Why State VSC Compliance Is Complex (and Costly to Get Wrong)

Vehicle service contract providers face a reality that surprises many dealers: there's no single federal compliance playbook. Instead, VSC obligors, administrators, and sellers navigate a patchwork of state-level statutes, each with distinct licensing requirements, financial responsibility thresholds, and contract form mandates. Get it wrong, and the consequences escalate quickly—Texas publishes a formal penalty schedule starting at $1,000 for first violations and climbing to $4,000 per day for repeat offenses, while Florida's Office of Insurance Regulation can suspend or revoke licenses outright under s. 634.081.

Non-compliance isn't just costly; it can shut down operations. Recent enforcement actions include Michigan's Attorney General suing a VSC provider for deceptive advertising, and dealers in multiple states receiving cease-and-desist orders for selling without proper licensure.

If your dealership presents, administers, or backs VSCs in any capacity, understanding where your exposure lies is the first step. This guide is for:

- Franchise dealers presenting VSCs in the finance office

- Independent dealers and BHPH operators acting as obligor on their own programs

- Dealer principals entering or expanding VSC offerings across multiple states

TLDR

- No federal VSC standard exists—22+ states follow the NAIC Model Act, each with customized requirements

- Dealers can act as provider, administrator, seller, or obligor—each role carries distinct obligations

- Licensing, financial responsibility, and contract form approvals are required in most states before selling

- Florida, Texas, and Illinois have detailed frameworks; California, Alaska, and Maryland are tightening rules

- DealerRE manages filings, renewals, tax returns, and legal forms for dealer-owned reinsurance programs

Understanding the Key Roles: Provider, Administrator, Seller, and Obligor

State regulators don't view everyone in a VSC program the same way. Each role carries distinct legal and financial obligations:

Provider: The entity ultimately responsible for the contract—holds the license, ensures financial backing, and bears final accountability to regulators and consumers.

Administrator: Manages day-to-day operations including claims processing, customer communications, cancellations, and contract enforcement. In many dealer-owned programs, the dealer's reinsurance company operates through a licensed third-party administrator.

Seller: The dealership presenting the VSC to the consumer. Even when the dealer isn't the obligor, sellers must comply with disclosure rules, anti-sliding provisions, and advertising restrictions.

Obligor: The entity financially responsible for paying claims. In third-party programs, this is typically an insurer or warranty company. In admin-obligor structures, the dealer's reinsurance company becomes the obligor, backed by an A-rated insurer through contractual liability insurance (CLIP).

Why this matters:

Dealers who misidentify their role—or operate without the proper license for their actual function—trigger one of the most common audit findings. A dealer acting as obligor without an obligor license isn't just non-compliant; they're selling unenforceable contracts and exposing themselves to consumer lawsuits and regulatory penalties.

That's why role assignment in dealer-owned programs isn't just structural—it's the compliance foundation the entire program rests on. In programs DealerRE structures, the dealer's reinsurance entity becomes the obligor backed by A-rated insurers, with each role defined to meet state licensing requirements. That deliberate structure is what allows dealers to control underwriting profits and claims decisions without stepping outside their licensed authority.

The State-by-State Regulatory Framework: Why There's No Single Standard

The U.S. has no uniform federal VSC law. Instead, each state has enacted its own framework, creating a compliance landscape that changes at every state line.

NAIC Model Act Adoption:

The NAIC Service Contracts Model Act (#685) was adopted in 1995 as a baseline framework. According to the NAIC's own state-page chart, 22 jurisdictions have adopted the current version in substantially similar form. A 2022 NAIC-published academic paper notes "some suggest that as few as seven states fully adopted Model #685" — even "Model Act states" customize key provisions.

In practice, the adoption picture looks like this:

- ~38 states have some form of service contract statute

- 12–18 states rely solely on general consumer protection law

- States with "Model Act" adoption still modify key provisions to fit local priorities

That last point matters most. A state that claims Model Act adoption may still require different disclosures, different financial reserves, or different cancellation timelines than any other state on your list.

Two Regulatory Approaches:

The Standard Approach — Standalone Service Contract Statutes: Most states regulate VSCs outside their insurance codes entirely. These frameworks require provider registration, financial responsibility standards, contract disclosures, and cancellation rights — without treating VSCs as insurance products.

Florida's Exception — Insurance Code Regulation: Florida stands apart. Chapter 634, Title XXXVII treats motor vehicle service agreement companies as quasi-insurers, requiring licensure from the Office of Insurance Regulation and imposing solvency thresholds comparable to insurance carriers.

Florida's Multi-Product Categories:

Florida's insurance-code approach also creates a structural complexity that directly affects multi-state providers: separate statutes govern each product line within the same state.

- Motor vehicle service agreements (Chapter 634, Part I)

- Home warranties (Part II)

- Service warranties for consumer goods (Part III)

A multi-state VSC provider may need different licenses for different product lines in the same state.

States Requiring Pre-Approval of Contract Forms:

- Maryland: Obligors must file contracts at least 45 days before sale via SERFF ($125 per contract)

- Alaska: AS 21.59.125(a) prohibits delivery or issuance of motor vehicle service contracts unless the provider first files the contract and receives director approval

Recent Legislative Changes:

State laws change frequently. Examples include:

- Florida HB 989 (2024): Effective May 2, 2024, amended s. 634.041 to allow VSC obligors to use multiple contractual liability insurance policies (CLIPs) rather than requiring a single insurer, giving dealer-owned programs more flexibility

- California SB 766 (CARS Act): Chaptered October 6, 2025, prohibits dealers from charging for VSCs void due to preexisting conditions and requires 10-day payment to VSC providers

- Alaska SB 132: Created pre-approval requirements for motor vehicle service contract forms

Any of these changes can retroactively affect a compliant program. A form that passed approval in 2022 may violate a 2024 amendment — which is why ongoing monitoring, not just launch-time review, is the only defensible compliance posture.

Core Compliance Requirements Every VSC Provider Must Meet

Licensing and Registration

Most states require the VSC provider or obligor to obtain a license or registration before selling contracts. The application process typically involves:

- Financial statements demonstrating minimum net assets

- Appointment of a registered agent for service of process

- Filing fees (ranging from $25 in Maryland to $1,000+ in Illinois)

- Designated contact information

- Proof of financial responsibility (CLIP or reserve fund)

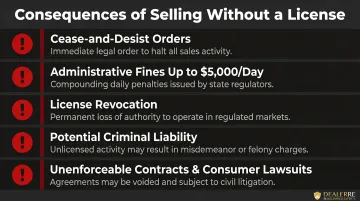

Consequences of selling without a license:

- Cease-and-desist orders halting all sales

- Administrative fines (Texas authorizes up to $5,000 per violation per day)

- License revocation for existing providers

- Potential criminal liability in some states

- Unenforceable contracts, exposing dealers to consumer lawsuits

Financial Responsibility Requirements

States accept two primary methods to demonstrate financial solvency:

1. Contractual Liability Insurance Policy (CLIP):

- Provider obtains a policy from an A-rated authorized insurer covering 100% of liabilities

- Contract must disclose insurer name, address, and direct filing rights

- Consumers may file claims directly with the insurer if the provider fails to pay within 60 days

2. Reserve Fund + Security Deposit:

- Provider maintains a funded reserve account (percentage of gross consideration less claims paid)

- Plus a security deposit (surety bond, securities, cash, or letter of credit)

- Percentage requirements vary by state

| State | Reserve Requirement | Security Deposit | Net Worth Alternative |

|---|---|---|---|

| Florida | 25-50% of unearned premium (waived if 100% CLIP) | $200,000 ($100K if <$750K premium) | $500,000 net assets required |

| Texas | 25% of gross consideration less claims | $25,000 minimum | $100,000,000 |

| Illinois | 40% of gross consideration less claims | 5% of gross consideration, min $25,000 | $15,000,000 |

Dealer-owned admin-obligor programs can satisfy these financial responsibility requirements through CLIP coverage backed by A-rated insurers, while keeping dealers in control of underwriting profits and claims adjudication. DealerRE manages the trust account administration, regulatory filings, and insurer partnerships required to maintain solvency standing in each state where a dealer operates.

Contract Form Requirements

States mandate specific disclosures and formatting in the VSC document itself:

Florida s. 634.121 requires:

- Boldfaced, conspicuous type for exclusions, limitations, and assignment rights

- Assignment provision: must be assignable within 15 days after vehicle sale/transfer; assignment fee capped at $40

- Pre-sale notice: "Purchase of the service agreement is not required to purchase or obtain financing"

- Pricing disclosure: "The rate charged for the service agreement is not subject to regulation by the office"

- Obligor's name, address, and Florida license number

Remanufactured parts and rental car disclosures:

- If the VSC permits used or remanufactured parts, this must be disclosed in boldfaced type

- Rental car benefit terms must be clearly stated

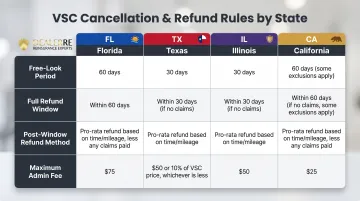

Cancellation and Refund Rules

States prescribe specific refund calculations for both consumer-initiated and provider-initiated cancellations:

| State | Free-Look Period | Full Refund Window | Post-Window Refund | Max Admin Fee |

|---|---|---|---|---|

| Florida | 60 days | 100% minus claims paid | 90% of unearned pro-rata minus claims | 5% of gross premium |

| Texas | 20 days (mail) / 10 days (in-person) | 100% if no claim filed | Pro-rata minus admin fee | $50 |

| Illinois | 20 days (mail) / 10 days (in-person) | 100% if no claim filed | Pro-rata minus admin fee | Lesser of 10% or $50 |

| California | 60 days (new) / 30 days (used) | 100% if no claim filed | Pro-rata | Lesser of 10% or $25 |

Important state-specific rules:

- Texas imposes a 10% monthly penalty on refunds not paid within 45 days

- Illinois allows consumers to file claims directly against the reimbursement insurer if the provider fails to pay within 60 days

- Florida permits provider-initiated cancellations after 60 days only for fraud, material misrepresentation, lack of maintenance, odometer tampering, or nonpayment—requiring certified mail notice

Claims Handling Standards

Most states prohibit unfair claim settlement practices, including:

- Failing to acknowledge claims promptly

- Denying claims without reasonable investigation

- Failing to provide written explanation for claim denials

- Misrepresenting contract provisions to settle claims for less than owed

- Altering documents without consumer consent

Florida s. 634.282(8) and Illinois 215 ILCS 152/35 both mirror these prohibitions, applying them to VSC administrators and obligors, not just insurers.

DealerRE's full-service administration includes claims adjudication that meets state standards by ensuring timely acknowledgment, reasonable investigation, and documented decision-making processes.

Advertising and Disclosure Rules

Key advertising prohibitions appearing in most state VSC statutes:

Florida s. 634.095 prohibits:

- Falsely implying affiliation with a motor vehicle manufacturer

- Claiming a manufacturer's warranty is expiring when it is not

- Advertising "free" warranties as inducements

- Representing that a warranty is required by law ("sliding")

Most states also require specific affirmative disclosures in any advertising:

- Name, address, and license number of the obligor in at least 12-point boldfaced type

- Clear identification that the product is a service contract, not insurance (in most states)

Beyond what's prohibited and required, provider naming rules add another layer. Under the NAIC Model Act, providers cannot use names including "insurance," "casualty," "surety," or "mutual," and cannot use names deceptively similar to insurance corporations.

State-Specific Compliance Highlights Dealers Should Know

Four states illustrate the range of regulatory approaches dealers encounter — from detailed insurance-code frameworks to model-act registrations to emerging consumer protection mandates. Here's what to know about each.

Florida (Chapter 634)

Florida maintains one of the most detailed VSC frameworks in the country, regulating motor vehicle service agreement companies under its insurance code.

Key requirements:

- Licensure from the Office of Insurance Regulation required before transacting business (s. 634.031)

- Minimum $500,000 net assets (s. 634.041(6))

- Required deposit: $200,000 in securities ($100,000 if gross written premium under $750,000)

- Unearned premium reserves: 25-50% of gross unearned premium unless 100% CLIP coverage

- Pre-sale disclosure of terms upon consumer request

- Specific contract form requirements (boldfaced exclusions, rental provisions, assignment language)

- Strict cancellation/refund timelines

2024 HB 989 update: Effective May 2, 2024, Florida now permits VSC obligors to use multiple CLIPs rather than requiring a single insurer for financial backing, giving dealer-owned programs more flexibility in structuring reinsurance arrangements.

Texas (Occupations Code Ch. 1304)

Texas regulates service contract providers under the Occupations Code Chapter 1304 through the Texas Department of Licensing and Regulation (TDLR), not the Office of Consumer Credit Commissioner.

Key requirements:

- Registration required for both providers and administrators (Sec. 1304.101, 1304.1025)

- Three financial security options: (1) reimbursement insurance covering 100% of liabilities; (2) funded reserve at 25% of gross consideration less claims + $25,000 security deposit; (3) net worth of at least $100 million

- Contracts must include plain-language disclosures, provider/administrator contact info, TDLR registration number, deductible amounts, claims procedure with toll-free number, and a mandatory statement directing unresolved complaints to TDLR

- Penalty schedule: 1st violation = reprimand to $1,000; 2nd = $500-$2,000; 3rd = $1,000-$4,000 per day

Illinois and the Model Act States

Illinois follows the NAIC Service Contract Model Act framework under 215 ILCS 152.

Key requirements:

- Registration with Director of the Department of Insurance

- Financial security: (1) reimbursement insurance from authorized insurer; (2) reserve at 40% of gross consideration less claims + security deposit at 5% of gross consideration (min $25,000); (3) net worth of $15 million

- $1,000 initial registration fee, $500 annual renewal

- Records must be kept for at least 3 years after coverage period expires

- Providers cannot use names including "insurance," "casualty," "surety," or "mutual"

The Model Act sets a baseline, but each adopting state customizes key provisions. Treat it as a starting point, not a compliance checklist.

Emerging Trends — States to Watch

California CARS Act (SB 766): Chaptered October 6, 2025, with key VSC-related provisions:

- Dealers cannot charge for VSCs void due to preexisting conditions (e.g., prior crash/flood damage)

- Dealers must pay VSC providers within 10 days of consumer signing

- Add-on optionality disclosure required in consumer's negotiation language

- 3-day cancellation right for used vehicles priced at $50,000 or less

Alaska pre-approval: AS 21.59.125 requires pre-approval of motor vehicle service contract forms by the Division of Insurance director before delivery or issuance

Maryland filing requirements: Obligors must file contracts at least 45 days before sale via SERFF ($125 per contract)

Florida SB 120 (proposed, died 3/13/2026): Would have required video recording of contracting process with elderly persons (60+) or disabled adults, memorializing understanding and absence of duress

Dealers operating across multiple states — or structuring dealer-owned reinsurance programs — need to track these developments actively. A requirement that passes in California or Alaska today can inform model legislation that appears in your home state next session.

How Dealers Can Build a Compliant VSC Program from the Start

Build Compliance into Program Design

Step-by-step approach:

- Identify your operating states: List every state where you plan to sell VSCs—including states where you occasionally deliver vehicles

- Determine your program structure: Are you a seller only, or will you act as obligor through a dealer-owned reinsurance company?

- Obtain required licenses before selling: Apply for all necessary registrations and licenses in each state before presenting a single contract

- Implement change-tracking: Establish a process for monitoring state legislative updates and regulatory changes

Compliance should be built into program design from day one, not retrofitted after a regulator inquiry.

Ongoing Operational Compliance

Running a VSC program requires continuous management:

- Timely contract form filings and amendments

- Annual license renewals in each state

- Accurate refund calculations on all cancellations

- Claims adjudication that meets state standards

- Financial reporting and reserve fund management

- Advertising materials that comply with disclosure rules

For dealers running admin-obligor programs, a full-service administrator like DealerRE handles the operational side of compliance: licensing coordination across states, state-mandated contract disclosures, claims adjudication, and financial reporting. That frees the dealer's internal team to focus on sales performance rather than regulatory paperwork.

Periodic Compliance Audits

Ongoing compliance management reduces day-to-day risk, but periodic audits go further—surfacing exposure that routine monitoring can miss. Schedule regular compliance reviews, either internal or through an experienced third-party resource, before a state regulator finds the gap first.

Pre-audit reviews are particularly important when:

- Acquiring an existing VSC program

- Expanding into a new state

- A state updates its VSC statutes

- Changing program structure (e.g., moving from seller-only to admin-obligor)

Frequently Asked Questions

What does VSC coverage mean?

A Vehicle Service Contract (VSC) is a contract between a vehicle owner and a provider that covers the cost of certain mechanical repairs or component failures, typically after the manufacturer's warranty expires or alongside it. Though often called an "extended warranty," it is not technically a warranty under federal law.

Are vehicle service contracts legally enforceable?

Yes, VSCs are legally enforceable contracts. Most states regulate them under specific service contract statutes or insurance codes that establish both provider obligations and consumer rights.

Who is the administrator of a vehicle service contract?

The administrator is the entity responsible for managing day-to-day operations of a VSC program—including processing claims, managing customer communications, and ensuring contract terms are honored. This may be a third-party company or, in a dealer-owned program, the dealer's reinsurance company operating through a licensed administrator.

What is a service contract provider in Texas?

In Texas, a service contract provider is an entity registered with the Texas Department of Licensing and Regulation (TDLR) to issue VSCs, and must meet specific financial responsibility and registration requirements under the Texas Occupations Code before selling contracts to consumers.

Is a vehicle service contract required?

VSCs are optional products; consumers are not legally required to purchase one. That said, dealers and providers offering them must comply with all applicable state licensing, contract form, and disclosure requirements regardless of purchase volume or consumer demand.

Is VSC the same as gap insurance?

No, these are distinct products. A VSC covers mechanical repair costs when components fail, while GAP insurance (or a GAP waiver) covers the difference between a vehicle's actual cash value and the remaining loan balance if the vehicle is totaled or stolen. Each product is regulated differently at the state level.