Introduction

Most auto dealers understand that CFC reinsurance builds wealth by capturing underwriting profits from their F&I products. What many don't fully grasp is how those profits are taxed — or how much of that income can avoid taxation altogether. Misunderstanding the tax treatment of a dealer-owned CFC can lead to unexpected liabilities, missed opportunities, or poorly timed distributions that cost thousands in avoidable taxes.

A Controlled Foreign Corporation (CFC) in the dealer reinsurance context is an offshore-domiciled insurance company that reinsures F&I contracts sold by the dealership. Despite the "offshore" designation, all funds remain in the United States — held in US banks or brokerage accounts. The foreign domicile provides regulatory advantages without moving money out of the country.

This article covers the foundational tax mechanics of CFC reinsurance, including:

- The §831(b) election and how it excludes underwriting profit from income tax

- The annual premium cap and what happens when it's exceeded

- How dividends are taxed when distributed to the dealer-owner

- How the CFC compares to NCFCs, DOWCs, and Super CFCs on a tax basis

Key Takeaways

- A CFC elects under §953(d) to be treated as a US taxpayer, files Form 1120-PC annually, and operates within the US tax system

- Under §831(b), underwriting profit is excluded from taxable income entirely; only investment income is taxed at the 21% corporate rate

- The annual premium cap for 2026 is $2.9 million; exceeding it triggers full taxation of underwriting profit

- Dealer-shareholder dividends qualify for long-term capital gains rates (max 23.8%) — not ordinary income rates up to 40.8%

- CFCs avoid the 1% federal excise tax on reinsurance premiums that NCFCs pay

The §831(b) Election: The Foundation of CFC Tax Treatment

What §831(b) Does

IRS §831(b) allows qualifying small insurance companies to exclude underwriting profit from taxable income. Under this election, the CFC pays federal income tax only on investment income — interest, dividends, and capital gains earned on the assets held inside the company. This is the core tax advantage of the CFC structure.

Underwriting profit (premiums earned minus claims paid) accumulates year after year without triggering taxation. As long as the company stays under the annual premium cap, that profit remains permanently exempt.

How §953(d) Makes It Work

The §831(b) election is only possible because of a separate election under §953(d). This provision allows a foreign corporation to voluntarily be treated as a domestic US taxpayer for all IRS purposes. Without the §953(d) election, US dealer-owners would face annual Subpart F income inclusions on their personal tax returns — a complex and burdensome reporting requirement that treats passive foreign income as immediately taxable.

By making the §953(d) election, the CFC:

- Files a US corporate tax return (Form 1120-PC)

- Pays US corporate income tax on investment earnings

- Avoids federal excise tax on reinsurance premiums

- Eliminates Subpart F complexity for shareholders

Together, these two elections keep the structure fully inside the US tax system — with none of the offshore reporting burden dealers typically want to avoid.

Practical Tax Impact

The combined effect of §953(d) and §831(b) is this: underwriting profits build inside the CFC without annual taxation, while only investment income earned on those accumulated assets is taxed each year at 21%.

Example: A CFC earns $1.8 million in net premium and pays $500,000 in claims. The $1.3 million underwriting gain is excluded from taxable income. The company invests those reserves and earns $40,000 in interest and dividends. Only the $40,000 investment income is taxed at 21%, resulting in an $8,400 tax bill for the year.

Timing and Filing

A CFC takes the §831(b) election in its first year of operation — unlike Dealer-Owned Warranty Companies (DOWCs), which sometimes defer the election while drawing down net operating losses. That first-year election means tax efficiency starts immediately, with no lag period.

DealerRE coordinates with insurance tax specialists to prepare and file the annual Form 1120-PC, keeping the election properly executed year after year.

What Income Is Taxable vs. Exempt Inside a CFC

Taxable Investment Income

Investment income earned inside the CFC is subject to the 21% corporate tax rate under §11(b). This includes:

- Interest from bonds and cash accounts

- Dividends from investment holdings

- Capital gains from sales of securities

- Rental income or royalties (if applicable)

- Income from any non-insurance trade or business

The CFC calculates taxable investment income under §834, which allows deductions for investment expenses, depreciation, interest paid, and capital losses. The net figure is taxed at 21%.

Exempt Underwriting Profit

Underwriting profit is the net difference between earned premiums and paid claims. Under §831(b), this income is permanently excluded from taxation.

Example: A CFC collects $2 million in net premium and pays $650,000 in claims over the year. The $1.35 million underwriting gain is not taxed. If the company earns $25,000 in investment income on its reserves, only that $25,000 is taxed at 21% ($5,250 tax bill).

That underwriting gain disappears from the tax return permanently — which is exactly why the §831(b) election is so valuable for dealers operating below the premium cap.

Subpart F Avoidance via §953(d)

Without the §953(d) election, US shareholders of a foreign corporation must include their proportional share of certain passive income (Subpart F income) on their personal tax returns annually — even if the corporation never distributed a dividend.

The §953(d) election eliminates this by treating the CFC as a domestic corporation. Subpart F rules apply only to foreign corporations, so making the election sidesteps the issue. Dealer-shareholders face no annual tax liability unless they take a dividend, and when they do, it's taxed at favorable capital gains rates.

When filing, confirm with your CPA that the §953(d) election is active and that investment income is reported separately from underwriting results — they're taxed under different rules and must be tracked independently.

The Annual Premium Cap: Thresholds, Limits, and Tax Consequences

Current Premium Threshold

For tax year 2026, the §831(b) annual premium threshold is $2.9 million. For 2025, it was $2.85 million. The cap is indexed annually for inflation and increases in $50,000 increments.

The threshold applies to net written premiums or direct written premiums, whichever is greater. This means dealers cannot artificially reduce below the cap by ceding premiums outward if their direct written premiums already exceed it.

What Happens When You Exceed the Cap

Exceeding the cap is a cliff, not a phaseout. If a CFC's premiums exceed $2.9 million in 2026, the company loses §831(b) eligibility for that year. All underwriting profit becomes fully taxable at the 21% corporate rate.

This is a meaningful tax event. A dealer who exceeds the cap and generates $1.5 million in underwriting profit would owe $315,000 in federal tax instead of zero.

Managing the Cap: Forming Multiple CFCs

Dealers approaching the cap often form additional CFCs with slightly different ownership structures. For example:

- A second CFC owned by a spouse or family trust

- A CFC where business partners hold ownership

- A structure involving adult children or key employees

Each CFC can independently capture up to $2.9 million in premium, allowing a dealership group to scale beyond the single-entity limit. Multi-entity structures also double as succession planning tools, making it easier to transition ownership or reward key personnel over time.

Staying Compliant as Your Program Grows

Once multiple CFCs are in play, the administrative complexity compounds — premium tracking, entity filings, and tax returns must stay synchronized across each structure. DealerRE handles this end-to-end, including:

- Legal entity formation and offshore registration

- Annual tax return preparation (Form 1120-PC)

- Financial reporting and premium tracking

- Renewal filings and regulatory compliance

- Coordination with CPAs and legal counsel

That coordination keeps dealers focused on selling rather than managing compliance deadlines across multiple entities.

How CFC Dividends and Distributions Are Taxed

Qualified Dividend Treatment

Dividends from a §953(d)-elected CFC are treated as distributions from a domestic corporation. When the dealer-shareholder holds the stock for more than 60 days during the 121-day period around the ex-dividend date, the dividends qualify for long-term capital gains rates.

2026 Qualified Dividend Tax Rates:

- 0% for income up to $49,450 (single) or $98,900 (married filing jointly)

- 15% for income between those thresholds and $545,500 (single) or $613,700 (married)

- 20% above those thresholds

Most dealer principals fall into the 20% bracket. The 3.8% Net Investment Income Tax (NIIT) also applies to individuals with modified adjusted gross income over $200,000 (single) or $250,000 (married).

Effective maximum rate on CFC dividends: 23.8% (20% capital gains + 3.8% NIIT).

Contrast with Ordinary Income

Distributions from contingent commission programs or dealer profit-sharing arrangements are taxed as ordinary income at rates up to 37%, plus the 3.8% NIIT where applicable — an effective maximum of 40.8%.

The tax savings on a $500,000 distribution:

- CFC dividend: $119,000 in tax (23.8% rate)

- Ordinary income: $204,000 in tax (40.8% rate)

- Savings: $85,000

Strategic Timing

Dealer-shareholders control when dividends are declared, which means they can time distributions to reduce their annual tax exposure. Common approaches include:

- Delaying a dividend until a lower-income year

- Coordinating distributions with other business deductions

- Spreading distributions across multiple tax years to stay in lower brackets

A CPA familiar with reinsurance structures can help dealer principals identify the right distribution window — and potentially save tens of thousands of dollars across just a few tax years.

How CFCs Compare to Other Reinsurance Structures on Taxes

CFC vs. NCFC

Non-Controlled Foreign Corporations (NCFCs) are foreign entities where the dealer owns a minority interest and does not control the company. Key differences:

| Feature | CFC | NCFC |

|---|---|---|

| US tax return | Yes (Form 1120-PC) | No |

| Federal excise tax | Exempt under §953(d) | 1% on reinsurance premiums |

| Underwriting profit tax | Excluded under §831(b) | Not taxed at entity level |

| Shareholder tax exposure | Dividends taxed as qualified | Subpart F or ordinary income |

The 1% federal excise tax on NCFC premiums is an ongoing cost. A dealer ceding $1.5 million annually pays $15,000 in FET every year. Over 10 years, that's $150,000 in non-recoverable tax cost.

CFCs avoid this entirely because the §953(d) election treats the company as domestic.

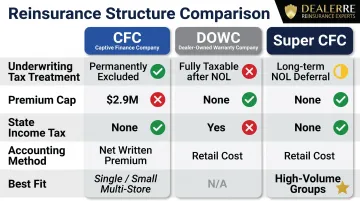

CFC vs. DOWC

Dealer-Owned Warranty Companies (DOWCs) are domestic C-Corps taxed under Subchapter L. Key differences:

| Feature | CFC with §831(b) | DOWC |

|---|---|---|

| Entity type | Offshore corp, §953(d)-elected | Domestic US C-Corp |

| Tax filing | Federal only | Federal + state |

| Underwriting income | Permanently excluded | Fully taxable after NOL exhaustion |

| Accounting method | Net written premium | Retail cost accounting |

| Premium cap | $2.9M (2026) | None |

| State income tax | None | Yes (varies by state) |

DOWCs use retail cost accounting, which generates large initial net operating losses by expensing dealer commissions and admin fees upfront. This creates tax deferral for 5-7 years, but once the NOL is exhausted, the DOWC pays full corporate tax on underwriting profit plus state income tax.

By contrast, CFCs offer:

- Permanent exclusion of underwriting profit (not just deferral)

- No state income tax exposure

- Simpler ongoing compliance with no retail accounting requirements

CFC vs. Super CFC

The Super CFC uses retail accounting and NOL deferral instead of the §831(b) election, eliminating the annual premium cap. Key differences:

| Feature | CFC (§831(b)) | Super CFC |

|---|---|---|

| Premium cap | $2.9M (2026) | None |

| Tax treatment | Permanent exclusion | Long-term NOL deferral |

| Accounting | Net written premium | Retail cost |

| State tax | None | None |

The Super CFC suits high-volume dealer groups whose F&I production exceeds the §831(b) cap — trading permanent exclusion for unlimited premium capacity with multi-year tax deferral.

For most single-rooftop and small multi-store groups producing under $2.9 million annually, the traditional CFC with §831(b) delivers the highest tax efficiency.

Frequently Asked Questions

How is a CFC taxed?

A CFC elects under §953(d) to be treated as a US domestic corporation, files Form 1120-PC annually, and takes the §831(b) election to exclude underwriting profit from taxable income. Only investment income earned on reserve assets is taxed, at the 21% corporate rate.

How is the CFC charge calculated?

Apply the 21% corporate rate to net investment earnings only — specifically interest, dividends, and capital gains earned during the tax year. Underwriting profit is excluded under §831(b) before the calculation begins, so claims experience and premium volume don't factor into the taxable base.

What is exempt CFC income?

Exempt CFC income refers to underwriting profit (premiums earned minus claims paid), which is permanently excluded from taxable income under §831(b) as long as the company stays within the annual net premium threshold of $2.9 million (2026).

What is the federal excise tax on reinsurance?

The federal excise tax is 1% on reinsurance premiums paid to foreign insurers that do not file US tax returns. CFCs avoid this tax because the §953(d) election treats the company as a US taxpayer. NCFCs remain subject to it.

What is the purpose of the CFC rule?

The Subpart F rules were designed to prevent US taxpayers from deferring income by sheltering it in foreign corporations. The §953(d) election allows dealer CFCs to voluntarily enter the US tax system, eliminating Subpart F exposure and providing clear regulatory standing for shareholders.

What is a super CFC?

A Super CFC is an industry term for an offshore reinsurance structure that uses retail cost accounting and net operating loss deferral instead of the §831(b) election. That approach eliminates the annual premium cap entirely, making it a better fit for dealers with high F&I volume who would otherwise exceed the $2.9 million threshold.