tax advantages but caps annual premiums at $2.85 million (2025). An NCFC removes that cap entirely — but operates under different tax rules and ownership mechanics.

What follows is a side-by-side breakdown of both structures — covering taxes, ownership, premium limits, and scalability — so you can match the right vehicle to where your dealership is headed.

Key Takeaways

- CFC (Controlled Foreign Corporation): Dealer-owned offshore reinsurance entity; qualifies for IRS 831(b) tax election; best for small to mid-sized dealers with annual net ceded premium caps of $2.85M (2025) and $2.9M (2026).

- NCFC (Non-Controlled Foreign Corporation): Pooled offshore reinsurance structure with no ownership control by any single dealer and no annual premium cap — designed for high-volume or multi-rooftop operations.

- The two structures diverge most on premium scalability, tax treatment, and how much direct control you retain over your reinsurance company.

- Neither structure is universally superior — the right fit depends on your F&I volume, risk tolerance, and long-term financial goals.

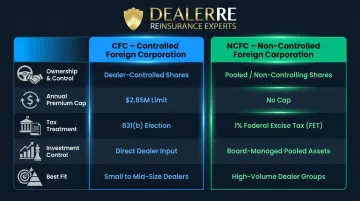

CFC vs NCFC: Quick Comparison

| Dimension | CFC (Controlled Foreign Corporation) | NCFC (Non-Controlled Foreign Corporation) |

|---|---|---|

| Ownership & Control | Dealer or related parties own >50% of voting power or total value (>25% for insurance companies under IRC §953(c)). | Ownership spread across multiple dealers; no single party holds a controlling interest. Dealers typically hold non-voting or restricted shares. |

| Annual Premium Capacity | Capped at $2.85M (2025) / $2.9M (2026) in net ceded premium per year under IRC 831(b). Indexed annually in $50K increments. | No annual premium cap under U.S. tax law. Built for scalability beyond 831(b) limits. |

| Tax Treatment | Treated as a U.S. insurer under IRC §953(d); premiums excluded from taxable income up to the cap. Only investment income is taxed. Exempt from federal excise tax (FET). | No 831(b) election available. Remains offshore for tax purposes; subject to 1% FET on ceded premiums. Income deferred until distribution to U.S. shareholders. |

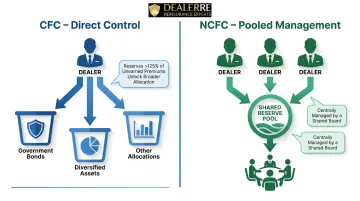

| Investment Structure | Dealer has direct input over reserve investment. Starts conservatively (government bonds); can shift to more aggressive allocations once reserves exceed 125% of unearned premiums. | Pooled reserves managed by the board or appointed managers. Dealers don't control individual allocation, but benefit from institutional scale and diversification. |

| Administrative Complexity | Manageable with an experienced administrator. Core requirements: compliance filings, tax returns, annual renewals, and investment oversight. | More moving parts due to the pooled structure, but centralized management reduces the burden on individual dealers. |

What Is a CFC Reinsurance Program?

A Controlled Foreign Corporation (CFC) is an offshore reinsurance company that the dealer or related parties own and control, designed to capture the underwriting profit from F&I products sold at the dealership. "Controlled" means U.S. shareholders own more than 50% of the voting stock or total value — or for insurance companies, 25% or more under IRC Section 953(c). This ownership structure is what distinguishes a CFC from an NCFC.

The 831(b) Tax Election

Under IRC Section 831(b), a small insurance company can elect to exclude net written premiums from taxable income up to an annual cap. For 2025, that cap is $2.85 million; for 2026, it rises to $2.9 million, adjusted annually for inflation in $50,000 increments.

When a CFC makes the 831(b) election (via IRC Section 953(d), which allows the offshore entity to be taxed as a domestic insurer), the dealer is taxed only on investment income, not premium income — keeping the bulk of earned premiums sheltered within the structure.

Key Operational Benefits for Dealers

- Controls the reinsurance entity and its accumulated reserves directly

- Works with asset managers to select investments aligned with risk tolerance and time horizon

- Retains both underwriting profit and investment income — no sharing with third-party providers

- Deploys earned income into the dealership, real estate, education, or other assets

Where CFCs Hit a Ceiling

The 831(b) cap is also the structure's main constraint. Once F&I premium volume approaches or exceeds that threshold, the CFC can no longer scale efficiently. Dealers who continue to grow may need to form multiple CFCs — which introduces ownership complexity — or explore an NCFC instead.

Use Cases of CFC

Ideal dealer profile:

- Single-point or small dealer groups (typically one to four rooftops)

- Consistent but not yet high-volume F&I production

- Dealers who want to start retaining underwriting profit with direct control and meaningful tax efficiency

Products best suited for a CFC:

- Stable, predictable F&I products: vehicle service contracts, appearance protection, ancillary coverage

- Products with manageable loss patterns and steady claims experience

- GAP coverage typically needs separate risk management given its less predictable loss patterns

Working with a full-service administrator:

Running a CFC effectively requires professional support. A full-service administrator handles legal setup, compliance filings, claims adjudication, tax returns, and F&I training — so dealers can stay focused on the finance office. DealerRE has supported dealers in this capacity for over 28 years, managing all filings, tax returns, and renewals while ensuring programs are backed by A-rated insurers.

What Is an NCFC Reinsurance Program?

A Non-Controlled Foreign Corporation (NCFC) is an offshore reinsurance company in which multiple dealers participate as shareholders, but no individual dealer or U.S. shareholder group holds controlling ownership or voting authority. This structural distinction prevents it from being classified as a CFC under U.S. tax law and unlocks different tax treatment and scalability.

Ownership Mechanics

Dealers typically hold non-voting or restricted shares, with governance controlled by the reinsurance company's board or managing entity. Each dealer's participation is tracked separately (often through a distinct share class tied to their production), but the entity operates as a pooled structure.

That pooled design is intentional — it enables scalability beyond the 831(b) cap without triggering CFC ownership thresholds.

Tax and Regulatory Implications

NCFC programs do not elect U.S. insurer tax treatment under IRC Section 953(d), so they are not subject to the annual premium cap. However, they are subject to:

- 1% federal excise tax (FET) on ceded reinsurance premiums (IRC Section 4371)

- Income deferral until distributions are made to U.S. shareholders

- No Subpart F exposure (Subpart F applies only to CFCs, not NCFCs)

Because NCFCs remain offshore and do not make the 831(b) election, dealers sacrifice the tax-free treatment of underwriting profits in exchange for unlimited premium capacity. FET planning and income deferral timing are the two areas where qualified tax counsel most often adds value.

Investment Structure

In a CFC, dealers often influence investment decisions directly. An NCFC works differently: assets are pooled across all participants, and the board or appointed managers oversee investments centrally under a defined policy. The tradeoff is straightforward — dealers gain scale and diversification but give up direct control over asset allocation.

Use Cases of NCFC

Ideal dealer profile:

- High-volume dealers or dealer groups (typically five or more rooftops)

- Single-point dealers with consistently high F&I production

- Dealers approaching or exceeding the CFC's annual premium threshold who need a structure that can grow without the cap constraint

Key consideration when evaluating NCFC programs:

Not all programs are structured or administered equally. Differences in fee transparency, claims adjudication standards, reserve methodology, and reporting quality can significantly affect long-term results. Vetting the administrator is as important as understanding the structure itself.

CFC vs NCFC: Which Reinsurance Structure Is Right for Your Dealership?

The right structure depends on three core factors:

- Current and projected F&I premium volume

- Appetite for control and administrative involvement

- Long-term financial objectives (near-term cash access vs. long-term tax-deferred wealth accumulation)

Situational Guidance

Scenario A: Single-point or small group dealer

- Growing but manageable F&I volume

- Wants to start building reinsurance wealth with direct control and tax benefits

- Best fit: CFC — provides tax efficiency under 831(b), direct ownership, and straightforward administration with the right partner

Scenario B: Multi-rooftop dealer group or high-volume single store

- Approaching or exceeding the $2.85M annual premium cap

- Seeking scalability without administrative fragmentation across multiple entities

- Best fit: NCFC — removes the premium cap, offers pooled investment benefits, and scales with growth

When to Transition

Signals that a dealer may need to move beyond a CFC:

- Premium volume consistently near the 831(b) cap

- Needing to form a second or third CFC to accommodate volume

- Administrative burden of managing multiple entities outweighs the tax benefit

Some dealers use a Super CFC as an interim step before exploring NCFC: a more advanced CFC structure that accommodates higher premium volume while maintaining controlled ownership.

Schedule a Consultation

Once you know where your volume stands and where you want to go, the structure decision becomes straightforward. DealerRE reviews your F&I premium volume, evaluates your growth trajectory, and recommends the program setup that fits your dealership — then manages the compliance, filings, and administration so you can stay focused on selling. Schedule a consultation to get a clear picture of which structure fits your situation.

Frequently Asked Questions

What is an NCFC?

NCFC stands for Non-Controlled Foreign Corporation — an offshore reinsurance structure where multiple dealers participate without any single dealer holding controlling ownership, enabling scalability beyond CFC premium limits with tax deferral benefits and pooled investment management.

How to know if a company is a CFC?

A company is classified as a CFC when U.S. shareholders collectively own more than 50% of the voting stock or total value. For insurance companies, the threshold is 25% or more under IRC Section 953(c). In dealer reinsurance, this typically means the dealer and related parties are the primary owners and exercise control.

What is the difference between CFC and Super CFC?

A Super CFC is an advanced CFC structure designed to accommodate higher premium volume while maintaining the dealer's controlled ownership model. It acts as an intermediate step between a standard CFC (with its 831(b) cap) and an NCFC for dealers who need more capacity but want to retain direct ownership and control.

What is the difference between reinsurance accepted and reinsurance ceded?

Reinsurance ceded is the premium a primary insurer transfers to pass along risk; reinsurance accepted is what the reinsurer takes on. In dealer reinsurance, F&I premiums are ceded from the primary insurer into the dealer's CFC or NCFC, which then accepts that risk and participates in the underwriting profit.

What are the 4 types of reinsurance?

The four primary types are:

- Facultative — negotiated contract by contract

- Treaty — covers a portfolio under a standing agreement

- Proportional — risk and premium shared at a set ratio

- Non-proportional — reinsurer pays only when losses exceed a threshold

Most dealer programs use a treaty/proportional structure — specifically quota share — where the dealer's reinsurance entity assumes a fixed percentage of premiums and corresponding losses from F&I products.