Introduction

Most auto dealers who decide to stop handing underwriting profits to third-party F&I providers and open their own reinsurance company hit the same wall early: state licensing requirements are nothing like what they've dealt with before. Reinsurance entities don't fall under dealer licensing rules — they fall under state insurance law, and that's an entirely different regulatory framework.

Dealers are used to working with Departments of Motor Vehicles or transportation authorities. The Department of Insurance operates on a different set of rules — with capital thresholds, compliance obligations, and ongoing regulatory oversight built specifically for entities that assume insurance risk.

This guide breaks down state-level licensing requirements for dealer-owned reinsurance companies. You'll learn who regulates these entities, what the application process involves, how your program structure affects requirements, and how DealerRE helps dealers navigate the process without getting buried in paperwork.

Key Takeaways

- State Departments of Insurance regulate dealer-owned reinsurance companies—not DMV or motor vehicle authorities

- Licensing requirements vary by state but typically include entity formation, capital minimums ($100,000–$250,000+), and formal DOI applications

- Admin obligor structure—backed by an A-rated insurer—determines which licensing pathways apply

- Ongoing compliance involves annual financial filings under Statutory Accounting Principles (SAP), premium tax returns, and license renewals

- DealerRE handles all legal forms, filings, tax returns, and license renewals for dealer clients

What Is a Dealer Reinsurance Company and Why Does Licensing Matter?

A dealer-owned reinsurance company is an insurance entity established by an automobile dealer to assume the risk—and retain the profit—from F&I products like vehicle service contracts, GAP coverage, and credit life insurance. Rather than paying underwriting profits to a third-party provider, the dealer captures these profits through their own reinsurance entity.

Vermont's Department of Financial Regulation formally classifies these entities as "Agency Captives"—reinsurance companies controlled by an insurance agency or brokerage that receive premiums and pay claims via a reinsurance agreement with a traditional insurer.

Because these entities technically assume insurance risk, state Departments of Insurance treat them as insurance-adjacent companies, triggering formal licensing and compliance obligations that differ entirely from standard dealer licensing.

Why proper licensing matters:

- Gives you the legal right to retain underwriting profits, invest premiums, and build long-term wealth through your own entity

- Operating without proper licensing exposes dealers to fines, cease-and-desist orders, contract invalidation, and potential jeopardy to your dealer license

- Nearly all U.S. states criminalize the unauthorized transaction of insurance, with penalties ranging from misdemeanors to felonies—Arizona classifies it as a Class 5 felony

These penalties catch many dealers off guard—because of a common misconception about who handles licensing. Many dealers assume their third-party administrator or program provider covers it entirely. While your administrator manages many compliance tasks, your reinsurance entity has independent state-level obligations that must be satisfied.

Who Regulates Dealer Reinsurance Companies?

State Departments of Insurance Hold Primary Authority

State Departments of Insurance hold primary jurisdiction over reinsurance companies operating within their borders. Unlike auto dealer licensing—which falls under departments of transportation or motor vehicle authorities—reinsurance entities answer to insurance regulators. Each state DOI maintains licensing authority, conducts financial examinations, and enforces solvency requirements for entities domiciled within its jurisdiction.

The NAIC's Role and Model Laws

The National Association of Insurance Commissioners (NAIC) sets model laws and standards that most states adopt, creating a baseline framework. However, implementation varies meaningfully from state to state. Key NAIC model laws relevant to dealer reinsurance include:

Credit for Reinsurance Model Law (#785): Governs when a ceding insurer may take credit for reinsurance on its financial statements and defines authorized versus unauthorized reinsurer status.

Unauthorized Insurers Process Act (#850): Provides states with jurisdiction over unlicensed entities conducting insurance business within their borders.

Captive Insurance Laws (Chart CA-80): State-by-state comparison of captive insurance laws, capital requirements, and permitted structures.

Federal Oversight Is Limited

Reinsurance regulation in the U.S. is primarily state-based, not federal. The Dodd-Frank Act created the Federal Insurance Office (FIO) within the Treasury Department, but the FIO has no supervisory role over insurance providers. That authority stays with state regulators.

The Nonadmitted and Reinsurance Reform Act (NRRA), passed as part of Dodd-Frank, did simplify multi-state reinsurance regulation. If the ceding insurer's state of domicile is NAIC-accredited and recognizes credit for reinsurance, no other state may deny that credit. For dealer reinsurance companies operating through a fronting carrier structure, this significantly reduces multi-state regulatory complexity.

Onshore vs. Offshore Domiciles

Dealer-owned reinsurance companies have historically used both onshore and offshore jurisdictions. Common offshore options include:

- Cayman Islands — lower capital requirements and fewer reserve mandates than most U.S. states

- British Virgin Islands — flexible regulatory structure with established reinsurance infrastructure

- Turks and Caicos Islands — another popular choice for dealer-owned captive structures

The trade-off is collateral. Offshore reinsurers not authorized in U.S. states face a 100% collateral requirement under the NAIC Credit for Reinsurance framework, which affects how the fronting carrier reflects the arrangement on its balance sheet. That cost has to be weighed against any regulatory savings.

If you operate franchises or used car lots in multiple states, each state's rules around the reinsurer's domicile also come into play — specifically whether the entity must be separately licensed or recognized in each operating state.

Common State Licensing Requirements for Dealer Reinsurance Companies

Entity Formation as a Prerequisite

Before applying for any insurance or reinsurance license, your company must be formally incorporated or organized—typically as a corporation or LLC—in your chosen domicile state.

The domicile state (where the entity is chartered) and the operating states may differ. That choice affects several key factors:

- Tax treatment: Some domiciles offer favorable captive tax structures

- Regulatory oversight: Each state's insurance department sets its own filing and examination requirements

- Ongoing compliance costs: Annual fees, reporting obligations, and examination schedules vary significantly by state

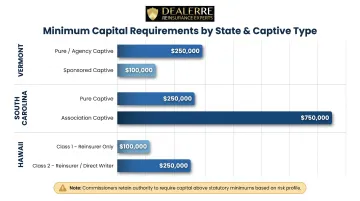

Capital and Surplus Minimums

Most states impose minimum capital and surplus requirements that a reinsurance company must meet to receive and maintain its license. These minimums vary significantly by state and by the type of coverage the entity will reinsure.

| State | Captive Type | Minimum Capital |

|---|---|---|

| Vermont | Pure/Agency Captive | $250,000 |

| Vermont | Sponsored Captive | $100,000 |

| South Carolina | Pure Captive | $250,000 |

| South Carolina | Association Captive | $750,000 |

| Hawaii | Class 1 (Reinsurer Only) | $100,000 |

| Hawaii | Class 2 (Reinsurer/Direct Writer) | $250,000 |

In all jurisdictions, the insurance commissioner can require capital above statutory minimums based on the type, volume, and nature of business transacted. Budget conservatively above these floors — regulators routinely request additional reserves when program volume grows or when the lines of coverage written are considered higher risk.