Introduction

Most auto dealers enrolled in profit participation programs assume they're earning well on their F&I products. In reality, you may be capturing only a fraction of the profits your vehicle service contracts and GAP products generate — while third-party administrators keep the rest.

Both dealer reinsurance and profit participation programs let dealers share in F&I underwriting profits. They differ fundamentally, though, in ownership, control, tax treatment, and long-term financial upside.

Those differences matter. The profit gap between the two models compounds over time, affecting not just your annual income but your dealership's balance sheet value.

Key Takeaways

- Profit participation programs share underwriting profits with dealers, but a third-party administrator keeps the majority

- Dealer reinsurance lets you own your own reinsurance company and capture 100% of underwriting profits plus investment income

- The two programs differ most on profit capture, tax planning potential, and long-term wealth-building — not just upfront simplicity

- Dealers with consistent F&I volume and long-term growth goals typically benefit more from reinsurance than profit participation

- The right choice depends on deal volume, financial goals, risk tolerance, and operational readiness

Dealer Reinsurance vs. Profit Participation Programs: Quick Comparison

The comparison below covers the eight dimensions that most directly affect dealership profitability, control, and long-term wealth. Pay particular attention to the profit capture, tax, and exit rows — that's where the two structures diverge most sharply.

| Dimension | Profit Participation | Dealer Reinsurance |

|---|---|---|

| Profit capture | Partial (percentage of net profit) | 100% of underwriting profit minus admin fees |

| Investment income | None (retained by administrator) | Earned on premiums held in trust |

| Tax advantages | None (ordinary income) | 831(b) election available for qualifying companies |

| Company setup required | No | Yes (CFC, DOWC, or similar structure) |

| Control over claims | None | Full visibility and influence |

| Risk assumed | None | Dealer participates in underwriting risk |

| Exit flexibility | Exit penalties common | More portable, dealer owns the entity |

| Long-term wealth potential | Limited (periodic commission checks) | Significant (asset with balance sheet value) |

These reflect the most common program structures. Individual programs vary, so dealers should review specific terms with a qualified reinsurance advisor — such as DealerRE — before moving forward.

What is Dealer Reinsurance?

Dealer reinsurance is an arrangement in which a dealer establishes their own reinsurance company that assumes the insurance risk associated with F&I products — primarily vehicle service contracts, GAP, and ancillary products — from the primary insurer. When claims are lower than premiums collected, the dealer's company earns the underwriting profit.

The Admin Obligor Structure

DealerRE specializes in the admin obligor (AO) model, which pairs a dealer's reinsurance company with an A-rated primary insurer. The dealer participates in the financial upside while the insurer provides the regulatory and claims backstop. This structure removes many compliance burdens while preserving the dealer's profit capture. According to AM Best's rating system, an A rating signifies "Excellent" financial strength and ability to meet ongoing policy obligations.

Three Core Financial Benefits

Three financial advantages separate dealer reinsurance from profit participation:

- Full underwriting profit capture: The dealer's company keeps 100% of the underwriting result — not a capped percentage — with only administrative fees paid out.

- Investment income on reserves: Premiums are held in trust before claims are paid, generating investment returns that compound over time. Profit participation offers no equivalent.

- Section 831(b) tax treatment: Under IRS Section 831(b), smaller reinsurance companies may be taxed only on investment income — not underwriting profit — if annual net written premiums stay below $2,900,000 for 2026. This treatment is unavailable in profit participation structures.

Claims Control and Visibility

Because the dealer owns the reinsurance entity, they have visibility into and influence over claims handling. This allows them to manage costs, spot patterns, and improve the customer experience — something impossible with a third-party profit participation arrangement where the administrator controls claims entirely.

Who Reinsurance Fits Best

Reinsurance programs work for:

- Franchise dealers with consistent F&I product volume

- Independent dealers selling new and pre-owned vehicles

- BHPH operators who can use reinsurance to protect against mechanical breakdown losses funded by the customer base

Reinsurance can be structured for both new and pre-owned vehicle sales, with sufficient volume to justify company formation and management.

Use Cases of Dealer Reinsurance

A franchise or independent dealer with consistent F&I volume can redirect underwriting profit — currently paid out to a third-party administrator — directly into their own reinsurance company. That margin stays in the dealer's hands instead of a vendor's.

Earned reinsurance income can then be reinvested strategically: back into the dealership, real estate, education, or other assets. Unlike periodic profit share checks, reinsurance reserves accumulate and compound, building value that grows alongside the dealer's book of business.

What is a Profit Participation Program?

Profit participation programs are commission-based arrangements — also called profit shares, retro commissions, contingent commissions, or guaranteed retros — where the dealer receives periodic payments from the F&I administrator or insurer based on the underwriting profitability of the dealer's book of contracts. No separate company is formed, and no insurance risk is assumed by the dealer.

Common Types

Dealers encounter several variations:

- Standard profit share — Paid when the book is profitable

- Retrospective commission — Calculated on actual loss experience

- Contingent commission — Tied to volume or loss ratio thresholds

- Advanced profit share — Payments made earlier, subject to reconciliation

Despite different names, all of these programs are commission arrangements — not reinsurance — even if a provider issues a "cession statement." According to JMA Group, payouts typically begin after two full calendar years of writing contracts, and the dealer is not responsible for losses — but checks stop if the portfolio goes negative.

What Profit Participation Programs Don't Include

These programs lack several critical components:

- No investment income

- No tax planning advantages

- No control over claims

- No company ownership

- Profits capped by the administrator's payout formula

The dealer will only ever receive a fraction of what the program actually earns.

Operational Considerations

Profit participation programs typically have:

- Volume requirements for payout tiers

- Exit penalties or suspension of payments when the dealer leaves the program

- Limited portability — details dealers often only discover after they've committed

These terms can be easy to overlook during onboarding, but they directly affect how much the program is worth if the dealer's situation changes.

When a Profit Participation Program Makes Sense

Profit participation may make sense for:

- Dealers with lower F&I volume

- Those just beginning to build their product mix

- Dealers not yet ready for the administrative responsibility of owning a reinsurance entity

For dealers who meet these criteria, profit participation offers a low-barrier entry into underwriting economics. Once volume grows and the dealership is operationally ready, transitioning into a dealer-owned reinsurance structure captures significantly more of those same profits.

Dealer Reinsurance vs. Profit Participation: Which Program Fits Your Dealership?

Primary Decision Factors

Dealers should evaluate:

- Monthly F&I product volume and premium generation — Higher volume justifies reinsurance company formation

- Long-term business and personal financial goals — Wealth building vs. periodic income

- Appetite for ownership — Are you ready to own a reinsurance entity?

- Interest in tax planning — Can 831(b) election benefit your situation?

- Desire for claims control — Do you want to influence the customer experience?

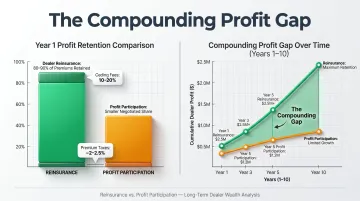

The Real Profit Gap

In a profit participation program, the dealer receives a percentage of underwriting profits — the administrator keeps the rest. In a reinsurance structure, the dealer's company captures the full underwriting result and pays only administration fees.

Industry data from Buckeye Reinsurance puts the numbers in context:

- Ceding fees: 10–20% depending on volume

- Premium taxes: approximately 2–2.5%

- Dealer retention under reinsurance: 80–90% of premiums after fees

- Dealer share under profit participation: a negotiated percentage — often significantly less — with the administrator keeping the balance

Over multiple years, this gap compounds. The reinsurance company earns investment income on reserves it holds directly. In a profit participation program, the administrator holds and invests those funds — not the dealer.

Situational Guidance

Choose dealer reinsurance if you:

- Have consistent F&I volume ($250,000+ in annual premium is a common threshold)

- Want to build long-term financial assets

- Are interested in tax planning and wealth management

- Want control over your claims process and customer experience

Choose profit participation if you:

- Are early-stage or running lower volume

- Prefer simplicity with no company management responsibilities

- Want to test F&I product profitability before committing to ownership

Common Misconceptions About Dealer Reinsurance

These four myths hold dealers back — here's what's actually true:

- "It requires going offshore" — Some structures do use offshore domiciles like Turks and Caicos, but all funds remain in U.S. trust accounts. Domestic options (DOWC) are available too.

- "It's only for large franchise dealers" — Independent and BHPH dealers qualify with sufficient F&I product volume. Franchise scale isn't a requirement.

- "It's too complicated to manage" — DealerRE handles administration, compliance, filings, and reporting. No in-house expertise needed.

- "It's too risky" — Admin obligor structures are backed by A-rated insurers. Dealers share in underwriting profits when claims are low and are protected from catastrophic loss exposure.

Long-Term Wealth Building

Unlike profit share checks — which are income and nothing more — a well-managed dealer reinsurance company accumulates capital that can be invested, loaned, or distributed, creating a genuine business asset.

"Properly managed reinsurance programs can evolve into meaningful balance sheet assets and cash-generating entities." — CBT News

That compounding advantage is what separates reinsurance ownership from simply receiving a periodic check.

Real-World Example: From Profit Share to Full Profit Capture

Consider a mid-sized independent dealer who had been enrolled in a profit participation program for several years. The dealer was satisfied — until a reinsurance analysis showed exactly how much underwriting profit their administrator was keeping each year.

What Triggered the Evaluation

The dealer's F&I director attended a state dealer association event where DealerRE presented on reinsurance. Curious about the profit gap, the dealer requested an analysis comparing their current profit share arrangement against a reinsurance structure.

The Transition Process

The dealer worked with DealerRE to:

- Establish a reinsurance company under the admin obligor model

- Train F&I staff on new product offerings and claims procedures

- Move product sales to reinsured contracts

DealerRE handled all legal forms, filings, tax returns, and renewals to maintain compliance with IRS Code 831(b) and state regulations.

What Changed Operationally

Once the reinsurance program was in place:

- Per-deal F&I profitability improved — The dealer retained the full underwriting margin instead of sharing it

- Investment income was earned — Premiums held in trust generated returns that belonged to the dealer's company

- Claims visibility increased — The dealer could track claim patterns and manage costs proactively

- Tax benefits were realized — The 831(b) election allowed underwriting profit to accumulate tax-deferred

The dealer's reinsurance company became a fifth business unit alongside Sales, Service, Parts, and F&I, generating capital that could be reinvested into dealership growth, real estate, or other strategic assets.

Situational Takeaway

This example best applies to dealers who:

- Have consistent monthly F&I volume

- Are already comfortable with their product mix and penetration rates

- Want to transition from periodic commission checks to building a capital asset

Contact DealerRE for a no-obligation analysis to see how your current F&I program's profitability compares under a reinsurance structure.

Conclusion

Dealer reinsurance and profit participation programs both allow dealers to participate in the financial performance of their F&I products, but they operate at fundamentally different levels — one is a commission arrangement, the other is ownership. The right choice comes down to volume, timeline, and how seriously the dealer wants to build a long-term financial asset.

For dealers with growing F&I volume and a long-term outlook, reinsurance consistently delivers more than profit participation alone:

- Captures a larger share of underwriting profits instead of passing them to a third party

- Builds a dealer-owned financial asset that grows with the program

- Opens investment upside on accumulated premiums

- Provides control over claims experience and product performance

With the right administrative partner handling the legal, compliance, and reporting details, the operational lift is more manageable than it appears.

Frequently Asked Questions

What's the difference between insurance and reinsurance?

Insurance is the primary risk coverage product sold to consumers. Reinsurance is the arrangement where a separate company (in this case, dealer-owned) assumes the risk from the primary insurer, allowing the dealer to capture underwriting profits instead of passing them to a third party.

How does profit participation work?

Profit participation is a commission arrangement where the dealer receives periodic payments from their F&I administrator based on product profitability. No separate company is formed, no risk is assumed, and the dealer receives only a share of profits — not the full underwriting income.

What are the 4 types of reinsurance?

Common dealer reinsurance structures include CFC (controlled foreign corporation offshore), Super CFC (higher-volume offshore structure), DOWC (dealer-owned warranty company domestic), and admin obligor/DORC (dealer obligor reinsurance company). The admin obligor model is the most dealer-friendly structure because it combines full profit ownership with A-rated insurer backing for catastrophic risk.

Can small or independent dealerships qualify for dealer reinsurance?

Yes. Reinsurance is not just for large franchise dealers — independent and even BHPH dealers can establish reinsurance programs, provided they have sufficient F&I product volume to support adequate risk distribution. DealerRE offers a no-obligation dealership analysis to determine whether your current volume and product mix can support a reinsurance program.

What are the tax advantages of a dealer-owned reinsurance company?

Smaller reinsurance companies may qualify for the 831(b) election, where only investment income is taxed — not underwriting profit — provided annual premiums stay below $2,900,000. This, combined with the ability to invest premium reserves and control distributions, creates tax planning advantages that profit participation simply can't match. A qualified tax advisor should be consulted for guidance specific to your situation.

Is dealer reinsurance risky for the dealership?

The dealer does assume underwriting risk, but admin obligor structures offset this with an A-rated primary insurer as the backstop — so the dealer participates in profits when claims are low while remaining protected from catastrophic loss. Proper pricing and sufficient deal volume keep risk well-distributed across the program.