Introduction

When a dealer's F&I premium volume outgrows the $2.9 million ceiling imposed by the IRS 831(b) small insurance company election, the next step is often a Non-Controlled Foreign Corporation (NCFC). This offshore reinsurance participation structure lets dealers capture underwriting and investment income from the F&I products they sell — without the annual premium cap that constrains other structures.

Many dealers make that move once they've exhausted the Controlled Foreign Corporation (CFC) model. The mechanics of the NCFC, however, are where the clarity often breaks down.

The NCFC is widely used among larger dealer groups, but confusion persists around how income is taxed, what filings are required, and how post-TCJA rules apply. The Tax Cuts and Jobs Act of 2018 introduced GILTI (Global Intangible Low-Taxed Income) provisions that significantly reduced the deferral benefits NCFCs once offered.

According to a 2018 Protective Asset Protection survey, 43% of dealer executives were unaware of how the new tax laws affect their reinsurance accounting. This guide breaks down how the NCFC structure works, how income flows through it, and what dealers need to know to use it compliantly under current law.

Key Takeaways

- An NCFC is an offshore reinsurance company — dealers participate through preferred shares with limited operational control, not as officers or directors

- NCFC income is subject to 1% federal excise tax under IRC Section 4371, not a standard U.S. corporate tax return

- No annual premium cap makes it useful for high-volume dealers exceeding the $2.9 million 831(b) limit

- TCJA's GILTI provisions can expose individual NCFC shareholders to ordinary income tax rates as high as 37%

- Dealers weighing NCFC vs. 831(b) must account for GILTI exposure — the tax savings can disappear without the right setup

What Is the NCFC Tax Structure?

An NCFC is a multi-owner foreign corporation, typically incorporated offshore, in which the dealer holds preferred shares but is not a common shareholder, officer, or director. This structural distinction makes it "non-controlled" under U.S. tax law because no single U.S. shareholder or group of related shareholders owns enough of the company to trigger CFC classification.

Under IRC Section 957(a), a foreign corporation becomes a CFC when U.S. shareholders own more than 50% of voting power or value. For insurance income, Section 957(b) lowers the threshold to more than 25% ownership. To avoid crossing these thresholds, NCFCs typically require at least 11 unaffiliated U.S. participating shareholders or actual foreign owners, according to GPW and Associates, a reinsurance administration firm.

The NCFC is designed to let dealers participate in underwriting profits and investment income generated by F&I contracts they already sell. Premiums are ceded to the NCFC monthly with no annual cap on contributions.

The key structural differences from a CFC include:

- Ownership role: The dealer holds preferred shares only — no common stock, no officer or director title

- Governance: Control rests with a board shared across all participating dealers, not a single owner

- Tax treatment: NCFCs fall outside the IRS 831(b) election framework, which allows CFCs to exclude up to $2.9 million in annual premiums from taxable income (2026 limit)

- Decision-making: No single dealer can direct the company's underwriting or investment decisions unilaterally

That shared governance is what keeps the structure "non-controlled" — and it's also what determines how the IRS treats the income flowing back to each participating dealer.

Why Auto Dealers Use the NCFC Structure

The primary driver for choosing an NCFC is scale. Dealers whose annual F&I premium volume exceeds the 831(b) cap cannot fully benefit from a CFC alone, and the NCFC provides a path to continue capturing underwriting income without that ceiling. For context, the IRS raised the Section 831(b) annual premium limit to $2.9 million for tax year 2026, up from $2.85 million in 2025. Once a dealership surpasses this threshold, the traditional CFC tax advantages disappear, making alternative structures necessary.

The NCFC distributes risk across a pool of unaffiliated dealers, which stabilizes loss ratios and reduces the impact of any single dealership's claims experience on overall returns. An experienced administrator acts as a gatekeeper — approving new participants and managing the shared risk profile to protect pool quality.

That structure creates concrete advantages for participating dealers:

- More predictable claims environment compared to a single-dealer CFC

- Greater capacity for investment strategies backed by a pooled premium base

- Reduced exposure to outlier claims from any one participant

Industry data confirms the structure's prevalence. A 2019 Digital Dealer report referencing a Protective Asset Protection survey indicated that more than half of the dealer groups surveyed currently participate in offshore reinsurance structures. Yet the same firm's October 2018 survey found that 43% of dealer executives were unaware of how tax law changes affect their reinsurance programs. For dealers evaluating the NCFC today, that knowledge gap is exactly the kind of exposure a qualified administrator can help close.

How the NCFC Tax Structure Works

Under an NCFC structure, a portion of each F&I contract premium is ceded monthly to the offshore reinsurance entity — with no annual cap on the amount ceded, unlike a CFC. Once inside the NCFC, those funds serve three core functions:

- Holds reserves to pay future claims as they arise

- Invests surplus according to board-approved investment policies

- Captures underwriting profit that would otherwise go to a third-party provider

Excise Tax Obligation

Unlike a CFC, an NCFC does not file a standard U.S. corporate income tax return. Instead, reinsured premiums flowing into the NCFC are subject to a federal excise tax. Under IRC Section 4371(3), the rate is 1 cent on each dollar of reinsurance premium, or a 1% excise tax. This is a permanent cost layer that dealers must factor into program economics.

Exemptions exist under certain bilateral income tax treaties, but most common NCFC domiciles do not qualify. The IRS confirms that Bermuda and Barbados treaties do not exempt Section 4371 excise tax for periods after December 31, 1989. Countries with valid treaty exemptions include Ireland, Israel, Japan, Mexico, the Netherlands, Switzerland, and the United Kingdom, but dealers rarely domicile NCFCs in these jurisdictions.

Shareholder Disclosure Requirements

While the NCFC itself does not file a U.S. tax return, individual dealer-shareholders are still subject to additional reporting requirements on their personal income tax returns related to ownership in a foreign corporation. This is a compliance obligation often underestimated by participating dealers, and failure to meet these disclosure requirements can result in penalties.

Subpart F and GILTI Implications

The Tax Cuts and Jobs Act of 2018 introduced GILTI rules under IRC Section 951A and expanded Subpart F income provisions that can affect passive foreign income earned through structures like the NCFC. Income that was previously deferred offshore may now be subject to current U.S. taxation depending on the dealer's specific circumstances.

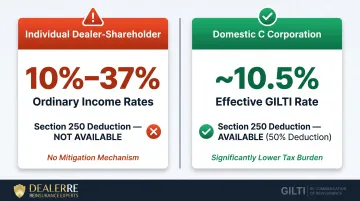

The rate treatment differs significantly depending on how the dealer holds their NCFC shares:

| Shareholder Type | GILTI Rate | Section 250 Deduction Available? |

|---|---|---|

| Individual dealer-shareholder | 10%–37% (ordinary income rates) | No |

| Domestic C corporation | ~10.5% (after 50% deduction) | Yes |

Thomson Reuters confirms that "the tax rate for GILTI is based on the individual's income tax bracket, which means the rate can range from 10% to 37%." Corporate shareholders, by contrast, can claim a 50% deduction under Section 250, reducing their effective GILTI rate to approximately 10.5%. This deduction is only available to domestic C corporations — putting dealer principals who hold NCFC shares personally at a significant tax disadvantage compared to corporate structures.

A GILTI high-tax exclusion is available under final Treasury regulations T.D. 9902 when the effective foreign tax rate exceeds 18.9% (90% of the 21% U.S. corporate rate). However, most offshore reinsurance domiciles impose minimal or zero tax, making this exclusion unavailable in typical NCFC structures.

Taken together — the 1% excise tax, GILTI exposure at ordinary income rates, and shareholder disclosure obligations — the NCFC tax picture is more layered than most dealers initially expect. DealerRE manages all legal forms, filings, and tax returns on behalf of dealer clients, working directly with insurance tax specialists to keep programs compliant and flag issues before they become IRS problems.

Key Tax Factors and NCFC vs. CFC Comparison

Structural Tax Difference

A CFC qualifies for the 831(b) small insurance company election, which allows up to $2.9 million in annual premiums (2026) to be excluded from taxable income, and investment income is taxed at favorable rates. The NCFC has no such cap but is subject to 1% excise tax on premiums and does not benefit from the 831(b) election. Each structure carries distinct volume thresholds and tax profiles — neither is universally superior.

Distribution Treatment

Dealers can receive distributions from an NCFC without redeeming shares, which offers some liquidity flexibility. However, the tax treatment of those distributions depends on how the income has been characterized. Under IRC Section 1248, when a U.S. person sells or exchanges stock in a foreign corporation and owns 10% or more of the voting stock, gain is recharacterized as ordinary dividend income to the extent of accumulated earnings. For NCFC preferred shareholders who own less than 10%, capital gain treatment may apply, but this depends on specific ownership structure and applicable attribution rules.

Post-TCJA Impact

Prior to 2018, the NCFC was popular partly because offshore income could be deferred. Post-TCJA, GILTI and updated Subpart F rules reduced that deferral advantage significantly.

Rosenfield & Co noted in November 2018 that "the TCJA expanded the definition of a U.S. Shareholder and as such, more of these programs will be ineligible to be considered a NCFC." The TCJA changed the definition to include ownership by value (not just voting power), which undermines some NCFC structures that relied solely on voting control thresholds to avoid CFC classification.

Investment Policy Differences

Because NCFC boards manage pooled assets across multiple dealers, investment decisions are made collectively. JMA Group states the NCFC has a "stronger investment policy statement" that allows for more aggressive investment strategies and potentially higher returns. However, this removes individual dealer control over investment allocation. Dealers who prefer direct access to reserves and unilateral investment decisions may find the shared governance structure limiting.

State Compliance Variable

Beyond investment governance, the regulatory environment at the state level adds another layer of structural complexity. F&I products are regulated at both federal and state levels, and a dealer's domicile state can affect whether an NCFC structure delivers the expected benefits or creates additional legal exposure. What works in one state may not be permissible or advantageous in another, requiring you to get qualified legal review before committing to an NCFC.

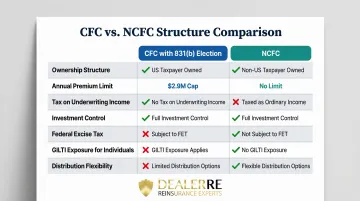

| Factor | CFC (with 831(b) Election) | NCFC |

|---|---|---|

| Ownership | Single dealer/dealer group; 100% control | Multiple unaffiliated dealers (11+ shareholders) |

| Annual Premium Limit | $2.9M (2026) under 831(b) | No statutory premium limit |

| Tax on Underwriting Income | $0 under 831(b) election | Subject to corporate tax at entity level |

| Investment Control | Dealer controls investment policy | Board of Directors controls; potentially more aggressive strategies |

| Federal Excise Tax | Avoided if 953(d) election made (treated as domestic) | 1% under IRC 4371(3) |

| GILTI Exposure (Individuals) | Mitigated via 953(d) domestic election | Full ordinary income rates (10-37%) |

| Distribution Flexibility | Full control; redemption of shares | Distributions without share redemption possible via preferred shares |

Common Misconceptions and When NCFC May Not Be Appropriate

Misconception: NCFC Eliminates U.S. Tax Exposure Entirely

Many dealers assume the NCFC functions like a tax shelter that eliminates U.S. tax exposure entirely. That's not accurate. The 1% excise tax still applies to reinsured premiums, shareholders must still file personal tax disclosures, and post-TCJA, offshore deferral benefits are reduced compared to what they were before 2018.

Individual shareholders face GILTI inclusion at their full marginal ordinary income tax rate — potentially as high as 37%.

Misconception: Exceeding the 831(b) Cap Means NCFC Is the Obvious Next Step

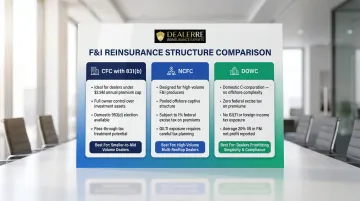

Exceeding the 831(b) cap does not automatically make an NCFC the best choice. Other structures such as a Dealer-Owned Warranty Company (DOWC) or a second CFC may be better suited depending on the dealer's control preferences, tax profile, and state regulations.

Protective Asset Protection, self-described as the originator of the DOWC, reports that dealers using a DOWC structure see an average 20% lift in F&I profits.

The DOWC is a domestic C-corporation that acts as the obligor for service contracts — and avoids the federal excise tax and offshore compliance complexity entirely.

When NCFC Is Not Appropriate

- Smaller-volume dealers who fit within the 831(b) cap have little reason to accept the complexity and reduced control of an NCFC

- Dealers who require direct access to and control over their funds may find the shared governance structure limiting

- Dealers uncomfortable with offshore structures or heightened post-TCJA reporting obligations should consider domestic alternatives before committing to an NCFC

IRS Compliance Clarity

That said, the regulatory landscape for dealer reinsurance structures has improved. On January 14, 2025, the IRS issued final regulations establishing a "Seller's Captive" exception for F&I reinsurance companies meeting four criteria, including that at least 95% of business comes from contracts purchased by customers unrelated to the dealership.

Compliant structures now have clearer regulatory standing and are exempt from Form 8886 reporting under Notice 2016-66 — meaning dealers in qualifying programs no longer face the disclosure requirements that previously added administrative overhead.

Frequently Asked Questions

What is a non-controlled foreign corporation?

An NCFC is an offshore corporation in which the U.S. dealer holds shares but does not have controlling ownership or management authority. To avoid CFC classification, NCFCs typically require at least 11 unaffiliated U.S. shareholders, ensuring no single shareholder or related group exceeds the 50% (or 25% for insurance income) ownership threshold.

What is the tax rate for a non-resident foreign corporation receiving reinsurance premiums?

The federal excise tax under IRC Section 4371(3) is 1% of reinsurance premiums paid to foreign reinsurers. The NCFC does not file a U.S. corporate income tax return, but this excise tax applies to each dollar of premium ceded to the offshore entity.

What are the exceptions to Subpart F?

Two exceptions are most relevant to NCFC reinsurance income: the high-tax exception under IRC Section 954(b)(4) (applies when foreign tax rates exceed 18.9%) and the qualified active insurance business exception. Whether either applies to your specific structure depends on how the NCFC is set up — your tax advisor can confirm which exceptions are available given your arrangement.

How does an NCFC differ from a CFC for auto dealers?

A CFC gives the dealer direct control and access to the 831(b) election, but carries an annual premium cap ($2.9M in 2026). The NCFC pools multiple dealers offshore, removing that cap — but individual control is reduced and the tax treatment shifts to a 1% federal excise tax rather than the 831(b) exclusion.

What did the Tax Cuts and Jobs Act change for NCFC structures?

TCJA introduced GILTI provisions and tightened Subpart F rules, reducing the offshore deferral benefits that previously made NCFCs attractive. Individual shareholders now face GILTI inclusion at full ordinary income rates (up to 37%). On top of that, TCJA's expanded definition of "U.S. shareholder" caused some NCFCs to inadvertently cross CFC classification thresholds.

Can auto dealers access their funds held in an NCFC?

Unlike dealer-controlled structures, NCFC distributions are decided at the board level — individual dealers don't control the timing. That said, dealers can generally receive distributions without redeeming their shares, which provides some liquidity within the pooled governance structure.