](https://file-host.link/website/dealerre-3iaaqr/assets/blog-images/bec91c5a-ae6d-406a-a6df-f71b9c159de7/1778047621519612_2ef4396443334d8ba79dc79610969f89/360.webp)

Introduction

The choice between CFC and NCFC reinsurance structures is one of the most consequential decisions a dealer makes when entering reinsurance. Selecting the wrong structure can limit growth, create unexpected tax exposure, or lock a dealer into terms that don't fit their volume or long-term goals.

Many dealerships get this wrong — not from carelessness, but from incomplete information or industry hearsay. The consequences are real:

- Leaving underwriting profits on the table

- Exceeding regulatory caps without realizing it

- Surrendering control over your own reinsurance income

This guide breaks down both structures in plain terms, identifies the six key factors every dealer should evaluate, and outlines a clear decision framework — so the decision is driven by data and strategy, not guesswork.

Key Takeaways

- CFC (Controlled Foreign Corporation) is dealer-owned and dealer-controlled, with an annual premium cap of $2.85M (2025) and favorable tax treatment

- NCFC (Non-Controlled Foreign Corporation) pools risk across multiple dealers offshore, with no annual premium cap—built for high-volume operations

- Your choice depends on six factors: F&I volume, control preferences, tax goals, cash flow needs, risk tolerance, and claims history

- The right fit depends on where your dealership stands today and the direction you're growing toward

- A qualified reinsurance advisor can map both structures against your numbers before you commit

What Are CFC and NCFC Reinsurance Structures?

Dealer-owned reinsurance lets a dealership own its own reinsurance company and capture underwriting profits that would otherwise flow to third-party warranty or insurance providers. The structure you choose determines who controls those profits, how they're taxed, and what volume limits apply — which is why the CFC vs. NCFC decision carries real financial consequences.

CFC (Controlled Foreign Corporation / PARC)

A CFC — also commonly called a PARC (Producer-Affiliated Reinsurance Company) — is a foreign reinsurance entity that the dealer owns and controls directly. It files an annual U.S. corporate tax return and operates under IRS rules that cap annual net ceded premium at approximately $2.85 million for 2025 (rising to $2.9 million in 2026) to maintain favorable tax treatment under IRC Section 831(b).

Key advantages for dealers:

- Dealer serves as owner, officer, and director with full decision-making authority

- Profits accessed via loans against surplus or declared dividends, typically taxed at capital gains rates

- Assets invested monthly, generating additional investment income

- Most dealer CFCs elect domestic treatment under IRC Section 953(d), filing Form 1120-PC or 1120-L instead of triggering Subpart F income on personal returns

NCFC (Non-Controlled Foreign Corporation)

An NCFC is an offshore reinsurance company — often domiciled in Bermuda or the Cayman Islands — where no single U.S. dealer owns more than 25% of voting power or value. That ownership cap keeps it outside the IRS "controlled" classification under IRC Section 957(b), shielding it from Subpart F income rules and letting underwriting profits accumulate tax-deferred.

In practice, this structure works differently from a CFC:

- Dealers participate as minority shareholders in a pooled reinsurance company alongside other dealers

- Premium is ceded monthly without annual limits

- Investment decisions are made by the reinsurance company's board or professional managers, not the individual dealer

- Dealers receive distributions based on participation share rather than controlling distribution timing

- Subject to 1% federal excise tax on ceded reinsurance premium under IRC Section 4371

Key Differences Between CFC and NCFC Reinsurance

Understanding the structural differences across four critical dimensions makes the decision clear rather than arbitrary.

Ownership and Control

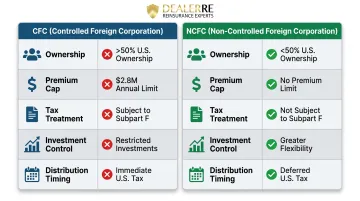

CFC: The dealer is the owner, officer, and director—they can make decisions about investments, distributions, and program structure.

NCFC: The dealer holds non-voting or limited shares; governance sits with the reinsurance company's board. This tradeoff—less control for more scale and tax deferral—is the central tension every dealer must resolve.

Premium Capacity and Scalability

CFC: The annual net ceded premium cap of approximately $2.85 million (2025) is a hard ceiling. Exceeding it without establishing additional CFCs triggers significant tax penalties.

NCFC: No equivalent annual cap, making it the natural choice for high-volume dealerships or dealer groups whose F&I production consistently exceeds what a single CFC can absorb.

F&I profit per vehicle retailed (PVR) hit $2,534 in Q3 2025 across publicly traded dealer groups — up 5.2% year-over-year. Dealers retailing 1,140+ vehicles annually (roughly 95 per month) can approach the CFC cap quickly, depending on their ceded premium percentage. At that volume, the NCFC's unlimited capacity becomes a practical necessity rather than a theoretical advantage.

Tax Treatment

CFC distributions declared as dividends typically receive favorable capital gains tax treatment, and the entity files an annual U.S. corporate return. Under the 831(b) election, only investment income is subject to federal corporate tax. Underwriting income is excluded entirely.

NCFCs avoid Subpart F reporting requirements as long as the ownership structure remains non-controlled (meaning no single U.S. person owns more than 50%), allowing profits to accumulate tax-deferred. That deferral advantage comes with specific obligations, however:

- Subject to 1% federal excise tax on ceded premium

- Passive investment income may fall under PFIC (Passive Foreign Investment Company) rules under IRC Section 1297

- Shareholders must file Form 8621 annually if the NCFC is classified as a PFIC

The tax mechanics of both structures are complex and subject to evolving IRS guidance — which structure minimizes your tax burden depends heavily on your volume, ownership profile, and how quickly you plan to take distributions. A qualified tax advisor familiar with dealer-owned reinsurance is essential before committing to either path.

Investment Structure

CFC: The dealer typically has input into investment portfolio options — assets are invested for the individual dealer's benefit. Common portfolio tiers include:

- Conservative: 100% bonds

- Moderate: 90% bonds / 10% equity

- Growth: 80% bonds / 20% equity

NCFC: Assets are pooled across all participating dealers and managed by professional investment managers under a board-approved investment policy. This means greater institutional diversification but less individual control over allocation decisions.

6 Factors to Help You Choose Between CFC and NCFC

Knowing how CFC and NCFC structures differ is only the starting point. These six factors help you identify which one actually fits your dealership.

Factor 1: Annual F&I Premium Volume

This is the most objective filter. If a dealer's annual net ceded F&I premium consistently approaches or exceeds $2.85 million, a CFC alone cannot scale without adding complexity or tax risk. An NCFC or a multi-CFC strategy becomes necessary.

Volume context: NADA reports 16,990 franchised dealers in the U.S. selling 16.2 million vehicles in 2025—roughly 954 vehicles per dealership annually, or about 80 per month. Dealers well below the premium threshold should typically start with a CFC.

Factor 2: Desire for Ownership and Control

Control is the core question here — specifically, how much authority you want over investment decisions, distribution timing, and your role as officer or director.

If direct control is a priority: A CFC is the better fit.

If you're comfortable with a managed, board-governed structure: An NCFC may work, especially if you prefer a hands-off approach and value pooled diversification over individual authority.

Factor 3: Tax Strategy and Time Horizon

CFC: Provides near-term access to profits with capital gains treatment, suiting dealers who want to deploy reinsurance earnings back into the business, real estate, or personal wealth in the short-to-medium term.

NCFC: Tax deferral suits dealers with a longer time horizon who want profits to compound offshore before distribution. However, work with a tax advisor to model exit planning and distribution tax treatment before committing.

Factor 4: Cash Flow Needs and Liquidity

Consider how soon you may need access to reinsurance earnings:

- CFC: Declare dividends or take surplus loans on demand — suited for reinvestment in the dealership, real estate, education, or other near-term uses

- NCFC: Funds stay in reserves subject to board-governed distribution policies, making short-term access limited

Factor 5: Risk Tolerance and Claims History

Evaluate your dealership's historical F&I claims experience.

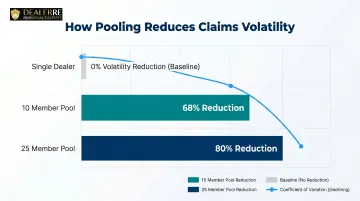

Higher or volatile claims activity: May benefit from the risk pooling an NCFC provides. Actuarial analysis shows that pooling reduces the Coefficient of Variation (loss volatility measure) by 68% at 10 members and 80% at 25 members.

Strong, consistent claims record: You may prefer to keep underwriting gains in a CFC rather than pool them with others whose loss experience you can't control.

Factor 6: Administrative Capacity and Complexity Tolerance

CFC administrative obligations:

- File a U.S. tax return (Form 1120-PC) and Form 5471 with personal returns

- Oversee investment choices and maintain ongoing compliance

- The IRS imposes substantial penalties for non-compliance

NCFC administrative tradeoffs:

- Board and program administrator handle most operational filings

- Still requires federal excise tax on ceded premium and IRS disclosure (Form 8621 if PFIC)

- Compliance quality depends heavily on the administrator you choose

How DealerRE Can Help You Choose the Right Structure

With 28+ years of experience helping dealers nationwide, DealerRE starts every relationship with a comprehensive business analysis to determine which structure genuinely fits the dealership's volume, goals, and financial situation.

That full-service model covers every stage of program management:

- Manage all legal forms, filings, tax returns, and renewals

- Provide comprehensive staff onboarding and F&I training (online and in-person)

- Adjudicate claims

- Deliver ongoing performance reporting and financial statements

DealerRE specializes in admin obligor reinsurance structures backed by A-rated insurers, so your reinsurance company operates within a secure, compliant framework from day one. Dealers can schedule a no-obligation consultation to have their F&I production and financial goals evaluated before choosing a structure.

Conclusion

The CFC vs. NCFC decision is not about which structure is more prestigious or popular—it's about which one aligns with where the dealership is today and where it intends to go.

Three factors drive that alignment:

- Premium volume — whether current production justifies a CFC or warrants the broader capacity of an NCFC

- Tax position — how the dealer's overall tax exposure shapes the value of each structure

- Cash flow needs — whether immediate access to funds or long-term accumulation better fits the business

This decision should be revisited as the dealership grows. A CFC that fits at 150 retail units per month may need to evolve into a multi-CFC strategy or an NCFC as volume increases. That evolution is exactly where an experienced reinsurance partner like DealerRE adds lasting value — helping dealers not just set up the right structure, but adapt it as their business scales.

Frequently Asked Questions

What does CFC stand for?

CFC stands for Controlled Foreign Corporation, also commonly referred to as a PARC (Producer-Affiliated Reinsurance Company). It is a dealer-owned, dealer-controlled foreign reinsurance entity that files a U.S. annual tax return under IRC Section 953(d).

What is the annual premium limit for a CFC reinsurance structure?

CFCs are generally subject to an annual net ceded premium cap of approximately $2.85 million for 2025 (rising to $2.9 million in 2026). Exceeding this limit without establishing additional CFC entities can trigger significant tax penalties under IRS Section 831(b) guidelines.

Who controls an NCFC reinsurance company?

In an NCFC, no single U.S. dealer can own more than 25% of voting power or value under IRC Section 957(b). Control rests with the reinsurance company's board of directors or managing entity, not the individual participating dealer.

Which structure is better for smaller or mid-size dealerships?

Most smaller and mid-size dealerships are better served by a CFC structure. Lower setup complexity, dealer ownership and control, favorable capital gains tax treatment, and F&I volume that typically falls within the annual premium cap all make it the more practical starting point.

Can a dealership switch from a CFC to an NCFC as it grows?

Dealers can transition as their production grows, but switching involves legal, tax, and administrative considerations. Plan your structure's evolution with a qualified advisor from the start — it's a strategic move, not a simple upgrade.

What are the main tax differences between CFC and NCFC reinsurance programs?

CFC distributions typically receive capital gains tax treatment and require an annual U.S. corporate return. NCFCs allow profits to accumulate tax-deferred offshore but are subject to a 1% federal excise tax on ceded premium and additional IRS shareholder disclosures.