Introduction

Vehicles break down — that's the universal reality every Buy Here Pay Here dealer faces. When subprime customers rarely have cash for repairs, warranty decisions reach well beyond customer service — they directly affect cash flow, tax liability, compliance exposure, and long-term profitability. 37% of U.S. adults cannot cover a $400 emergency expense with cash, and BHPH customers skew even more financially vulnerable. A single breakdown can trigger default, turning a performing loan into a repossession.

That repossession risk makes your warranty approach one of the most consequential operational decisions in your dealership. This article compares two paths: managing warranty obligations in-house versus establishing a dealer-owned reinsurance company. In-house warranty keeps costs visible but drains capital and creates uncontrolled liability. A dealer-owned reinsurance structure converts those same obligations into a profit center funded by your customer base.

With subprime auto loan delinquency at 15.78% as of Q3 2025 — more than four times the overall rate — choosing the wrong structure compounds an already tight margin environment.

Key Takeaways

- In-house warranty approaches expose dealership gross profit to ordinary income tax and create unpredictable cash drains when major repairs hit

- Dealer-owned reinsurance captures the underwriting profits third-party companies keep by routing customer-funded premiums through a separate legal entity you control

- Unwritten warranty practices can trigger implied lifetime warranty liability under state consumer law, creating real litigation exposure

- IRC 831(b) programs tax reinsurance distributions at dividend rates rather than ordinary income rates, creating a meaningful tax advantage

- Modern reinsurance programs require neither high volume nor large upfront capital — the structure scales from modest volumes upward

In-House Warranty vs. Dealer-Owned Reinsurance: Quick Comparison

| Comparison Factor | In-House Warranty | Dealer-Owned Reinsurance |

|---|---|---|

| Profit Retention | Dealer absorbs costs from gross profit; no structured profit capture | Unclaimed reserves become dealer profit in trust account; captures what third parties kept |

| Tax Treatment | Informal reserves taxed as gross profit at standard business rate | 831(b) election taxes only investment income; distributions taxed at dividend rate |

| Claims Control | Dealer decides case-by-case; no structure, no nationwide support | Professional claims team adjudicates; includes roadside assistance and 800-number |

| Compliance Risk | Informal coverage implies lifetime bumper-to-bumper warranty under consumer law | Admin obligor structure with legal coverage language protects dealer |

| Customer Financing | Upfront costs deplete lending pool; customer can't finance warranty | Customer finances warranty on contract; pro-rated premiums flow to trust monthly |

What Is an In-House Warranty for BHPH Dealers?

An in-house warranty represents an informal arrangement where the dealer personally absorbs vehicle repair costs. Three approaches dominate:

Self-funded cash reserve: Dealers set aside money internally for anticipated claims. The core problem: under IRC Sec. 461, informal warranty reserves fail the all-events test because liability remains contingent until a customer files a valid claim. The IRS treats reserved funds as dealership gross profit, forcing you to pay income tax before using the money for repairs. That tax drag erodes every dollar you set aside.

50/50 split with customers: Works only for minor repairs. In the BHPH market where customers are credit-challenged, requiring them to pay half often results in you paying the full amount anyway or losing the customer and their future payments to repossession. When BHPH customers carry an average default rate of 31.41%, unexpected repair costs accelerate defaults directly.

Third-party warranty purchase: Offers structure but requires large upfront cash that depletes your lending pool. You also put claim decisions in the hands of a company whose financial incentive is denial, leaving you to fight for your customers or absorb the goodwill costs regardless.

The Compliance Trap Most Dealers Don't See

Operating without clearly defined written coverage terms (even informally) can expose you to claims of an implied lifetime warranty under state consumer protection law. The FTC Used Car Rule requires dealers to disclose warranty status on the Buyers Guide, and violations carry penalties of $53,088 per occurrence. When you make verbal promises without documented limits, you create enforceable obligations that exceed any repair cost.

Use Cases of In-House Warranty

In-house approaches persist primarily among:

- Very low-volume operations (fewer than 5 cars monthly) that haven't reached the threshold where structured programs justify setup costs

- Dealers unaware that better options exist

The out-of-town breakdown problem exposes in-house programs' core weakness. When a customer's vehicle fails 200 miles away, you have no repair network to call and no funding mechanism beyond writing a personal check.

GWC Warranty identifies mechanical breakdown as the #1 reason BHPH customers default. That single data point illustrates why unmanaged breakdowns are a direct threat to your receivables portfolio.

What Is Dealer-Owned Reinsurance for BHPH Dealers?

Dealer-owned reinsurance (also called an admin obligor reinsurance company or 831(b) corporation) is a separate legal entity owned by you that underwrites vehicle service contracts, GAP, and collateral protection products sold to customers — without involving a third-party company that keeps the underwriting profits.

How the BHPH Structure Works

Instead of you paying upfront for a warranty, the customer finances the vehicle service contract cost directly on their retail installment contract. A pro-rated portion of each payment flows into your reinsurance trust account monthly, creating a customer-funded reserve for claims without depleting your lending pool. The cash flow dynamic shifts entirely: you're not fronting capital. Customers fund their own coverage through their monthly payments.

Trust Account Structure

Premiums held in a U.S.-based reinsurance trust are legally protected, not commingled with dealership funds, and can only be used to pay claims or, once earned, distributed as profit to you. This differs entirely from an informal reserve that's taxed immediately. The trust structure ensures funds remain available for their intended purpose while providing legal separation between dealership operations and insurance obligations.

The 831(b) Tax Advantage

Small property and casualty insurance companies with qualifying net premiums up to $2,900,000 (2026 threshold) may elect under IRC 831(b) to be taxed only on investment income. Underwriting profits — premiums minus claims — are exempt from federal income tax at the corporate level. Distributions to you are taxed at dividend rates (0%, 15%, or 20%) rather than ordinary income rates. Compare this to informal in-house reserves where every dollar set aside faces immediate taxation as gross profit.

Admin Obligor Explained

Your reinsurance company is backed by A-rated insurers, giving it the infrastructure of a professional warranty provider. That infrastructure includes:

- Structured coverage terms backed by A-rated carriers

- A nationwide claims adjudication team

- Roadside assistance and a customer-facing 800-number

- Full control over repair direction and claims decisions

No profit goes to a third party. What warranty companies currently pocket stays with you.

Why BHPH Dealers Benefit Most

Reinsurance proves especially powerful for BHPH dealers because payments stop when cars stop running. When you have a funded, professionally managed system to get customers back on the road quickly, you directly protect the payment stream that sustains your business model.

DealerRE's admin obligor program handles the full setup — claims adjudication, legal filings, compliance, staff training, and financial reporting — so you gain the program without adding administrative load to your dealership. Dealers of all sizes have made it work, including those who assumed high volume was a prerequisite.

In-House Warranty vs. Reinsurance: Which Is Better for BHPH Dealers?

The right choice comes down to where your dealership stands on five key variables:

1. Monthly Volume and Growth Trajectory

If you're consistently selling 10+ units monthly, the opportunity cost of not using reinsurance grows significantly each year. Even at lower volumes, the compliance risk alone justifies exploring reinsurance.

2. Current Tax Exposure on Reserves

Every dollar you informally set aside for warranty claims is taxed as ordinary income before you use it. Reinsurance eliminates this double taxation.

3. Compliance Risk Tolerance

Informal practices create implied warranty liability. Reinsurance provides legally drafted coverage language that defines exactly what is and isn't covered, protecting you from open-ended obligations.

4. Out-of-Town Breakdown Coverage

In-house programs consistently fail when customers break down away from your lot. Reinsurance provides nationwide claims infrastructure.

5. Liabilities You're Currently Absorbing for Free

Many dealers offer GAP coverage informally, absorbing losses without capturing premiums. Reinsurance converts this liability into a profit center.

The Volume Misconception

Many dealers believe reinsurance requires high monthly volume or large upfront capital. Neither is true. The structure scales from modest volumes upward because premiums are customer-funded, not dealer-funded. Your customers finance their own coverage — you're not writing the check.

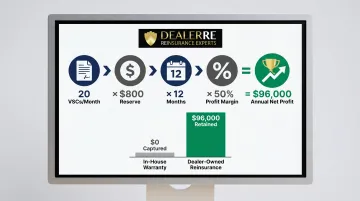

Quantifying the Opportunity

A BHPH dealer selling 20 vehicle service contracts monthly at $800 reserve each with a 50% loss ratio generates approximately $96,000 annually in additional net profit through reinsurance (20 VSCs × $800 reserve × 12 months × 50% profit margin = $96,000). In-house warranty programs leave this entirely on the table.

Who Should Stick With In-House (For Now)

In-house warranty is a short-term option only for dealers under 5 units monthly who haven't yet accessed a structured program — and even then, compliance exposure makes it worth exploring sooner rather than later. For any dealer consistently moving 10+ units monthly, the profit capture, tax advantages, and claims infrastructure that reinsurance provides build on each other in ways an informal program simply can't match. If you're in that range, the longer you wait, the more you leave behind.

Conclusion

For most BHPH dealers, the real question is straightforward: how long can you afford to give away underwriting profits to third parties while carrying the compliance exposure of an informal warranty arrangement? Reinsurance doesn't just reduce that risk — it converts the same warranty obligation into a revenue stream funded by your customers.

Mechanical breakdowns are the leading default trigger in BHPH portfolios. Dealers who address that problem with a structured, compliant reinsurance program — rather than an ad hoc in-house arrangement — protect both their customers and their margins. That combination is what separates dealerships that grow from those that plateau.

If you're ready to explore how dealer-owned reinsurance fits your operation, contact DealerRE at (804) 824-9533 for a dealership analysis.

Frequently Asked Questions

What is the minimum required warranty period for a BHPH dealer on a used vehicle?

Warranty requirements vary by state — some mandate implied or express warranty periods even on as-is vehicles, while others permit as-is sales with proper disclosure. Either way, informal warranty practices need to be documented precisely, since undocumented commitments can expose you to liability well beyond what you intended to cover.

What is the difference between warranty and insurance?

A warranty is a promise by the seller to repair or replace defects (mechanical coverage), while insurance protects against specific financial losses from events like accidents or theft. Dealer-owned reinsurance programs can cover both types of products — VSCs and collateral protection/GAP — under one structure.

What is the difference between buy here pay here and in-house financing?

BHPH is a specific type of in-house financing where the dealership both sells the vehicle and acts as the lender, collecting payments directly. This makes warranty and protection management especially critical because your revenue depends on customers staying on the road and continuing payments.

What does self-insured mean for auto insurance?

Self-insured means a business assumes financial responsibility for losses instead of transferring risk to an insurance company. An informal in-house reserve does exactly that — and brings full tax exposure and liability with it, unlike a properly structured reinsurance entity that carries legal protections for both.

Do I have to use a main dealer to keep my warranty?

With a dealer-owned reinsurance program, customers aren't limited to returning to your lot for covered repairs. They have access to nationwide repair coverage through a professional claims team, which improves the customer experience and keeps your service obligations from bottlenecking at your single location.