- All 56 U.S. jurisdictions adopted updated credit for reinsurance rules by September 2022, creating nationwide compliance standards

- Dealer-owned reinsurance entities face full state insurance regulation—unlike simply reselling third-party F&I products

- Missing contract provisions like insolvency clauses can disqualify your front carrier from taking regulatory credit, threatening program viability

- Reinsurance agreements must be executed within 9 months of the effective date to avoid restrictive retroactive accounting treatment

- Every front carrier must be verified for NAIC authorization status and financial strength rating before program launch

Introduction

Over 400 auto dealers now operate their own reinsurance companies to capture underwriting profits from vehicle service contracts, GAP insurance, and collateral protection products. Many entered these programs to escape the margins third-party providers take—50-70% of premium dollars. But a compliance reality catches dealers by surprise: when you own a reinsurance entity backing F&I products, you've entered a regulatory framework governed by state insurance law and shaped by National Association of Insurance Commissioners (NAIC) model regulations.

Dealers who simply resell manufacturer or third-party warranties face no insurance regulation. Dealer-owned reinsurance is different. In admin obligor structures—where your reinsurance company assumes risk from a licensed front carrier—you operate under the same statutory framework as commercial insurance companies.

Gaps in compliance don't just risk fines. They can invalidate the regulatory credit your front carrier depends on, collapsing the program's economics and stopping claims payments.

This guide covers:

- What NAIC is and why it governs dealer reinsurance programs

- Which model regulations apply to admin obligor structures

- How provisions like the 9-month execution rule work in practice

- How to verify your front carrier's credentials and financial strength

- Where compliance failures most often occur—and how to avoid them

What Is the NAIC and Why Does It Matter for Dealer-Owned Reinsurance?

The National Association of Insurance Commissioners (NAIC) is the U.S. insurance standards-setting body, composed of state insurance commissioners from all 56 jurisdictions—the 50 states, DC, and five U.S. territories. Founded in 1871, the NAIC provides expertise, data, and model laws to help state regulators protect consumers and maintain sound insurance markets. The NAIC itself does not regulate insurers directly — it creates model laws that each state adopts through its own legislative or regulatory process.

When the NAIC adopts a model law, each commissioner commits to bringing it to their state legislature or regulatory body for adoption. The goal is passage in most states within three years. Once a state adopts an NAIC model, it becomes enforceable law in that jurisdiction.

Why Dealer-Owned Reinsurance Falls Under NAIC Frameworks

Dealer reinsurance structures vary in regulatory treatment:

- Controlled Foreign Corporations (CFCs): Domiciled offshore and licensed as insurance companies in foreign jurisdictions

- Domestic captives: Domiciled in a U.S. state and regulated by that state's Department of Insurance

- Admin obligor programs: The administrative company holds the obligation; most are not regulated as insurers — but when a reinsurance layer is added, the dealer-owned reinsurer operates under insurance regulation in its domicile state

Regardless of which structure you use, the front carrier — the A-rated insurer backing your program — must comply with NAIC credit for reinsurance standards to count your arrangement as an asset on its financial statements. If it can't take credit, it must hold reserves for the full gross liability—eliminating the financial benefit of reinsurance and threatening the viability of your program.

Three specific compliance requirements flow directly from this:

- Your front carrier must be authorized or certified under NAIC standards

- The reinsurance agreement must include specific provisions NAIC models require

- Failure to meet these conditions affects whether the ceding insurer receives regulatory credit—which directly impacts program economics and claims-paying capacity

Key NAIC Model Laws That Govern Dealer Reinsurance Programs

Two model laws define the compliance framework for dealer reinsurance: Credit for Reinsurance Model Law (#785) and Credit for Reinsurance Model Regulation (#786). These establish the conditions under which a ceding insurer can take regulatory credit for risks it transfers to a dealer's reinsurance company.

Credit for Reinsurance: Why It Matters

Credit for reinsurance means the ceding insurer can record the reinsurance as "an asset or a reduction from liability" on its statutory financial statements. Without credit, the carrier must hold reserves for the full gross amount of liabilities—regardless of the reinsurance arrangement. This eliminates the financial benefit and makes the program unsustainable.

Reinsurer Categories Under Model #785

Model #785 creates a tiered system based on the reinsurer's authorization status:

| Category | Collateral Required | Key Requirements |

|---|---|---|

| Licensed (Authorized) | None | Licensed to transact reinsurance in the ceding insurer's state |

| Accredited | None | Accredited by commissioner; licensed in at least one state; $20M+ surplus |

| Certified Reinsurer | 0-100% (based on rating tier) | Certified by commissioner; domiciled in qualified jurisdiction; maintains financial strength ratings |

| Reciprocal Jurisdiction | Generally 0% | Domiciled in jurisdiction subject to U.S. Covered Agreement |

| Unauthorized | 100% | Does not meet any Section 2 requirements |

The distinction matters for dealer programs: an authorized reinsurer faces no collateral requirement, while an unauthorized reinsurer can only receive credit to the extent that actual security—cash, securities, or irrevocable letters of credit—is posted.

For dealers using offshore CFCs or entities not licensed in the front carrier's state, the collateral obligation can create significant cash flow and capital constraints.

Certified Reinsurer Collateral Scale

For certified reinsurers, collateral requirements scale with the reinsurer's rating:

- Secure-1: 0%

- Secure-2: 10%

- Secure-3: 20%

- Secure-4: 50%

- Secure-5: 75%

- Vulnerable-6: 100%

If a certified reinsurer holds less collateral than required, the ceding insurer's allowable credit is reduced by that deficiency.

Universal Adoption Milestone: September 2022

Understanding these collateral tiers is especially important now that the rules apply uniformly across every state. All 56 U.S. jurisdictions adopted the 2019 revisions to Models #785 and #786 by September 2022, with enforcement beginning January 1, 2023. Every dealer-owned reinsurance program now operates under the same standards, regardless of where the front carrier is domiciled.

What this means in practice: Programs structured before 2023 under older state-specific rules should be reviewed against current collateral and credit requirements to confirm they remain compliant.

Clarification: Model #582 Is Not a Reinsurance Regulation

Some references incorrectly cite Model #582 as a credit for reinsurance standard. Model #582 is the Life Insurance Illustrations Model Regulation, which governs consumer disclosures for life insurance policies—it has no relationship to reinsurance and should not appear in reinsurance compliance discussions.

The 9-Month Rule and Other Critical Reinsurance Contract Requirements

The 9-Month Rule Explained

The 9-month rule originates from SSAP No. 62R – Property and Casualty Reinsurance, Paragraph 24, a statutory accounting standard that governs how reinsurance transactions appear on financial statements.

The rule requires: A reinsurance contract must be finalized, reduced to written form, and signed by all parties within nine months of the contract's effective date.

Consequences of noncompliance: The contract becomes subject to retroactive accounting treatment instead of prospective accounting. Retroactive treatment restricts how the ceding insurer recognizes the financial benefit—requiring losses to be recognized immediately in surplus rather than gradually reducing reserves.

This is not a provision within Model #785 or #786—it's an accounting rule with regulatory consequences. The timeline starts on the contract's effective date (commencement date), not when negotiations begin.

For dealers: Ensure your reinsurance agreements are executed well before the nine-month deadline. Delays caused by contract review, signature collection, or administrative lag can trigger accounting treatment that undermines the ceding insurer's financial benefit.

Required Contract Provisions Under Model #786

Model #786 Section 15 mandates specific provisions as absolute conditions for credit. The regulation states credit "shall be allowed only when" these provisions appear.

Insolvency Clause (Section 15A):

The reinsurance must be payable to the ceding insurer or its liquidator, receiver, or statutory successor based on the ceding insurer's liability. This applies without reduction due to the ceding insurer's insolvency or the liquidator's failure to pay claims.

In plain terms: if your front carrier becomes insolvent, your reinsurance company still owes claims directly to policyholders or the receiver managing the insolvency. This protects consumers and preserves the integrity of the reinsurance arrangement.

Two additional provisions are required:

- Books and Records Access — Certified reinsurers must give the insurance commissioner free access to all books and records, with the right to examine them at the commissioner's discretion.

- Consequence of noncompliance — If the insolvency clause is absent or incorrectly drafted, the ceding insurer cannot take credit. No exceptions. A contract that is otherwise perfectly structured but missing this clause fails to qualify.

Additional Contract Requirements Under SSAP No. 62R

Qualifying reinsurance agreements must:

- Provide for reports of premiums and losses, and payment of losses, no less frequently than quarterly

- Contain no guarantee of profit, directly or indirectly, from either party

- Transfer significant insurance risk—both underwriting and timing risk—with a reasonably possible chance of significant loss to the reinsurer

Without all three, the arrangement may be reclassified as a financial accommodation rather than legitimate reinsurance—which eliminates the accounting and credit benefits your program depends on.

How to Verify Your Insurer's NAIC Standing and Credentials

What Is an NAIC Company Code?

Every insurance company operating in the U.S. is assigned a unique five-digit NAIC company code (also called an NAIC number). Examples include 26263, 16810, or 12831. This number allows you to confirm the company's licensure status, financial filings, and regulatory standing.

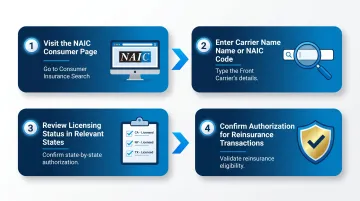

Using the NAIC Consumer Insurance Search Tool

The NAIC maintains a free, publicly accessible Consumer Insurance Search tool. You can search by company name or NAIC code to access:

- State licensing and authorization status

- Complaint data

- Financial health indicators

- Regulatory actions or sanctions

How to use it:

- Visit the NAIC Consumer page and select the insurance search tool

- Enter the carrier name or NAIC company code

- Review the results for licensing status in your state and the ceding insurer's domicile state (the state where the insurer is incorporated)

- Confirm the company is authorized to accept reinsurance in the relevant jurisdictions

Understanding Authorized vs. Unauthorized Status

An authorized company holds a license to do business in a given state. An unauthorized company does not — and that distinction carries real consequences in reinsurance.

When a reinsurer is authorized in the ceding insurer's domicile state, collateral requirements are eliminated. Unauthorized reinsurers typically must post letters of credit or trust funds to satisfy state credit-for-reinsurance rules. Note that this authorization applies specifically to reinsurance transactions, not to direct consumer sales.

AM Best Financial Strength Ratings: A Separate Credential

An AM Best Financial Strength Rating (FSR) is an independent opinion of an insurer's financial strength and ability to meet ongoing policy obligations. It's a credit rating, not a regulatory status.

Rating categories:

- A++ / A+ (Superior): Superior ability to meet ongoing obligations

- A / A- (Excellent): Excellent ability to meet obligations

- B++ / B+ (Good): Good ability; financial strength vulnerable to adverse changes

- B / B- (Fair): Fair ability; financial strength vulnerable

- C++ and lower: Marginal to poor ability; very vulnerable

When industry references cite an "A-rated" carrier, this typically means A- or higher—falling within the "Excellent" or "Superior" categories.

AM Best FSR and NAIC standing are complementary but serve different purposes. FSR assesses financial capacity; NAIC standing reflects licensure and regulatory authorization. Verify both independently when evaluating a front carrier.

What Dealers Should Ask Their Reinsurance Provider

Once you understand these two credentials, use them as a checklist when vetting any front carrier. Any reputable reinsurance administrator should supply:

- NAIC company codes for all front carriers used in your program

- Documentation of carrier authorization status in all states where you operate

- Current AM Best ratings

- Explanation of how the carrier's authorization status affects collateral requirements and program structure

DealerRE manages all legal forms, filings, tax returns, and renewals, and works exclusively with A-rated insurers. If your current administrator can't answer these questions clearly at onboarding, that's a red flag worth taking seriously.

Common NAIC Compliance Gaps That Put Dealer Reinsurance Programs at Risk

Administrative Neglect: Failing to Manage Ongoing Filings

The most common compliance failure occurs when dealers set up reinsurance programs with providers that don't manage ongoing regulatory filings, tax returns, and renewals. Initial setup may be compliant, but if quarterly cession statements, annual financial reports, and license renewals aren't maintained, the program drifts out of compliance without the dealer's knowledge.

The risk: State examiners conducting financial reviews can disqualify credit for reinsurance retroactively if required filings or documentation are missing—forcing the ceding insurer to restate reserves and threatening the program's financial viability.

Working with a full-service administrator — one that manages all legal forms, filings, tax returns, and renewals on your behalf — is the most reliable way to prevent this kind of drift.

Program Structure Mismatch

Administrative compliance is only part of the equation. The underlying structure of your reinsurance program has to fit your business — and that fit can shift over time.

Some dealers operate in the wrong structure for their volume, domicile state, or growth trajectory. A structure that was compliant at setup may fall outside NAIC requirements as the business changes: premium volume exceeds thresholds, multi-state expansion occurs, or the front carrier updates its collateral requirements.

Reinsurance structures include:

- NCFC (Non-Controlled Foreign Corporation)

- CFC (Controlled Foreign Corporation)

- Retro (retrospective reinsurance agreements)

- Admin obligor

Each carries different compliance obligations under NAIC frameworks, state licensing rules, and IRS tax treatment.

If you haven't reviewed your program structure in the last 24 months — or your sales volume has grown 25% or more — request a structure analysis. What was optimal at launch may no longer fit where your dealership stands today.

Documentation Gaps: Missing or Inadequate Records

Beyond structure, documentation quality determines how programs hold up under regulatory scrutiny. Failing to maintain cession statements, loss run reports, and contract documentation in the format regulators expect is one of the most common reasons programs face examination issues.

Required documentation includes:

- Quarterly cession statements showing premiums ceded and losses reported

- Loss run reports detailing claims paid, reserves held, and outstanding liabilities

- Premium remittance schedules confirming payment from dealer to reinsurer

- Executed reinsurance agreements with all required provisions

- Annual financial statements prepared according to statutory accounting principles

Compliance is an ongoing operational requirement, not a one-time event at program launch. Regulators examining the ceding insurer will request these records — and gaps or inconsistencies can disqualify credit.

The most practical safeguard: work with an administrator that produces and maintains these records automatically as part of their service model. DealerRE's full-service administration covers all required documentation, keeping dealer programs audit-ready without adding operational burden to the dealership.

Frequently Asked Questions

What is reinsurance in the auto industry?

Reinsurance in the auto industry refers to a dealer-owned or third-party arrangement where underwriting risk on F&I products like vehicle service contracts, GAP insurance, or collateral protection is transferred from a primary insurer to a reinsurance company. This allows dealers to participate in the underwriting profit rather than sending it to third-party product providers.

What does the NAIC do and what reinsurance guidelines apply to auto dealers?

The NAIC sets model insurance laws adopted by all 50 states and U.S. territories. For auto dealers operating reinsurance companies, the most relevant guidelines govern how the front carrier can take credit for ceded risk, what collateral must be held, and what contract provisions must be present for a legally recognized reinsurance agreement.

Which NAIC model regulations govern reinsurance (for example, Credit for Reinsurance Model #785 and Model #786)?

Credit for Reinsurance Model Law #785 and Model Regulation #786 are the primary frameworks. They set standards for authorized and certified reinsurer status, collateral requirements, and mandatory contract provisions. Dealers should confirm which models their state has adopted, as supplemental models may apply depending on jurisdiction.

What is the 9-month rule for reinsurance contracts?

The 9-month rule, found in SSAP No. 62R Paragraph 24, requires that a reinsurance contract be finalized and signed within nine months of the contract's effective date. Contracts executed outside this window fall under retroactive accounting treatment, limiting how the ceding insurer can recognize the financial benefit on statutory financial statements.

How do I find an insurer's NAIC company code (e.g., 26263, 16810, 12831)?

Visit the NAIC's free Consumer Insurance Search tool at naic.org and enter the carrier's name or NAIC code to view licensure status, state authorizations, and financial filing history. Verify this for any insurer fronting your reinsurance program before signing.

A dealer-owned reinsurance company creates real profit advantages, but only when structured and administered within the NAIC-governed regulatory framework. Missing contract provisions, delayed execution timelines, or inadequate documentation can disqualify the regulatory credit your front carrier depends on, threatening the program's financial viability.

DealerRE has helped over 400 auto dealers build compliant, profitable reinsurance programs backed by A-rated carriers and full-service administration that manages all filings, renewals, and regulatory requirements. If you're considering a reinsurance program or need to verify your current structure meets updated NAIC standards, contact DealerRE at (804) 824-9533 for a confidential consultation.