Introduction

BHPH dealers carry their own paper, absorbing credit risk from customers with FICO scores averaging between 461 and 554. But credit risk is only half the equation. When a customer's vehicle breaks down or gets totaled without insurance, the dealer either covers repair costs out of pocket or absorbs a repossession loss.

That dual exposure—credit risk plus collateral risk—is what makes risk management structure a direct cash flow decision, not an administrative one.

How you structure protection against that exposure determines whether underwriting profit stays inside your dealership or whether claim volatility repeatedly drains operating capital. Dealer-owned reinsurance creates a structured, premium-funded reserve that builds dealer equity. SIR leaves you exposed to unpredictable repair costs with no profit capture mechanism.

This article compares reinsurance and SIR across five critical dimensions: structure, profit potential, risk exposure, regulatory backing, and which model fits different dealer profiles.

Key Takeaways

- Dealer-owned reinsurance collects F&I premiums and captures the underwriting profit third-party providers normally keep

- SIR requires dealers to pay each claim directly from operating cash before excess coverage applies — no premium income collected

- Reinsurance builds long-term profit, offers tax advantages, and gives dealers control over claims; SIR offers simplicity at the cost of cash exposure

- Admin-obligor reinsurance is backed by A-rated insurers, a financial protection layer SIR does not provide

- BHPH dealers with steady F&I volume consistently see stronger long-term returns from reinsurance than from SIR

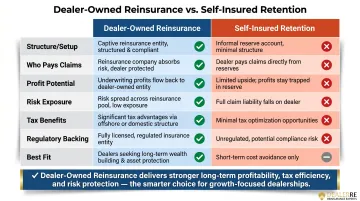

Reinsurance vs. Self-Insured Retention for BHPH Dealers: At a Glance

| Dimension | Dealer-Owned Reinsurance | Self-Insured Retention (SIR) |

|---|---|---|

| Structure/Setup | Formal reinsurance entity (CFC, DOWC) sits behind A-rated fronting carrier; requires legal formation, capitalization, administrator | Per-claim dollar threshold within existing policy; no entity formation required |

| Who Pays Claims | Reinsurance entity pays claims from premium pool; dealer retains underwriting profit after claims | Dealer pays claims directly from operating cash up to retention limit; carrier covers excess |

| Profit Potential | Premium income + investment returns - claims = underwriting profit retained by dealer | Zero profit capture; SIR is pure expense layer |

| Risk Exposure | Limited by A-rated carrier backing above retention layer; catastrophic claims protected | Full exposure within retention limit; no carrier backstop for retained layer |

| Tax Benefits | IRC 831(b) election allows tax only on investment income; underwriting profits accumulate pre-tax | No tax advantages; claims paid from after-tax operating income |

| Regulatory Backing | Licensed structure with carrier backing, trust accounts, regulatory oversight | Policy provision only; no formal regulatory structure |

| Best Fit | Dealers selling 30+ units/month with consistent F&I product attachment | Very limited scenarios; temporary stopgap only |

Both approaches differ from buying third-party F&I products outright — where underwriting profit stays with the warranty company. Of the two retention strategies, only reinsurance gives dealers a structured way to capture that profit margin for themselves.

What is Dealer-Owned Reinsurance for BHPH Dealers?

Dealer-owned reinsurance allows a BHPH dealer to establish a formal reinsurance company—typically using an admin-obligor structure—that sits behind the primary obligor on F&I products like vehicle service contracts (VSCs), GAP, and mechanical breakdown coverage. Instead of paying premiums to a third-party warranty provider, customers' premiums flow into the dealer's reinsurance entity. When claims are lower than premiums collected, the dealer keeps the difference as underwriting profit.

Admin-Obligor Structure Explained

In an admin-obligor arrangement, an administrative company serves as the legal obligor contractually responsible for honoring VSCs and other F&I products. The dealer's owned entity—a CFC (Controlled Foreign Corporation), DOWC (Dealer-Owned Warranty Company), or similar structure—reinsures the risk behind this obligor. The dealer's reinsurance company is backed by an A-rated insurance carrier, creating a professional safety net for catastrophic claims rather than leaving the dealer to absorb unlimited exposure alone.

This differs sharply from pure self-insurance, where the dealer informally sets aside funds with no formal policy structure, no carrier backing, and no regulatory protection.

The Profit Capture Mechanism

Profit accumulates through a straightforward premium flow:

- Premiums from VSCs and other F&I products flow into the dealer's reinsurance company

- Claims are paid from this premium pool

- Administrative fees (typically 20% or less) cover program costs

- Remaining funds accumulate as underwriting profit—money that otherwise would have gone to a third-party provider

Example: A BHPH dealer sells a VSC for $1,000. With a 50% loss ratio, $500 covers claims, $200 covers admin fees, and $300 becomes dealer profit. At 20 VSCs per month, that's $72,000 in annual underwriting profit—before investment income.

Financial Benefits Specific to BHPH Dealers

Tax Planning Advantages: Under IRC Section 831(b), reinsurance entities with less than $2.4 million in annual net premiums are taxed only on investment income—underwriting profits are exempt from current taxation. Offshore CFC structures pay no tax on underwriting profits at all.

That earned income can then be reinvested into the dealership, real estate, education, or other assets, creating compounding wealth well beyond day-to-day operations.

Improved Claims Control: Because the dealer has financial skin in the game, there's built-in motivation to manage inventory quality, reduce breakdown frequency, and adjudicate claims fairly. Better inventory = fewer claims = higher profit retention.

This creates a direct operational feedback loop: the dealer who maintains higher-quality vehicles sees that discipline reflected directly in reinsurance profitability.

How Dealer-Owned Reinsurance Works in a BHPH F&I Program

Those financial benefits play out through a straightforward transaction cycle. Here's how a single deal flows through the program:

- Dealer sells a used vehicle with a VSC for $1,000, financed over the loan term

- Premium deposits into the dealer's reinsurance company trust account

- Customer files a claim for $500 repair; funds are withdrawn to cover the claim

- At contract expiration, $300 (after claims and admin costs) remains as dealer profit

- Surplus accumulates and earns investment income, further growing the pool

Program setup requires working with an experienced reinsurance administrator. DealerRE manages legal filings, tax returns, claims adjudication, compliance, and performance reporting—giving dealers a fully administered program without adding operational complexity to the finance office.

What is Self-Insured Retention for BHPH Dealers?

Self-insured retention (SIR) is the dollar amount a business agrees to pay directly on each claim before any insurance coverage applies. According to IRMI, under an SIR provision, "the insured (rather than the insurer) pays the defense and/or indemnity costs associated with a claim until the SIR limit is reached. After that point, the insurer would make any additional payments for defense and indemnity that were covered by the policy."

SIR in the BHPH Context

In practice, SIR for BHPH dealers means assuming direct financial responsibility for a set dollar amount of each mechanical breakdown or collateral protection loss before any excess or stop-loss coverage kicks in. A dealer might set aside an informal reserve fund, but there's no formal premium-funded structure—claims come straight out of operating cash up to the retention limit.

Critical distinction from a deductible: With a deductible, the insurer pays costs and seeks reimbursement. With SIR, the dealer pays costs directly and manages claims administration within the retention layer.

Operational Risks of SIR for BHPH Dealers

BHPH customers drive older, higher-mileage vehicles and often lack the financial capacity to maintain them. The 2026 CarMD Vehicle Health Index reports the average check engine light repair hit a record $554 in 2025, a 33% year-over-year increase, while the average U.S. vehicle age reached an all-time high of 12.8 years.

When claim frequency spikes—multiple expensive repairs in a short period—SIR arrangements hit operating cash all at once. That means no premium reserve pool, no underwriting income to offset losses, and no carrier backstop when claims run hot.

What SIR Lacks Compared to Reinsurance

- No profit accumulation mechanism

- No underwriting income

- No tax planning benefits

- No A-rated carrier backstop above the retention layer

- No formal regulatory structure or trust account protections

The dealer absorbs losses without building long-term value or creating an equity position.

When SIR Might Appear in a BHPH Dealer's Setup

Many dealers use SIR without realizing it—informally "self-warranting" vehicles by covering repair costs out of pocket to keep good customers on the road and paying. It keeps the customer satisfied short-term, but it's a real missed profit opportunity. Every dollar spent on informal repairs could have been funded by customer premiums through a structured reinsurance program—with the surplus retained as dealer profit instead.

Reinsurance vs. Self-Insured Retention: Which Structure Wins for BHPH Dealers?

Key Decision Factors

BHPH dealers should evaluate:

- Current F&I product volume: How many VSCs, GAP policies, or ancillary products do you sell monthly?

- Inventory quality consistency: Can you maintain reliable vehicles that reduce claim frequency?

- Financial planning horizon: Are you focused on short-term cash preservation or long-term wealth building?

- Current profit leakage: Are you giving underwriting profit to third-party providers or absorbing repair costs informally?

Profitability Potential: Direct Comparison

Reinsurance model: Every policy sold creates underwriting profit potential. With an average VSC premium of $800, a 50% loss ratio, and 20% admin costs, each contract generates $240 in profit. At 20 contracts per month, that's $57,600 annually—plus investment income on reserves.

Over five years at that margin, a dealer selling 20 VSCs monthly accumulates approximately $288,000 in underwriting profit, not counting investment returns. A dealer who implemented a reinsurance program in 2016 accumulated $2 million in a reinsurance trust account, while a comparable dealer who declined left an estimated $1.5 million in unrealized profit.

SIR model: No premium income flows back to the dealer. Every claim within the retention limit is a direct expense. Over the same five-year period, the dealer pays claims from operating cash with zero profit capture and no compounding wealth accumulation.

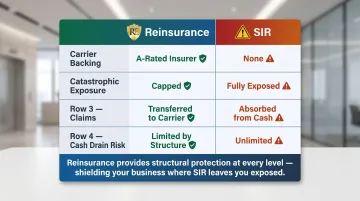

Risk Exposure and Downside Protection

| Reinsurance | SIR | |

|---|---|---|

| Carrier backing | A-rated insurer above retention layer | None |

| Catastrophic exposure | Capped at reinsurance entity capitalization | Fully exposed |

| Excess claims | Transferred to carrier | Absorbed from operating cash |

| Cash drain risk | Limited by structure | Unlimited within retention limit |

Situational Recommendations

Choose reinsurance if:

- You sell VSCs, GAP, or other F&I products consistently (30+ units/month)

- You want to stop surrendering underwriting profit to third parties

- You're willing to invest in structured, long-term wealth building

- You value claims control and operational discipline

Consider SIR only if:

- You're in a very limited, short-term scenario with no formal program in place

- You have no F&I product volume to reinsure

- You're unwilling to commit to entity formation and ongoing administration

Common Misconceptions Addressed

Myth: Reinsurance requires massive fleet size or high volume to be worthwhile. Reality: DealerRE works with dealers selling as few as 30 cars per month. The profit accumulation math works at modest scale—you don't need high volume to make the numbers move in your favor.

Myth: SIR and reinsurance are functionally similar—both involve retaining risk. Reality: They're structurally different products. Reinsurance builds dealer equity through premium income and underwriting profit. SIR is a cost-absorption layer with no profit potential whatsoever.

A Real-World Look: What Happens When BHPH Dealers Choose Each Path

One BHPH dealer informally self-warranted vehicles, paying repair costs from operating cash to keep customers current on payments. Over six years, repeated repair payouts drained working capital during exactly the moments the business needed it most—high-claim periods often coincided with tighter collections months, compounding the cash pressure.

A comparable dealer implemented a dealer-owned reinsurance program in 2016, selling VSCs funded by customer premiums. That dealer's repair costs came from the reserve account—not operating cash—while underwriting profits accumulated separately in a trust.

The structural difference: both dealers sold similar vehicles and served similar customers. The reinsurance dealer captured the profit margin the self-warranting dealer gave away—transforming a cost center into a wealth-building asset.

For BHPH dealers ready to stop giving away underwriting profit, DealerRE offers program analysis to evaluate whether an admin-obligor reinsurance structure fits your operation. Call DealerRE at (804) 824-9533 to find out what your current structure is actually costing you.

Conclusion

For BHPH dealers currently using SIR informally or surrendering F&I profit to third-party warranty companies, dealer-owned reinsurance is not just a risk management tool—it's a profit recovery strategy with compounding long-term financial benefits. SIR keeps cash exposed and profit outside the dealer's control.

The advantages of reinsurance compound over time: claims control reduces breakdown costs, underwriting profit builds in a tax-advantaged structure, and A-rated carrier backing provides financial security SIR arrangements lack. Given the harsh financial realities BHPH dealers face—default rates exceeding 35% and repossession assignments reaching 2.1 million in 2025—the reinsurance decision is one of the most impactful financial choices a BHPH dealer can make.

Reinsurance turns F&I products from a profit leak into a profit engine. Dealers who make that shift stop funding a third party's bottom line and start building their own.

Frequently Asked Questions

What's the difference between reinsurance and insurance?

Insurance transfers risk from a policyholder to an insurer. Reinsurance is a layer on top where the insurer (or in a dealer-owned structure, the dealer's company) transfers a portion of that risk to another carrier. The dealer captures premiums and underwriting profit rather than paying them to a third party.

What are the main types of reinsurance?

The two primary types are treaty and facultative. Treaty reinsurance covers classes of business automatically under a contract. For BHPH dealers, the admin-obligor structure is most relevant: the dealer's company reinsures risk behind a fronting carrier backed by A-rated insurers.

What is the retention limit in reinsurance?

The retention limit is the amount of risk a reinsurance company keeps on its own books before ceding excess to a reinsurer. In dealer-owned programs, this limit is set so the dealer retains enough risk to accumulate profit while ceding exposure that could exceed reserves.

What does self-insured retention mean?

SIR is the dollar amount a business agrees to pay directly on each claim before insurance coverage applies. In a BHPH context, the dealer absorbs repair or collateral protection losses from operating cash up to that defined threshold, with no premium income or profit capture.

What is the difference between self-insurance and captive insurance?

Self-insurance is an informal reserve approach with no licensed entity, formal policy structure, or regulatory oversight. Captive insurance, including dealer-owned reinsurance, is a legally structured entity that issues policies, collects premiums, and provides tax planning benefits along with the ability to invest premium funds.

What is reinsurance at a car dealership?

Dealer-owned reinsurance lets a dealership create its own reinsurance company behind F&I products like VSCs and GAP. Instead of sending underwriting profit to a third-party provider, the dealer collects premiums, pays claims, and keeps what's left as earned income.