Introduction

Dealer-owned reinsurance lets dealerships retain underwriting profits from F&I products, build equity, and create long-term wealth. But ownership alone isn't enough. Operating a reinsurance company carries a precise set of IRS, financial, and state-level reporting obligations — and dealers without a dedicated administrator often miss them.

The regulatory landscape shifted significantly in January 2025 when the IRS finalized new micro-captive reporting regulations, replacing the outdated framework dealers had relied on for nearly a decade. Dealers who continue filing forms based on obsolete guidance may be creating unnecessary audit exposure, while those who fail to file when required face strict penalties exceeding $200,000 per entity per year.

Getting this right requires understanding exactly what's changed — and what's at stake if you don't. This guide covers the 2025 IRS reporting rules, financial and state-level obligations, the most common compliance mistakes dealers make, and how a full-service administrator keeps every filing accurate and on time.

Key Takeaways

- The 2025 IRS micro-captive regulations replaced Notice 2016-66 with new definitions for who must file Form 8886

- Many dealer reinsurance structures using admin obligor models may not meet the "Insured" or "Captive" definitions — making them exempt from filing requirements entirely

- Dealers must receive quarterly financials, product-level performance reports, loan/dividend records, and investment reporting; on-demand summaries alone don't satisfy this obligation

- State reporting differs widely by domicile: Vermont requires $250,000 minimum capital, Tennessee mandates March 15 annual filings, and offshore CFCs trigger Form 5471 requirements

- Filing Form 8886 under the obsolete Notice 2016-66 invites unnecessary IRS scrutiny; every program needs its own evaluation

Why Reinsurance Reporting Requirements Matter for Auto Dealers

Non-compliance with IRS, state, or financial reporting requirements can expose dealers to penalties, loss of tax advantages, and heightened regulatory scrutiny. The same profit engine that builds wealth can become a costly liability if reporting is neglected.

The IRS's newly finalized micro-captive regulations, published in January 2025, replaced Notice 2016-66 and reset the criteria for determining which dealer reinsurance programs trigger reporting obligations. Dealers with existing programs — or those considering one — must understand exactly what reporting applies to their structure.

The IRS Large Business & International (LB&I) division maintains an active compliance campaign specifically targeting micro-captive insurance arrangements. This campaign continues to operate under the Enterprise Activities practice area, signaling ongoing enforcement priority. In 2019, the IRS mailed settlement offers to up to 200 taxpayers under audit for abusive micro-captive transactions, and promoter penalties have been assessed against those marketing questionable programs.

Accurate reporting does more than satisfy regulators. Dealers who stay current on their obligations can:

- Track program performance and loss ratios against benchmarks

- Make informed decisions about F&I product reserves

- Demonstrate legitimacy to auditors, lenders, and potential buyers

- Identify early warning signs before they become costly corrections

Dealers who treat reporting as an operational discipline — not a once-a-year scramble — run stronger, more defensible programs.

IRS Reporting Requirements: The 2025 Micro-Captive Regulations and Form 8886

Understanding Who Qualifies as an "Insured" Under the 2025 Regulations

The IRS finalized new reporting regulations in Treasury Decision 10029, published January 14, 2025, in the Federal Register. These regulations created two new regulatory sections — 26 CFR 1.6011-10 (listed transactions) and 26 CFR 1.6011-11 (transactions of interest) — and officially obsoleted Notice 2016-66.

The "Insured" definition uses a three-part test — all conditions must be satisfied simultaneously:

- The entity must conduct a trade or business

- The entity must be a party to the contract entered into with the captive or intermediary

- The entity must treat amounts paid under the contract as insurance premiums for federal income tax purposes

Key implication for dealer reinsurance programs: In most admin obligor structures, the dealer is not the party to the contract with the customer. The dealer facilitates the contract, but the customer contracts directly with the product obligor. If the dealer does not meet the definition of "Insured," the regulations do not apply and no Form 8886 filing is required.

If the dealer does qualify as an Insured under that test, the next question is whether the reinsurance entity itself meets the definition of a "Captive."

Understanding Who Qualifies as a "Captive" Under the 2025 Regulations

The "Captive" definition also requires three elements:

- The entity must be an insurance company with an 831(b) election in place

- The entity must issue or reinsure a contract to an Insured

- At least 20% common ownership must exist between the captive and the Insured or related parties

If a dealer's reinsurance company does not satisfy all three components, it is not classified as a captive under these regulations and has no Form 8886 filing requirement. For many dealer reinsurance programs, this is the end of the analysis — no further review required.

The Consumer Coverage Exception — and Why It Matters

Even if a dealer's entity qualifies as both an Insured and a Captive, one more protection applies. The regulations include a four-part Consumer Coverage Exception designed specifically for captives insuring third-party customer risks. All four conditions must be met:

- More than 50% common ownership between the captive and the seller

- No enterprise risk present in the captive (the captive does not insure the dealer's own business risks)

- 100% of the captive's business covers products or services sold by the seller or related persons

- More than 95% of total ceded risk insures customers unrelated to the seller

If a dealer's reinsurance entity meets all four conditions of the Consumer Coverage Exception, no Form 8886 filing is required. Properly structured dealer reinsurance companies that exclusively reinsure VSC, GAP, and ancillary products sold to unrelated retail customers will qualify for this exemption.

Critical caution: Dealers who have been continuing to file Form 8886 based on the now-obsolete Notice 2016-66 — simply because "it's always been filed" — may be making an error that unnecessarily places them under IRS scrutiny. The 2025 regulations replaced that framework entirely. If your program has not been reviewed against the new definitions and exceptions, now is the time to do that — before the next filing cycle.

Financial and Operational Reporting Requirements Inside Your Reinsurance Company

Beyond IRS filings, dealers have ongoing internal and administrative reporting obligations. At minimum, a trusted administrator should provide complete financial statements for the reinsurance entity on a quarterly basis, covering income, reserve levels, and underwriting results. Single-page summaries available only upon request are insufficient.

Product Performance Reporting

Dealers should receive a breakdown of claims by product type, individual claim records, cancellation activity, and loss ratios. This data is essential not just for compliance but for managing which F&I products are performing well and which carry excessive risk. Without detailed product-level reporting, dealers cannot make informed decisions about pricing, coverage terms, or whether to continue offering specific products.

Loan and Dividend Record-Keeping

If a dealer has borrowed against unearned or earned premiums — a common feature of well-structured programs — all loan balances, interest accrual, and repayment must be properly documented. Your administrator must track and record dividend distributions to support tax compliance and program oversight.

The IRS's new regulations specifically identify loan-back arrangements as a "Financing Factor" that can trigger reportable transaction classification. This makes thorough loan and dividend documentation non-negotiable, not just good practice.

Investment Reporting

Dealers whose reinsurance entities invest premium reserves need documentation of:

- Investment activity and returns

- Allocation between required reserves and distributable surplus

- Compliance with program investment guidelines

For Controlled Foreign Corporation (CFC) structures, this documentation carries extra weight — investment flexibility is one of the CFC's primary advantages, and without clear allocation records, dealers cannot accurately determine what capital is available for distribution versus held in reserve.

Annual Tax Filing for the Reinsurance Entity

Filing deadlines and structure-specific rules mean the reinsurance entity needs its own tax return prepared by CPAs with specialized experience in 831(b) structures. DealerRE partners with experienced CPAs and legal counsel to ensure IRS compliance and proper return preparation, taking this burden off the dealer's plate while ensuring accuracy. It's important to engage independent legal and accounting professionals — not solely the administrator — to maintain proper oversight.

State-Level and Structure-Specific Reporting Obligations

State insurance departments may impose their own registration, licensing, or surplus lines filing requirements depending on where the reinsurance entity is domiciled and in which states it operates. Requirements vary significantly by state, and dealers should work with compliance professionals familiar with their specific domicile and operating states.

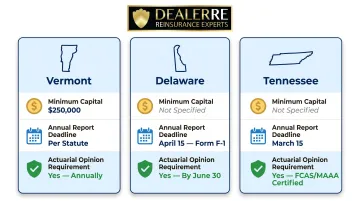

Domestic Captive Domicile Requirements

| State | Minimum Capital | Annual Report Deadline | Actuarial Opinion Required |

|---|---|---|---|

| Vermont | $250,000 (8 VSA 6004) | Per statute | Yes, annually |

| Delaware | Not specified | April 15 (Form F-1) | Yes, by June 30 |

| Tennessee | Not specified | March 15 | Yes, FCAS/MAAA certified |

Structure matters for state reporting. A Controlled Foreign Corporation (CFC) domiciled offshore in a jurisdiction like the Cayman Islands or Turks and Caicos Islands has different state-level reporting considerations than a domestic Dealer Owned Warranty Company (DOWC).

In certain states, DOWCs may be regulated as insurance companies and subject to state insurance department oversight, capital requirements, or annual filings.

Offshore Captive (CFC) — Form 5471 Requirements

Beyond state-level obligations, offshore structures carry a separate federal layer. U.S. shareholders of offshore captive insurance companies that have not made a section 953(d) election face Form 5471 filing obligations. Penalties for failure to file are substantial:

- $10,000 per failure to file a complete and correct Form 5471

- If not filed within 90 days after IRS notice, an additional $10,000 per 30-day period (up to $50,000 maximum continuation penalty)

Cayman Islands or other offshore captive owners must verify Form 5471 compliance annually.

BHPH Dealer Considerations

For BHPH dealers, admin obligor reinsurance programs covering mechanical breakdown often carry additional state-level obligations that stack on top of standard reinsurance reporting. These may include:

- Consumer protection statutes governing service contract disclosures

- State warranty or service contract licensing requirements

- Separate annual filings with the state insurance or consumer affairs department

DealerRE manages the forms, filings, and renewals that keep BHPH dealer reinsurance programs in good standing across these layered state and federal requirements.

Common Reinsurance Reporting Mistakes Auto Dealers Make

Continuing to File Form 8886 Under Obsolete Notice 2016-66

The most costly IRS mistake is continuing to file Form 8886 under the now-obsolete Notice 2016-66 after the 2025 regulations changed the rules. This can place dealers in a scrutinized category unnecessarily. Each program must be individually tested against the new definitions before deciding whether to file.

The IRS provided a limited penalty waiver through Notice 2025-24, extending the disclosure deadline to July 31, 2025, but that deadline has now passed. Dealers who missed it face full penalty exposure.

Accepting Inadequate Financial Reporting

Dealers who receive only minimal or infrequent reports cannot properly track program health, identify underperforming products, or make informed decisions about distributions. A complete quarterly report should include:

- Detailed financial statements (income, reserves, underwriting results)

- Product-level claim breakdowns and loss ratios

- Individual claim records and cancellation activity

- Loan balances, interest accrual, and dividend distributions

- Investment activity and allocation between reserves and surplus

The Captive Insurance Companies Association recommends financial reports produced at least twice per year in accordance with GAAP, STAT, or IFRS, in auditable form.

Including Enterprise Risk in the Reinsurance Entity

Including enterprise risk — coverage for the dealer's own business risks rather than customer-facing products — creates three compounding problems:

- Disqualifies the Consumer Coverage Exception

- Triggers Form 8886 filing obligations

- Complicates both IRS compliance and state insurance treatment

Properly structured reinsurance entities should exclusively reinsure customer-facing F&I products. That structural discipline is also what keeps penalty exposure off the table.

Penalty Exposure for Non-Compliance

Form 8886 penalties are strict liability with no reasonable cause defense. Under IRC Section 6707A:

| Transaction Type | Maximum Penalty per Entity per Year |

|---|---|

| Listed Transactions | $200,000 |

| Transactions of Interest | $50,000 |

These penalties are assessed per failure, per year — calculated at 75% of the tax decrease shown on the return, with the statutory maximums above applied when that figure exceeds the cap.

How a Full-Service Reinsurance Partner Manages Your Reporting Obligations

One of the most significant practical advantages of working with a full-service reinsurance administrator is that they handle legal forms, filings, tax returns, and renewals on behalf of the dealer — removing the administrative and compliance burden while ensuring obligations are met correctly and on time.

What Proper Reporting Support Looks Like

A qualified partner should provide:

- Proactively delivered quarterly financial statements covering income, reserves, and underwriting results

- Product performance analysis with claim breakdowns, loss ratios, and cancellation activity

- Loan and dividend records documenting all financing arrangements and distributions

- Annual tax return support coordinated with independent CPAs experienced in 831(b) structures

- Investment reporting showing allocation between required reserves and distributable surplus

These reports should be reviewed with the dealer regularly, not just made available upon request. Dealers should ask prospective partners exactly what reporting they provide and how often.

DealerRE's Full-Service Administration Model

DealerRE partners with experienced administrators, CPAs, and legal counsel to ensure every reporting obligation is met fully and on time — minimizing audit risk while protecting the dealer's ability to retain underwriting profits long-term.

With 28 years of experience and more than 400 dealers served nationwide, DealerRE gives dealer principals a fully managed compliance infrastructure — so the program runs cleanly in the background while the dealership stays focused on selling cars and building F&I income.

Frequently Asked Questions

What is dealer compliance?

Dealer compliance refers to an auto dealership's adherence to federal, state, and industry regulations governing its operations — including F&I practices, consumer protection laws, and, for dealers with reinsurance companies, IRS reporting and insurance regulatory requirements.

Is reinsurance an asset or liability?

A properly structured dealer-owned reinsurance company is generally considered an asset. It holds premium reserves, generates underwriting and investment income, and represents growing equity. Underfunded or poorly managed programs, however, can create financial exposure.

What is Form 8886 and do most auto dealers with reinsurance need to file it?

Form 8886 is the IRS Reportable Transaction Disclosure Statement for captive insurance arrangements. Under the 2025 micro-captive regulations, many dealer reinsurance companies using admin obligor structures will not meet the definition of "Insured" or "Captive" and are not required to file.

How often should dealers receive reporting on their reinsurance company?

Dealers should receive comprehensive financial statements and product performance reports at least quarterly, proactively provided by their administrator — not available only upon request. These should be reviewed together with a reinsurance specialist at each interval.

What happens if an auto dealer doesn't meet reinsurance reporting requirements?

Missing a required Form 8886 filing can result in penalties up to $200,000 per entity per year and increased IRS scrutiny. Inadequate financial reporting can also mask program losses, trigger unexpected tax consequences, or create state regulatory issues.

Do reporting requirements differ between a CFC and a DOWC reinsurance structure?

Yes, reporting obligations differ by structure. A CFC has specific offshore domicile, IRS foreign corporation reporting (Form 5471), and federal tax considerations, while a DOWC is a domestic entity that may face state insurance department oversight and different regulatory filing requirements depending on state of operation.

Ready to ensure your dealer-owned reinsurance program meets every reporting obligation while maximizing profitability? Contact DealerRE at (804) 824-9533 for a free consultation. DealerRE has been helping dealers build profitable, compliant reinsurance programs since 1994 — handling compliance, reporting, and administration from end to end.