This guide explains what the 831(b) election is, why dealer reinsurance programs use it, what the 2025 IRS final regulations changed, and how most properly structured dealer reinsurance companies may no longer need to file Form 8886 at all. We'll also cover the Consumer Coverage Exception—a critical safe harbor that protects most dealer F&I reinsurance structures.

TLDR:

- The 831(b) election lets qualifying small insurance companies exclude underwriting income from federal tax—only investment income is taxed

- The 2025 premium limit is $2,850,000; 2026 increases to $2,900,000

- T.D. 10029 (published January 14, 2025) replaced Notice 2016-66 and created new "listed transaction" and "transaction of interest" rules

- Most admin obligor dealer reinsurance programs won't meet the regulatory definition of "Insured" or "Captive"—meaning no Form 8886 filing required

- The Consumer Coverage Exception provides an additional safe harbor for dealer F&I programs covering unrelated customers

What Is the Section 831(b) Election?

Section 831(b) of the Internal Revenue Code allows qualifying small nonlife insurance companies to elect alternative tax treatment. Instead of paying corporate income tax on all income, the company pays tax only on its investment income. Underwriting profits (premiums collected minus losses paid) are excluded from federal income tax.

Under normal 831(a) taxation, a captive insurance company pays the 21% corporate tax rate on all income. Under 831(b), underwriting income accumulates tax-free and only investment returns are taxed at the corporate rate.

When the company distributes accumulated earnings as dividends to individual shareholders, those distributions qualify for preferential qualified dividend rates of 0%, 15%, or 20% — well below ordinary income rates.

History: From the 1986 Tax Reform Act to the PATH Act

Section 831(b) was introduced in the Tax Reform Act of 1986 to support small insurance company formation during the liability insurance crisis of the 1980s. The statute was amended by the Protecting Americans from Tax Hikes (PATH) Act of 2015, which:

- Raised the premium threshold from the original amount to $2,200,000 base amount

- Added diversification requirements (no single policyholder can represent more than 20% of premiums)

- Mandated annual inflation adjustments in $50,000 increments

The premium limit is now adjusted annually. For 2025, the limit is $2,850,000. For 2026, it increases to $2,900,000.

Key Requirements to Qualify for 831(b)

Meeting those PATH Act thresholds is necessary, but not sufficient. Your reinsurance company must also satisfy all of the following to make the election:

- Be a nonlife (property and casualty) insurance company

- Have net written premiums below the annual inflation-adjusted limit

- Meet the 20% diversification test (no single policyholder exceeds 20% of total premiums)

- File the election on Form 1120-PC by the tax return due date for the first election year

831(a) vs. 831(b): Why the Election Matters

| Tax Treatment | Underwriting Income | Investment Income | Typical Effective Rate |

|---|---|---|---|

| 831(a) | Taxed at 21% corporate rate | Taxed at 21% corporate rate | 21% on all income |

| 831(b) | Excluded from federal tax | Taxed at 21% corporate rate | 0% on underwriting + 21% on investment |

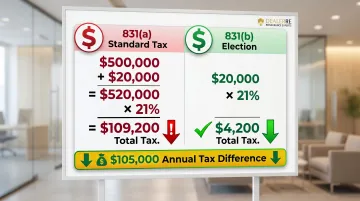

For a dealer reinsurance company generating $500,000 in underwriting profit and $20,000 in investment income, the tax difference is substantial:

- Under 831(a): ($500,000 + $20,000) × 21% = $109,200 tax

- Under 831(b): $20,000 × 21% = $4,200 tax

That's a $105,000 difference in federal tax liability on the same revenue — before accounting for the additional savings when earnings are eventually distributed as qualified dividends.

What "Micro-Captive" Really Means

A company making the 831(b) election is commonly called a micro-captive because of the premium cap. The term has become loaded due to IRS enforcement actions against abusive structures, but not all micro-captives are problematic — many are legitimate risk management tools used by businesses of all kinds. The label refers to size and tax election status, nothing more.

How Dealer Reinsurance Companies Use the Section 831(b) Election

Dealers who establish their own reinsurance companies—typically structured as admin obligor programs—receive premiums from F&I products sold to customers: vehicle service contracts (VSCs), guaranteed asset protection (GAP), collateral protection insurance, and ancillary products like tire-and-wheel or windshield protection. The reinsurance company collects a portion of those premiums and funds claims as they arise.

The 831(b) election is advantageous because when claims run lower than premiums collected, underwriting profits accumulate inside the reinsurance company tax-deferred. Instead of being taxed immediately at corporate rates, those profits can be invested to generate additional returns. Tax is paid only when distributed as dividends, and at preferential rates.

The Admin Obligor Structure: Why Dealers Aren't "Insureds"

In a typical admin obligor structure, the dealer is not a party to the insurance contract with the customer. The fronting carrier or intermediary issues the policy to the retail buyer. The dealer's reinsurance company reinsures a portion of that contract under a separate reinsurance agreement with the fronting carrier.

This structural fact is critical to how the 2025 IRS regulations apply. The regulations define an "Insured" as a party that:

- Conducts a trade or business

- Enters into a contract with the captive (or an intermediary reinsured by the captive)

- Treats amounts paid as insurance premiums for federal tax purposes

In an admin obligor program, the dealer doesn't enter into the contract with the customer and doesn't deduct insurance premiums. The customer (car buyer) is the policyholder, and the fronting carrier is the contractual counterparty to the reinsurance company. Because the dealer doesn't meet the three-part "Insured" definition, most dealer reinsurance structures fall outside the scope of the new regulations entirely.

Why Dealer Programs Differ from Enterprise-Risk Captives

The IRS's concern with micro-captive abuse has centered on enterprise-risk captives—structures where a business owner's captive insures that same owner's business-level risks (property, liability, directors and officers coverage) at inflated premiums, often with loan-back arrangements. Dealer reinsurance programs represent a structurally different model. Where enterprise-risk captives insure the owner's own business risks, dealer programs draw risk from thousands of unrelated retail customers purchasing warranty-like products.

That separation is what makes the difference. Two key contrasts:

- Risk source: Enterprise captives = owner's own business risks; dealer programs = unrelated retail customers

- Premium driver: Enterprise captives = internal cost allocation; dealer programs = real-world mechanical failures, total losses, insurance gaps

- Tax planning nexus: Enterprise captives often tied to premium inflation; dealer programs priced by third-party actuarial data

Consumer-facing reinsurance involves genuine third-party risk with no tax planning motive. The premiums and claims are driven by actual breakdowns and losses—not ownership structure.

DealerRE Note: DealerRE manages all legal forms, filings, tax returns, and renewals for the dealer reinsurance companies it supports, including coordinating the 831(b) election filing and ensuring ongoing compliance with premium limits and diversification requirements.

The 2025 IRS Final Regulations: What Changed for Dealer Reinsurance

On January 14, 2025, the IRS published final regulations (T.D. 10029) on micro-captive insurance arrangements. These regulations replaced the prior Notice 2016-66 and created two new classifications: "listed transactions" and "transactions of interest." Both trigger mandatory Form 8886 disclosure requirements and increased IRS scrutiny.

The "Insured" Definition: Why Most Dealers Don't Qualify

The regulations apply only when a defined "Insured" exists. Per 26 CFR 1.6011-10(b)(4), an "Insured" is any person that:

- Conducts a trade or business

- Enters into a contract with a captive or with an intermediary reinsured by a captive

- Treats amounts paid under the contract as insurance premiums for federal tax purposes

In a typical admin obligor dealer reinsurance program:

- The dealer conducts a trade or business (✓)

- The dealer does not enter into a contract with the captive or intermediary—the customer does (✗)

- The dealer does not treat amounts paid as insurance premiums on its tax return (✗)

Because the dealer fails criteria 2 and 3, there is no "Insured" under the regulatory definition. Without an "Insured," the company is not a "Captive" under these rules, and there is no Form 8886 filing requirement.

The "Captive" Definition and Ownership Threshold

Even if an "Insured" existed, the regulations define a "Captive" as an entity that:

- Elects under Section 831(b) to be taxed only on investment income

- Issues or reinsures a contract to an Insured

- Has at least 20% common ownership with the Insured or related parties

Without an "Insured," the 20% ownership test never applies. The dealer's reinsurance company may be 100% dealer-owned, but if the dealer isn't an "Insured," the ownership overlap is irrelevant for purposes of these regulations.

Listed Transaction vs. Transaction of Interest Thresholds

For programs that do meet the "Captive" definition, the regulations establish two classification levels based on loss ratios and financing arrangements:

| Classification | Loss Ratio Threshold | Financing Factor | Both Required? |

|---|---|---|---|

| Listed Transaction | Less than 30% over 10 years | Loan-back or capital transfer to related party | Yes—both factors required |

| Transaction of Interest | Less than 60% over 10 years | Either factor alone | No—one factor sufficient |

Listed transactions carry the most serious consequences: penalties up to $200,000 per year for entities and extended statute of limitations.

Transactions of interest require disclosure but carry lower penalties and less severe scrutiny.

These thresholds matter primarily for enterprise-risk captives, not consumer-facing dealer reinsurance programs. A well-run dealer program with genuine claims activity should maintain loss ratios well above 30%—and likely above 60%—placing it outside both classifications even if it somehow met the "Captive" definition.

Notice 2016-66: What It Required and Why It's Obsolete

Understanding where the new rules came from helps clarify what still applies to your program. Notice 2016-66, issued in 2016, classified micro-captive transactions as transactions of interest and required Form 8886 filings using a 70% loss ratio threshold over five years. Courts later invalidated it for failure to comply with the Administrative Procedure Act, but many taxpayers continued filing protectively.

T.D. 10029 formally obsoletes Notice 2016-66. Here's what that means for prior filings:

- Prior Form 8886 filings under the notice satisfy transaction-of-interest disclosure for pre-2025 years

- Those same filings do not satisfy listed transaction requirements under the new rules

- Dealers who previously filed protectively must reassess whether any filing is required at all

Continuing to file based on obsolete guidance may unnecessarily flag your reinsurance company for scrutiny when no disclosure is actually required.

The Consumer Coverage Exception: An Additional Safe Harbor

Even for reinsurance companies that do meet the regulatory definition of a "Captive," the 2025 final regulations provide a safe harbor that removes the Form 8886 filing requirement: the Consumer Coverage Exception.

The Four Requirements

Per 26 CFR 1.6011-10(d)(2), a transaction is excepted from both listed transaction and transaction of interest classification if the captive meets all four of these criteria:

- Related to a Seller: The captive is related to a seller, an owner of seller, or related persons

- Consumer-Facing Contracts: The captive issues or reinsures contracts purchased by unrelated customers in connection with products or services sold by the seller

- 100% Consumer Coverage: 100% of the captive's business is issuing or reinsuring contracts connected to products or services sold by the seller or related persons

- 95% Unrelated Customer Test: At least 95% of the captive's business is issuing or reinsuring contracts purchased by unrelated customers

The regulations explicitly define "Seller" to include "dealer (including an automobile dealer)" who sells products or services to customers who purchase insurance contracts in connection with those products.

How Dealer F&I Programs Typically Qualify

A dealer reinsurance company covering VSCs, GAP, and ancillary F&I products sold to unrelated retail customers typically satisfies all four conditions:

- Related to seller: The captive is dealer-owned (✓)

- Consumer-facing: VSCs and GAP are purchased by customers in connection with vehicle sales (✓)

- 100% consumer coverage: The captive reinsures only F&I products, not enterprise risks (✓)

- 95% unrelated customers: Retail car buyers are unrelated to the dealer (✓)

The 5% tolerance creates a narrow buffer — up to 5% of the captive's business may involve related-party contracts without disqualifying the exception.

The Enterprise Risk Trap: Don't Mix Coverage Types

Qualifying is straightforward for most dealer reinsurance programs — but one structural mistake can invalidate the exception entirely.

The 100% consumer coverage requirement is strict. If a dealer's reinsurance company also insures the dealership's own business-level risks — property damage, general liability, directors and officers coverage, cyber insurance, employment practices liability — those enterprise-risk coverages cause the captive to fail the 100% test.

Mixing enterprise risk with consumer coverage is the primary compliance trap. Dealers who need both types of coverage should maintain separate entities. DealerRE programs are built around consumer F&I product coverage only — no enterprise-risk insurance is included — so dealer clients don't inadvertently forfeit the Consumer Coverage Exception.

Compliance Steps Every Dealer with a Reinsurance Company Should Take

Step 1: Confirm Your 831(b) Election Status

Verify that an active 831(b) election is in place and properly documented. Without a valid election, your company is taxed under 831(a)—all underwriting profits are taxable—and the 2025 final regulations do not apply. The election is made on Form 1120-PC and must be filed by the due date of the return for the first election year.

Rev. Proc. 2025-13 now provides a streamlined revocation procedure if you need to exit the election without obtaining a private letter ruling.

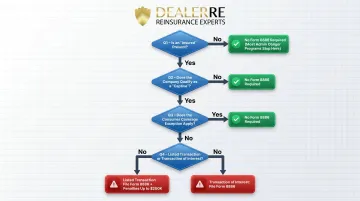

Step 2: Walk Through the Sequential Compliance Framework

Use this decision tree to determine whether Form 8886 applies to your program. Most dealer-owned reinsurance structures exit at Step 3, but working through each question confirms that position.

Question 1: Is an "Insured" present per the 2025 regulatory definition?

- Does the dealer conduct a trade or business? (Yes)

- Does the dealer enter into a contract with the captive or an intermediary reinsured by the captive? (In admin obligor structures: No)

- Does the dealer treat amounts paid as insurance premiums for tax purposes? (No)

If no "Insured" exists, STOP. No Form 8886 required.

Question 2 (if "Insured" exists): Does the company qualify as a "Captive"?

- Has the company elected 831(b)? (Yes)

- Does it issue or reinsure contracts to the Insured? (Yes)

- Is there at least 20% common ownership? (Likely yes)

If no "Captive" definition is met, STOP. No Form 8886 required.

Question 3 (if "Captive" exists): Does it meet the Consumer Coverage Exception?

- Related to a seller? (Yes—dealer-owned)

- Consumer-facing contracts? (Yes—VSCs, GAP sold to customers)

- 100% consumer coverage (no enterprise risk)? (Yes—if properly structured)

- 95%+ unrelated customers? (Yes—retail buyers)

If the Consumer Coverage Exception applies, STOP. No Form 8886 required.

Question 4 (if exception doesn't apply): Is it a listed transaction or transaction of interest?

- Does the captive have a financing factor (loan-backs, capital transfers)?

- What is the 10-year average loss ratio?

- If loss ratio < 30% and financing factor present = Listed Transaction

- If loss ratio < 60% or financing factor present = Transaction of Interest

If listed transaction or TOI applies: File Form 8886 with your tax return and send a copy to the IRS Office of Tax Shelter Analysis within 90 days of the designation.

Step 3: Monitor Premium Limits Annually

Separate from the Form 8886 analysis, the 831(b) election itself carries an annual premium cap. Exceeding it disqualifies the company from the election for that year.

| Year | Inflation-Adjusted Premium Limit |

|---|---|

| 2025 | $2,850,000 |

| 2026 | $2,900,000 |

Track net written premiums quarterly to stay within the limit.

DealerRE includes compliance oversight as part of its program administration — covering regulatory applicability reviews, filing assistance when required, and quarterly performance reporting against premium thresholds.

Frequently Asked Questions

What is the 831(b) premium limit?

The annual net written premium limit is inflation-adjusted each year. For 2025, the limit is $2,850,000; for 2026, it increases to $2,900,000. Exceeding this limit in any tax year disqualifies the company from the 831(b) election for that year, causing all underwriting income to be taxed at regular corporate rates.

What is a micro captive transaction?

A micro-captive is a captive insurance company that has elected to be taxed only on investment income under Section 831(b). The term "transaction" in an IRS context refers to arrangements the IRS has identified as potentially abusive—though many micro-captive arrangements are legitimate and compliant.

Does a dealer reinsurance company have to make a Section 831(b) election?

No, the election is optional. Without it, the company is taxed under 831(a) on all underwriting income at regular corporate rates, and the 2025 IRS micro-captive regulations do not apply. Making the election enables the underwriting profit exclusion from federal income tax.

What is the Consumer Coverage Exception and does my dealership qualify?

The Consumer Coverage Exception is a safe harbor in the 2025 IRS regulations that exempts certain consumer-facing reinsurance companies from Form 8886 filing. Most dealer F&I reinsurance programs covering VSCs and similar products qualify, though each program should be evaluated against the four-part test.

Do dealer reinsurance companies still have to file Form 8886 under the 2025 final regulations?

Many dealer reinsurance companies structured as admin obligor programs no longer meet the regulatory definition of "Insured" or "Captive" under the 2025 rules, so Form 8886 is no longer required. Continuing to file under the old Notice 2016-66 framework may be unnecessary and could flag your company for unwarranted scrutiny.

How is underwriting income taxed in an 831(b) company vs. an 831(a) company?

Under 831(b), underwriting profits (premiums minus losses) are excluded from federal income tax and only investment income is taxed at the 21% corporate rate. Under 831(a), all income including underwriting profits is taxed at regular corporate rates—making the 831(b) election more favorable for profitable dealer reinsurance programs.